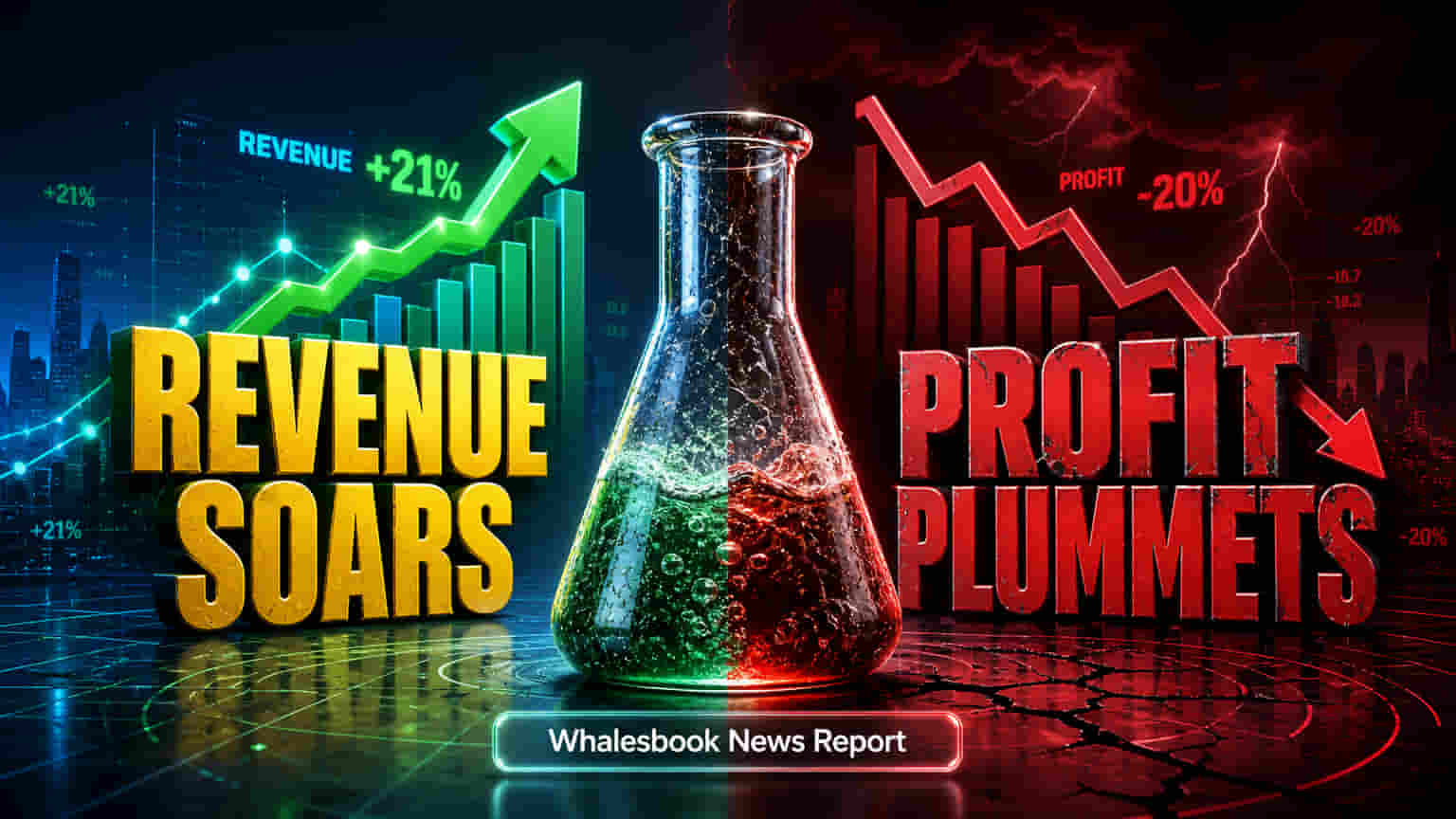

Financial Snapshot

Paushak Limited's fourth quarter of fiscal year 2026 saw a strong 20.74% rise in standalone revenue, reaching ₹63.35 Crores. This quarterly surge, however, contrasted with a challenging full fiscal year. For FY26, the company reported a modest 2.45% year-on-year revenue growth to ₹230.71 Crores. More significantly, annual profit after tax declined by 20.35% to ₹39.33 Crores, down from ₹49.38 Crores in FY25. The board recommended a dividend of ₹2.50 per share.

Debt and Expense Pressures

A key area of concern for investors is Paushak's balance sheet, which saw total borrowings nearly triple from ₹25.01 Crores in FY25 to ₹76.94 Crores in FY26. This substantial increase in debt, alongside a rise in total annual expenses from ₹166.41 Crores to ₹180.30 Crores, contributed to the reduction in profitability. The growing financial leverage and interest outgo present significant risks that require careful management.

Company Background

Paushak Limited, a member of the Alembic Group, holds a prominent position in India's specialty chemical sector. It is the country's largest manufacturer of phosgene-based specialty chemicals and intermediates, drawing on over 55 years of experience in handling phosgene and its derivatives. Its products, including isocyanates and chloroformates, are critical inputs for pharmaceuticals, agrochemicals, polymers, and various industrial applications.

Industry Context

Operating within the specialty chemical market, Paushak competes with firms like Aether Industries, Navin Fluorine International, and Gujarat Fluorochemicals. While Paushak leverages its specialized expertise in phosgene chemistry, its peers often possess broader product portfolios. Notably, Paushak's recent sharp increase in borrowings stands out when compared to the more conservative debt levels typically maintained by companies in this sector.

Investor Outlook

Investors will focus on Paushak's strategic approach to managing its heightened debt burden and efforts to bolster annual profitability. The strong Q4 revenue performance suggests underlying demand for the company's offerings may provide a positive foundation for upcoming quarters. The proposed dividend payment also signals a level of management confidence in the company's near-term financial position, complemented by a clean audit opinion on the latest financial reports.

Key Risks and Future Focus

The primary risks revolve around the persistent pressure on profit margins or higher operating costs that led to the annual profit decline. The elevated debt levels also increase financial risk and interest expenses. Looking ahead, key areas to track include management's detailed commentary on the reasons for the profit dip and its strategy for debt reduction. Investors will also monitor expense management, margin improvement initiatives, and the company's ability to sustain its Q4 revenue momentum into FY27. Updates on capacity expansion or new product developments will also be closely observed.