Revenue growth continues; high raw material costs pose margin pressure.

Key Financial Results

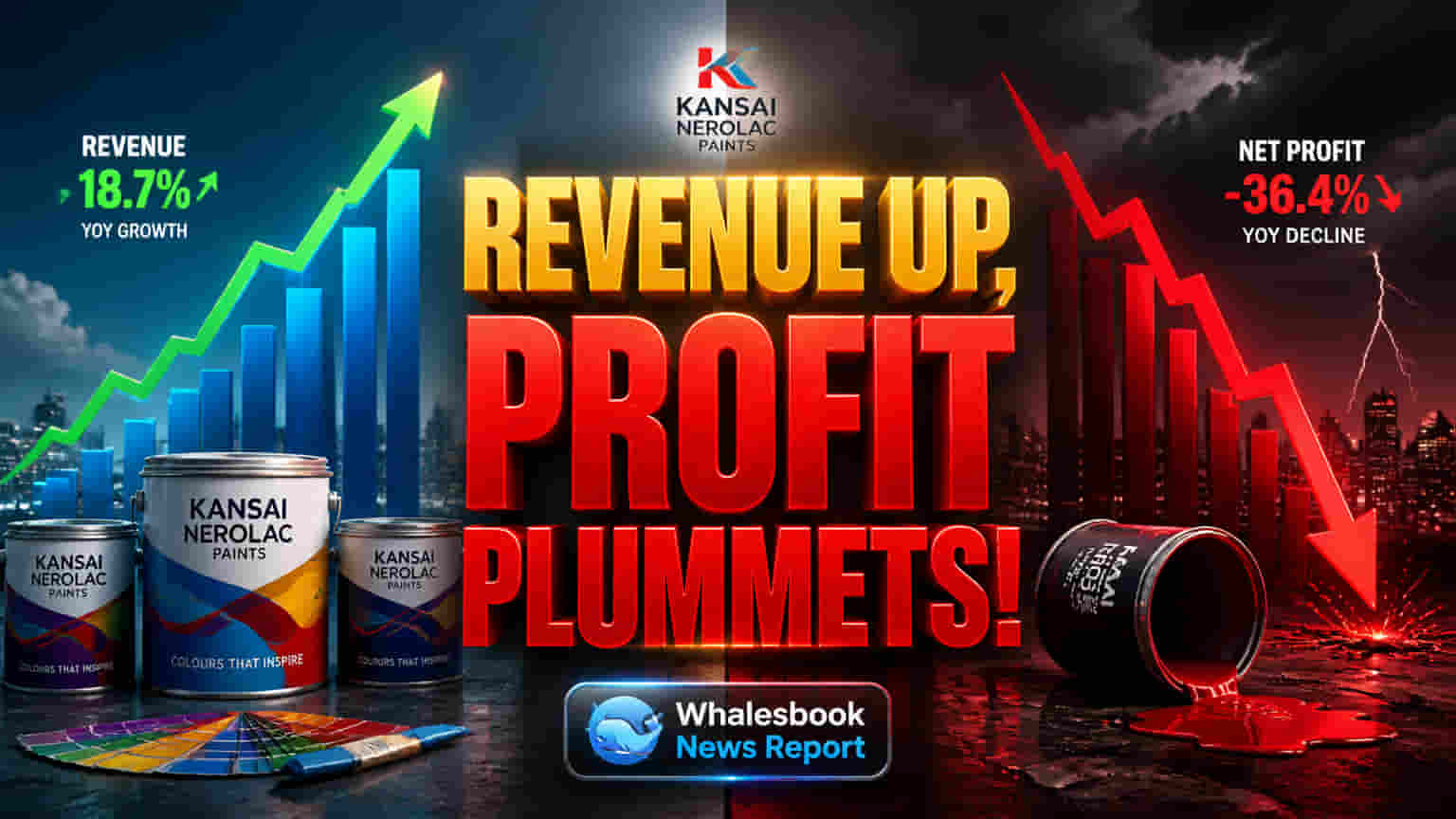

Kansai Nerolac Paints reported strong performance in its top line for the fiscal year ended March 31, 2026. Consolidated revenue for the fourth quarter (Q4 FY26) rose 6.99% year-on-year to ₹1,983.40 crore. For the full fiscal year (FY26), consolidated revenue increased by 2.96% to ₹8,197.85 crore.

However, consolidated net profit saw a significant decline, primarily due to exceptional items. For Q4 FY26, net profit was ₹109.89 crore. For the full year FY26, net profit plummeted 48.11% to ₹575.84 crore. This sharp annual drop was mainly because the prior year recorded a substantial exceptional gain of ₹629.51 crore, while the current year incurred ₹63.15 crore in exceptional losses.

Why it Matters

The revenue growth indicates steady demand for Kansai Nerolac's products and highlights its market presence. The profit contraction reported is largely due to these one-off financial events, rather than a deterioration in core business operations.

Despite these impacts, the company's financial health remains solid. It has strengthened its balance sheet through reduced debt and increased net worth. The key challenge for management moving forward is managing profitability amidst rising input costs.

The Story Behind the Numbers

Kansai Nerolac's financial results in the previous fiscal year (FY25) were significantly boosted by an exceptional gain of ₹665.4 crore from the sale of factory land and buildings at its Lower Parel, Mumbai location in Q3 FY25. This move involved monetizing non-core assets.

In contrast, the current fiscal year (FY26) faced exceptional costs. These included expenses from a fire incident at its Ghaziabad warehouse and costs associated with implementing the New Labour Code (Wage Code).

Industry Challenges and Risks

Kansai Nerolac operates in a competitive market alongside major players like Asian Paints and Berger Paints India. All industry participants are implementing price hikes of 1-8% to counteract rising input costs.

Rising raw material costs, particularly those tied to crude oil, pose a significant risk. Geopolitical tensions in West Asia and currency depreciation are driving these increases. Kansai Nerolac could see profit margins pressured if these costs cannot be fully offset by price adjustments.

Financial Health and Shareholder Returns

The company has demonstrated improved financial health. Consolidated long-term borrowings reduced to ₹8.68 crore as of March 31, 2026, from ₹30.00 crore a year prior. Current borrowings also decreased to ₹74.00 crore from ₹87.82 crore. This deleveraging, alongside an increase in consolidated equity, strengthens the balance sheet.

Shareholders were rewarded with a maintained dividend payout of 250% (₹2.50 per share) for FY26.

What to Watch Next

Investors will monitor the company's ability to implement price increases effectively to offset rising raw material costs.

Key areas to track include the success of cost-control measures and procurement efficiencies in safeguarding margins. Management commentary on the demand outlook, particularly in the decorative and industrial segments, amid geopolitical uncertainties will also be important. Finally, any further developments or financial implications arising from exceptional items, such as the Ghaziabad warehouse incident, should be observed.