Pehle toh revenue ki baat karte hain. JRRL ne Q4 FY26 mein ₹3,104.98 crore ka revenue banaya, jo pichhle saal se 76.42% zyada hai. Poore saal FY26 ka revenue bhi 48.43% badh kar ₹9,543.11 crore ho gaya. Ye sab lead alloy ingots, aluminium alloys aur copper recycling mein badhi volumes ki wajah se hua.

Par ab asli khel shuru hota hai. Jab profit ki baat aayi, toh sabke hosh ud gaye. Q4 FY26 mein net profit sirf ₹66.03 crore raha, jo ki Q3 FY26 ke ₹126.25 crore se 52% kam hai. Haan, pichhle saal se 25.70% zyada hai, par sequential drop bahut bada hai. Pre-tax profit bhi ₹174.4 crore se ₹89.9 crore ho gaya.

Ab sawal ye hai ki yeh profit gira kyun? Motilal Oswal ne bataya ki copper ke unstable prices, scrap ki kami, aur West Asia crisis ki wajah se profit margins pe pressure aaya. Shipping costs bhi badh gaye, aur West Asia crisis ne toh supply chain ki band baja di. Is sabse per ton profit kam ho gaya. Management aur kuch experts ko lagta hai ki ye temporary hai aur Q1 FY27 mein sab theek ho jayega, jab shipping routes normalize honge. Lekin haalat yeh hai ki operating margins 3.54% pe aa gaye, jo pichhle quarter mein 7.17% the.

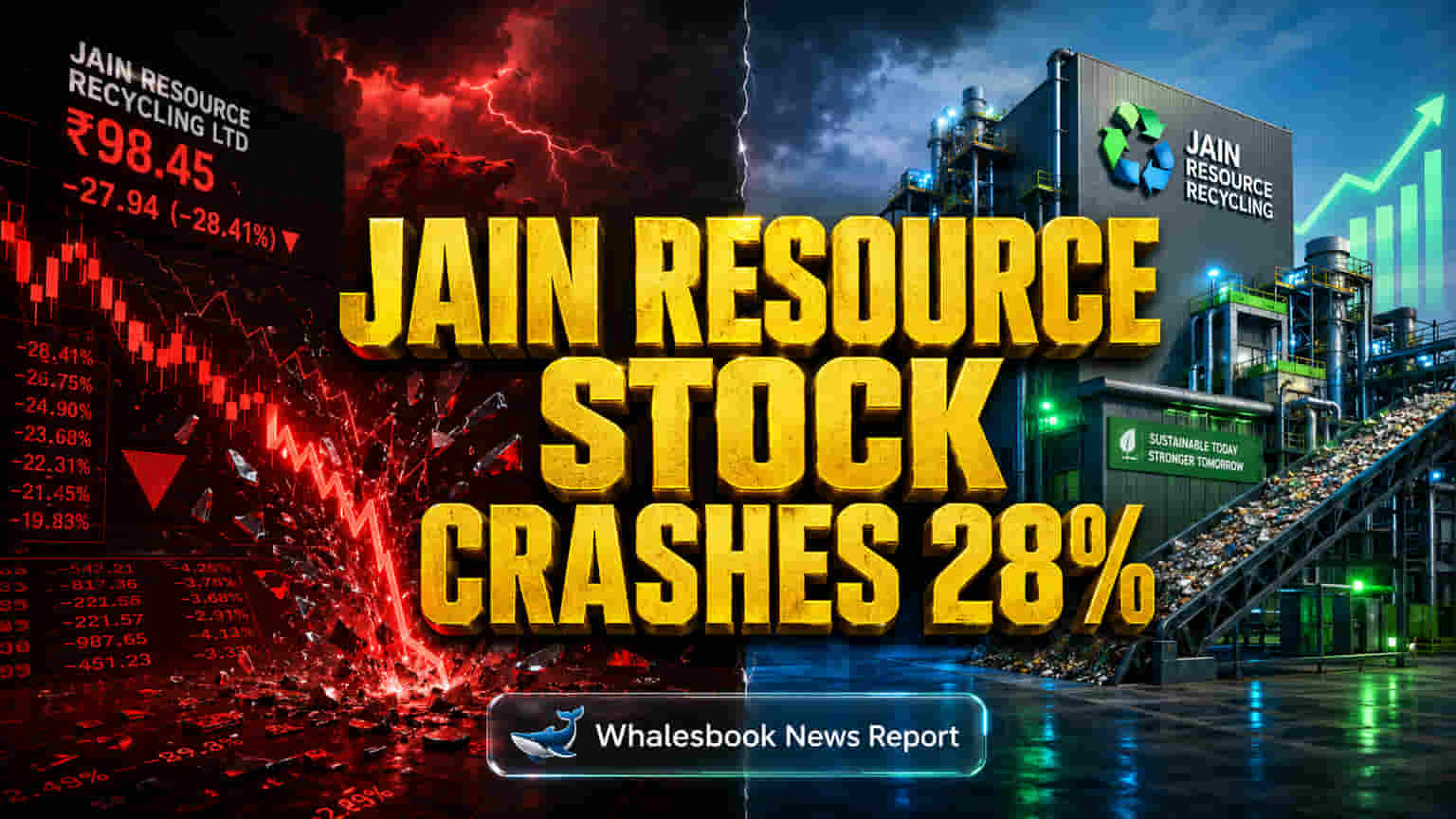

Is result ke baad toh JRRL ka stock 19th May, 2026 ko 15.78% gir gaya. Pichhle do din mein toh lagbhag 28% ka dip aa gaya hai! Aur iska ek bada reason hai company ka bahut high valuation. P/E ratio 51x se 57x tak pahunch gaya tha, jabki industry ka average 22.3x hai. Stock girne se ab investors soch rahe hain ki kya company apni high valuation justify kar paegi.

Brokers ka bhi opinion divided hai. Motilal Oswal ne 'Buy' rating rakhi hai par FY27 aur FY28 ke profit forecasts 15-16% kam kar diye. Dusri taraf, Bitget jaise kuch reports 'Sell' rating de rahe hain. MarketsMOJO ne bhi apna 'mojo grade' 'Buy' se 'Hold' kar diya hai, matlab ab thoda cautious rehne ka time hai.

Abhi bhi risks kam nahi hain. West Asia mein tensions supply chain ko disturb kar sakte hain, jisse shipping costs badhte rahenge. Metal recycling industry mein scrap ki supply aur quality ke issues bhi hain. Company plastic recycling plant bana rahi hai, par woh abhi immediate solution nahi hai. Borrowing costs ka badhna bhi ek chinta ka vishay hai.

Motilal Oswal ko Q1 FY27 mein copper segment mein recovery ki ummeed hai. Plastic recycling plant FY27 ke Q3 tak aa jayega. Lekin ab sabki nazar is baat pe hai ki JRRL kaise unstable commodity prices ko handle karta hai, profit margins kaise stable rakhta hai, aur kya woh apne high valuation ko justify kar pata hai.