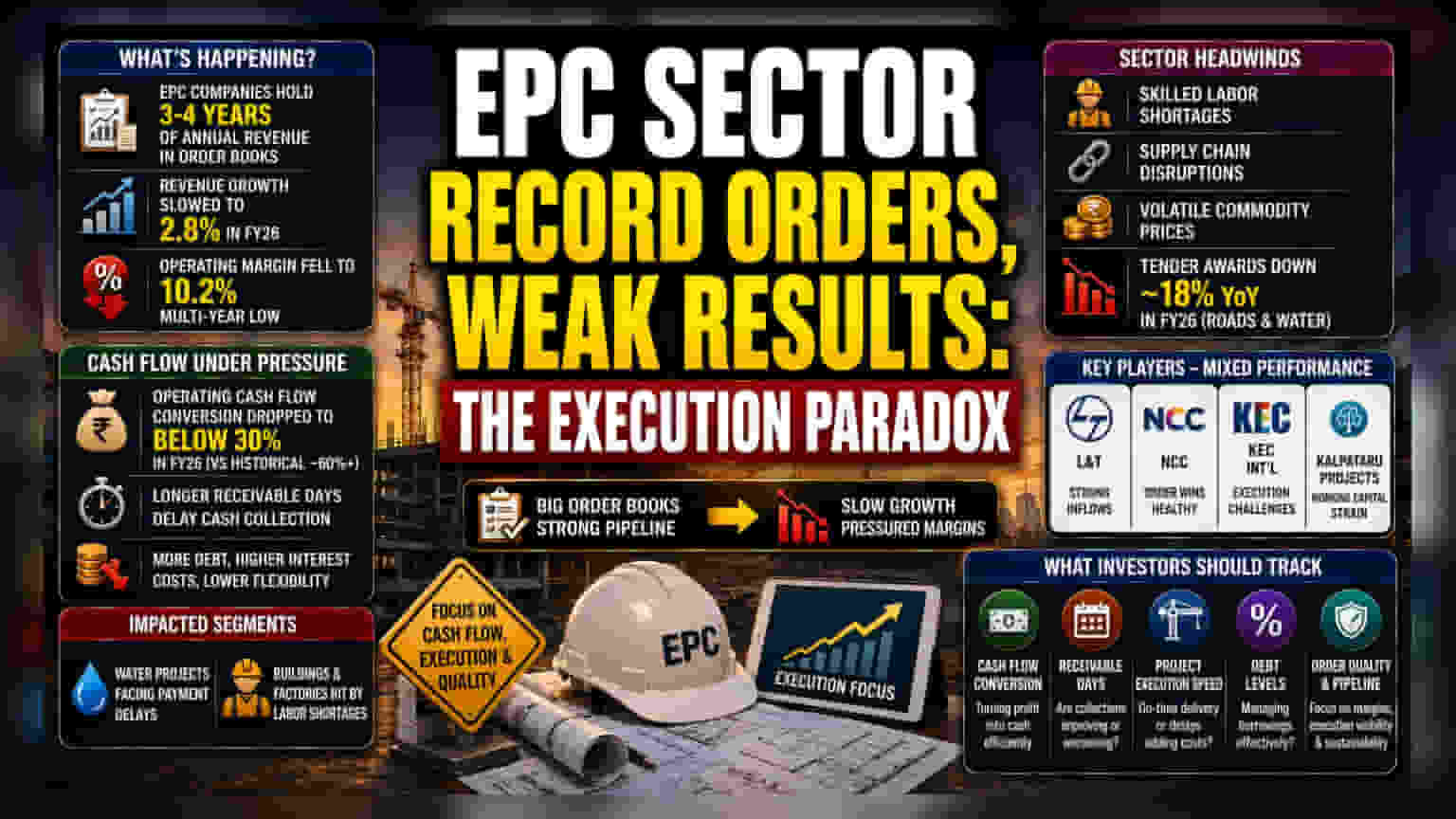

Arre bhaiyo, India ke EPC companies ke paas records tod order hain, itne ki 3-4 saal ki revenue nikal jaaye. Lekin problem ye hai ki in orders ko profit aur cash mein badalne mein mushkil ho rahi hai. Sector ki revenue growth bhi **2.8%** par aakar ruk gayi, aur margins niche jaa rahe hain. Ab investors order se zyada execution speed aur cash management par dhyaan de rahe hain, kyunki payment delays aur labor issues chal rahe hain.

Aisa kya hua?

India ka Engineering, Procurement, and Construction (EPC) sector ek ajeeb si situation mein phas gaya hai. Companies ke paas itne records tod order hain – kuch toh unki saal bhar ki revenue se 3-4 guna zyada – phir bhi woh in orders ko actual financial performance mein badalne ke liye struggle kar rahe hain. Latest data ke hisaab se, sector ki revenue growth FY26 mein 2.8% tak slow ho gayi. Profitability bhi pressure mein hai, operating profit margins 10.2% ke multi-year low par aa gaye hain.

Orders zyada, results kam?

Investors ke liye order book hamesha future income ka signal hota hai. Lekin abhi ki situation dikha rahi hai ki sirf orders hone se quick ya profitable revenue guarantee nahi hai. Companies ko projects shuru karne mein kaafi hurdles face karne pad rahe hain. Jaise ki skilled labor ki kami, raw materials ke liye supply chain mein disruptions, aur volatile commodity prices jisse long-term projects ki budgeting difficult ho jaati hai.

Isi wajah se, FY27 ke liye sector ki revenue growth forecast ko pehle ke 10% expectations se kam karke mid-single digits kar diya gaya hai. Matlab, market ko ab industry ke kai players ke liye growth expectations adjust karni padengi.

Cash flow kahan atak raha hai?

Sabse badi problem hai cash conversion. Simple terms mein, companies apna kaam khatam karne ke baad clients se cash collect karne mein struggle kar rahi hain. Operating cash flow conversion – yani kitna profit actually cash mein badal raha hai – FY26 mein 30% se bhi neeche gir gaya hai. Yeh sector ke historical performance ka aadha bhi nahi hai.

Is cash flow ki problem se sab taraf asar pad raha hai. Companies ko apne rozmarra ke kharchon ko manage karne ke liye zyada debt lena pad raha hai, jisse interest costs badh jaate hain aur doosre business needs ke liye kam paisa bachta hai. Kuch specific segments bhi suffer kar rahe hain: water projects mein payment delays ho rahi hain, aur buildings aur factories segment mein labor ki availability ki problem chal rahi hai.

Sector kaise react kar raha hai?

Bade players jaise Larsen & Toubro (L&T), NCC, KEC International, aur Kalpataru Projects International sabki kahani alag hai is challenging environment mein. Kuch firms strong inflows report kar rahe hain, jabki kuch working capital strain se lad rahe hain. Ek important trend yeh hai ki new tender awards mein 18% year-on-year ki kami aayi hai FY26 mein. Roads aur water projects mein yeh kami dikha rahi hai ki future work ka pipeline shayad pehle jitna strong na ho.

Aage kya dekhna hai?

Ab investors sirf order book ke size par nahi, balki execution ki quality par bhi focus kar rahe hain. Aane wale quarters ke liye important metrics yeh hain:

- Cash Flow Conversion: Kya company apne profits ko efficiently cash mein convert kar pa rahi hai?

- Receivable Days: Clients se payment collect karne mein lagne wala time improve ho raha hai ya nahi?

- Project Execution Speed: Kya projects planned timeline mein complete ho rahe hain, ya delays ki wajah se costs badh rahi hain?

- Debt Levels: Kya company cash flow par pressure hone ke bawajood borrowings ko effectively manage kar rahi hai?

Inko track karke, investors behtar samajh sakte hain ki kaun si companies sector ki current difficulties ko navigate kar pa rahi hain aur kaun si abhi bhi significant operational risks face kar rahi hain.