Blinkit ne Food Delivery ko piche chhoda!

Jo sabse zabardast update hai woh ye hai ki Eternal Limited (jisko pehle Zomato ke naam se jaante the) ka Blinkit ka quick commerce (QC) business, Food Delivery (FD) business se pehli baar user growth mein aage nikal gaya hai Q4 FY26 mein. Agar numbers dekhein toh, net profit 346% badh kar ₹174 crore ho gaya, aur revenue 196.5% upar jaakar ₹17,292 crore ho gaya. Aur suniye, Blinkit ne positive adjusted EBITDA bhi report kiya hai ₹37 crore ka! Quick commerce mein unka market share lagbhag 45-50% ho gaya hai, jo ki bahut bada lead hai. Swiggy Instamart 23-27% aur Zepto 21% ke saath peeche hain.

Profit toh badha, par economy ka kya?

Overall, company ka consolidated adjusted EBITDA 575% badhkar ₹486 crore ho gaya hai, aur margins bhi 2.8% ho gaye hain. Blinkit ke purane markets mein 5-6% tak steady-state margins ki ummeed hai, jabki Food Delivery ke margins 5.5% ho gaye hain. Yeh sab tab ho raha hai jab India mein overall e-commerce growth thoda slow ho gaya hai, jo ab 10-12% par aa gaya hai, pehle ye 20% se upar tha.

Valuation ki chinta aur competition!

Bade profits ke baad bhi ek badi chinta hai stock ka valuation. Company ki market cap ₹2.34-2.45 trillion ke aas-paas hai, par Price-to-Earnings (P/E) ratio 1,000 times se bhi zyada hai, jo ki bahut high hai. Is high valuation par bhi kuch analysts ko stock 'Significantly Undervalued' lag raha hai, lekin P/E ratio toh ek concern hai hi. Quick commerce market mein bhi takkar kaafi zabardast hai, jahan rivals Blinkit ko peeche chhodne ki koshish kar rahe hain. Average order value ₹500-625 ke beech hai.

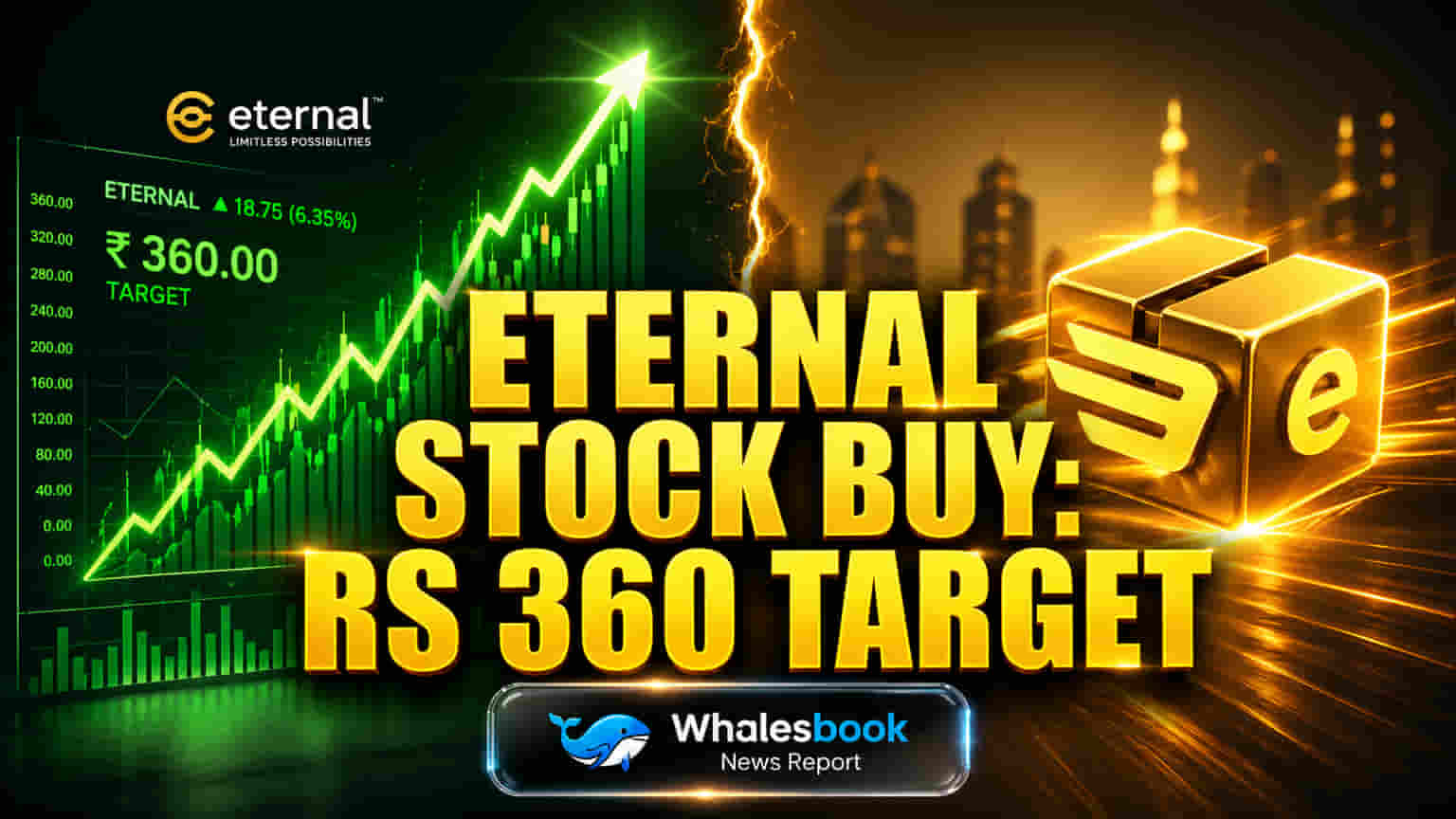

Analysts kya bol rahe hain?

Bahut se analysts abhi bhi Positive hain aur 'Buy' rating de rahe hain, jiska target price ₹359-360 ke aas-paas hai. Lekin sab aise nahi soch rahe. Macquarie jaise analysts ne 'Underperform' rating di hai aur target ₹200 rakha hai, unko growth slow hone aur competition ki chinta hai. Bernstein bhi near-term volatility ki baat kar raha hai. Company ka long-term target hai FY29 tak consolidated adjusted EBITDA $1 billion tak le jaane ka. Investors ko dekhna hoga ki company is high valuation par bhi kaise grow karti hai aur competition mein kaise tikti hai.