Krishna Institute of Medical Sciences (KIMS) ke board ne apne promoters ko **₹600 crore** ke warrants issue karne ka approval de diya hai. Isse company ko expansion ke liye paisa milega aur promoters ki holding bhi badhegi.

Kya hua?

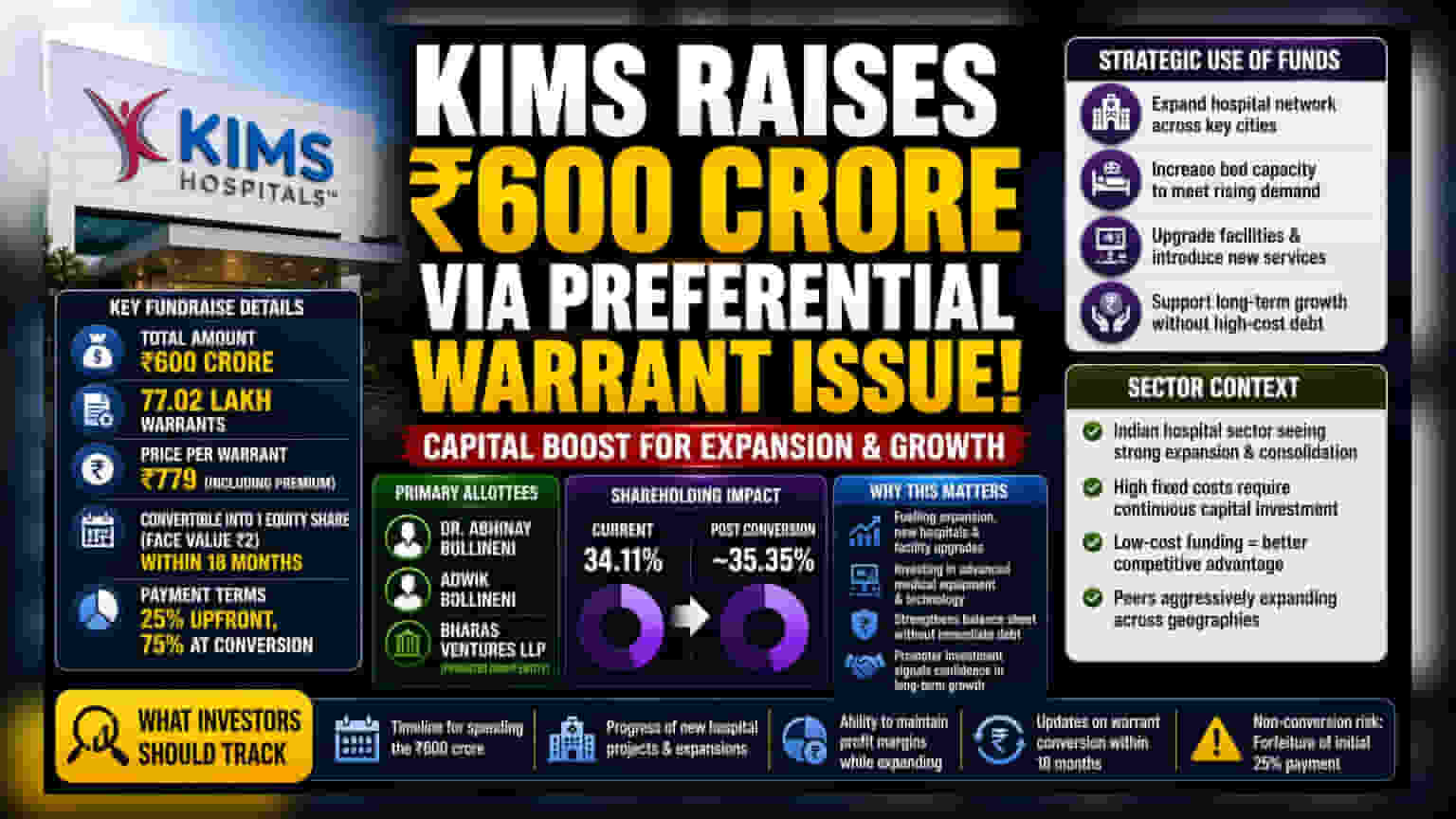

Krishna Institute of Medical Sciences Ltd (KIMS) ke board ne ₹600 crore fundraising ki approval de di hai, woh bhi preferential issue of warrants ke through. Company apne promoters aur promoter group ko 77.02 lakh warrants issue karegi. Har warrant ki price ₹779 rakhi gayi hai, jisme premium bhi shamil hai. Ye warrants allotment ke 18 mahine ke andar kabhi bhi equity share mein convert kiye ja sakte hain.

Terms ke hisaab se, iss deal mein jo log warrants le rahe hain, unhe total amount ka 25% upfront dena hoga, aur baaki 75% tab denge jab warrants ko shares mein convert karenge. Jo promoters iss deal ka hissa honge unme Dr. Abhinay Bollineni aur Adwik Bollineni hain, along with Bharas Ventures LLP. Agar ye sab warrants convert ho gaye, toh promoter group ki company mein current 34.11% holding badhkar lagbhag 35.35% ho jayegi.

Business ke liye yeh kyun important hai?

KIMS jaise hospital chain ke liye yeh capital infusion bahut strategic hai. Healthcare business mein bahut zyada paisa lagta hai, jaise ki naye medical equipment, facility upgrades, aur bed capacity badhana. Agar company promoters ke through paisa raise karti hai, toh bank loan ke interest ka bojh nahi padta aur balance sheet bhi healthy rehti hai. Jab promoters khud ₹600 crore invest karte hain, toh market ise company ke future prospects par ek strong confidence ka sign manti hai.

Funding strategy?

Jab promoters company mein commitment dikhana chahte hain ya cash reserves badhana chahte hain, toh aise preferential issues common hote hain. Public investors ki shares ko dilute kiye bina paisa mil jata hai. 18 mahine ka time frame company ko flexibility deta hai ki woh kab aur kaise paisa use karegi, jisse capital spending plans ke according cash inflow manage kiya ja sake.

Sector mein kya chal raha hai?

Indian hospital sector mein filhaal kaafi expansion aur consolidation ho raha hai. Apollo Hospitals, Max Healthcare, aur Narayana Health jaise players market share ke liye compete kar rahe hain. Ye companies regularly naye cities mein expand karne aur bed count badhane ke liye paisa laga rahi hain.

Hospital business mein fixed costs bahut zyada hote hain – buildings, expensive machinery, aur staff salaries. Isliye, saste mein expansion fund karna ek bada competitive advantage hai. Jo companies internal accruals ya promoter support se growth fund kar pati hain, un par profit margins ke liye kam pressure hota hai, compared to those who rely on high-cost external debt.

Investors ko kya track karna chahiye?

Promoters ka paisa lagana achha signal hai, lekin investors ko ye dekhna chahiye ki yeh funds kitne effectively use hote hain. Hospital sector mein long-term value ke liye naye hospitals ke 'gestation period' par nazar rakhni chahiye. Jab koi company naya facility banati hai, toh usse profit mein contribute karne mein saalon lag sakte hain.

Shareholders ke liye kuch important points ye hain:

- Yeh ₹600 crore actual mein kab aur kaise kharch honge.

- Is capital se fund hone wale naye hospital projects ya expansions ka progress.

- Company ki expand karte hue profit margins maintain karne ki ability.

- Warrants ke conversion ko lekar future updates. Agar 18 mahine mein convert nahi hue toh initial 25% payment forfeit ho jayegi.