Bhai log, home loan lete time sirf interest rate par dhyaan mat do. Processing fees, legal charges, aur tenure ka decision tumhara total loan cost kaafi badha sakta hai. Ye hidden kharche samajhna bahut zaroori hai!

Kya Hua?

Jab bhi log home loan lene jaate hain, sabse pehle to interest rate par hi nazar jaati hai. Haan, rate important hai, par asli picture kuch aur hi hoti hai. Interest ke alawa bhi aise kai kharche aur decision hain jo tumhare loan ko bahut mehnga bana sakte hain.

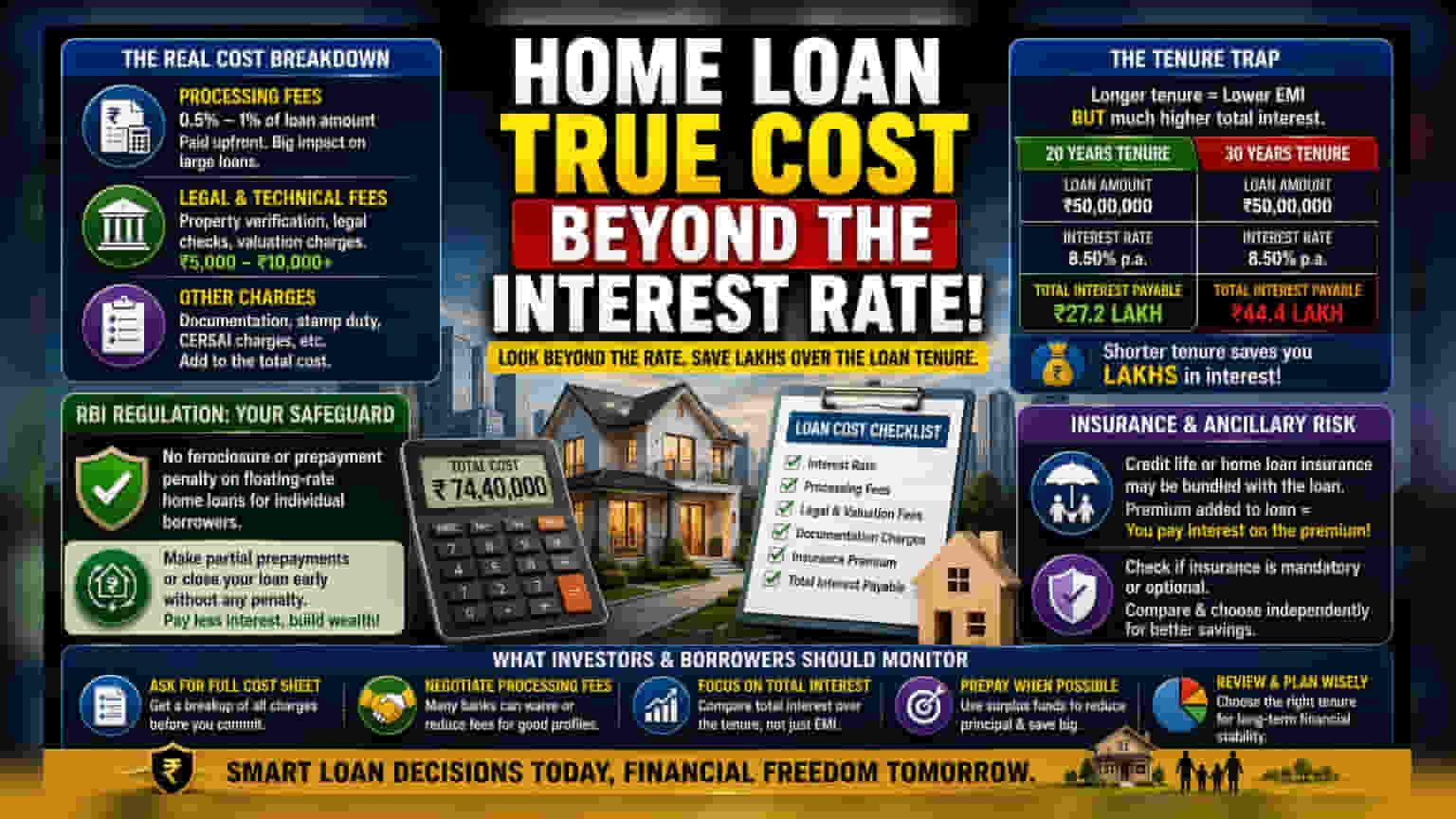

Asli Kharcha Kya Hai?

Home loan ke saath kuch fees judi hoti hain jo ya toh upfront le li jaati hain ya loan amount mein add kar di jaati hain. Processing fees, matlab bank ka administrative charge, usually loan amount ka 0.5% se 1% tak hota hai. Bade loan par ye kaafi badi upfront payment ban jaati hai. Iske alawa, property ke documents aur market value check karne ke liye banks legal aur technical valuation fees bhi charge karte hain. Ye fees kuch hazar se lekar 10,000 Rupees se bhi zyada ho sakti hai, property ke location ke hisab se.

Tenure Ka Chakkar

Bahut log mahine ka kharcha manage karne ke liye sabse lamba loan tenure chunte hain, jaise 30 saal tak. EMI kam ho jaati hai, ye theek hai. Lekin long term mein total interest bahut zyada ho jaata hai. Kyunki interest kam hote principal par calculate hota hai, zyada saal matlab zyada interest pay karna padta hai. Short tenure wale loan ke comparison mein ghar ki total cost kaafi badh jaati hai.

Regulatory Angle (RBI Kya Kehta Hai?)

Ye jaanna zaroori hai ki loan modification ke liye kya rules hain. Reserve Bank of India (RBI) ke according, floating-rate home loans par individual borrowers se banks foreclosure ya prepayment penalty nahi le sakte. Ye ek important protection hai. Agar tumhare paas extra paisa hai aur tum loan jaldi pay karna ya partial payment karna chahte ho, toh tumse penalty nahi li jayegi. Ye total interest kam karne ka sabse effective tareeka hai.

Insurance Ka Risk

Kai lenders loan ke saath credit life ya home loan insurance bhi bundle kar dete hain. Kuch cases mein, insurance ka premium bhi loan amount mein add ho jaata hai, matlab tum us premium par bhi interest pay kar rahe hote ho. Insurance lena ek achhi financial decision ho sakti hai, par tumhe ye clear karna chahiye ki insurance compulsory hai ya optional, aur kya tum use kahin aur se saste mein le sakte ho.

Investors aur Borrowers Ko Kya Dekhna Chahiye?

Home loan offer check karte time, sirf interest rate par focus mat karo, total ownership cost dekho. Borrowers ko saari upfront charges ki list mangni chahiye, jisme processing, legal, aur documentation fees sab shaamil ho. Processing fee ko negotiate karna bhi common hai, kyunki banks creditworthy customers ke liye ye fees kam kar sakte hain. Sabse important, pure tenure mein pay kiya gaya total interest track karo, na ki sirf monthly EMI. Ye sab factors tumhari long-term financial stability ke liye sahi decision lene mein help karenge.