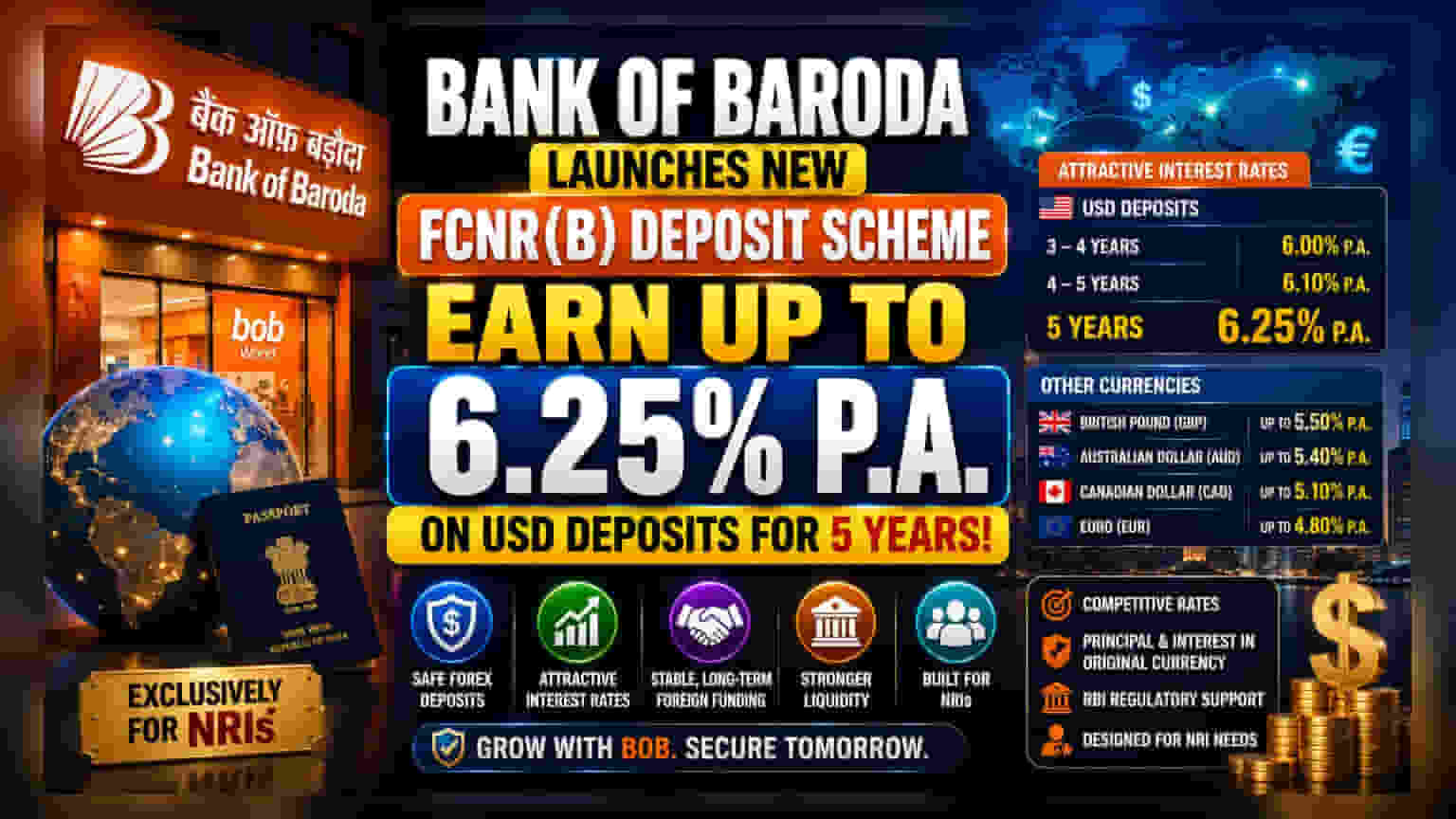

Bank of Baroda ne NRIs ke liye ek dum naya scheme launch kiya hai, jiska naam hai 'bob Legend FCNR(B) Deposit Scheme'. Isme 5 saal ke US dollar deposits par **6.25%** tak ka interest milega. Isse bank ko stable foreign currency milne ki umeed hai.

Kya hua?

Bank of Baroda ne NRIs ke liye 'bob Legend FCNR(B) Deposit Scheme' naam se ek naya product launch kiya hai. Isme US dollar deposits par 5 saal ke liye 6.25% tak ka annual interest milega. Chote terms ke liye bhi rates hain: 3 se 4 saal ke liye 6% aur 4 se 5 saal ke liye 6.1%. Bank ne British pound, Australian dollar, Canadian dollar, aur Euro jaise currencies ke liye bhi rates set kiye hain.

Investors ke liye ye kyun important hai?

NRIs se Foreign Currency Non-Resident (FCNR) deposits attract karna bank ke liye long-term foreign currency funding ka ek smart move hai. Zyaada rates offer karke, bank NRIs ka paisa attract kar sakta hai jo apne funds ko Indian rupees mein convert karne ke bajaye foreign currency mein rakhna pasand karte hain. Isse depositors ka currency fluctuation risk khatam ho jata hai kyunki principal aur interest dono original currency mein milte hain. Bank ke liye, ye deposits liquidity ka ek acha source bante hain.

Investors kaise dekhenge?

Investors hamesha dekhte hain ki deposit growth bank ke net interest margin ko kaise affect karta hai, jo ki loans se kamaya gaya interest aur depositors ko diye gaye interest ke beech ka difference hota hai. Jabki aggressive deposit schemes bank ko apna asset base badhane aur loan demand poori karne mein madad karti hain, ye funds ki cost bhi badha deti hain. Agar bank depositors ko attract karne ke liye zyada interest rates pay karta hai, toh use yeh ensure karna hoga ki woh in funds ko high-yielding loans mein deploy kar sake taaki uske profit margins safe rahein. Investors bank ke quarterly results check karenge ki kya ye naya scheme deposit base ko significantly profit margins ko squeeze kiye bina grow karta hai.

Business ka bada context

Indian banks apne credit growth ko support karne ke liye deposits attract karne mein kaafi competition face kar rahe hain. Credit-to-deposit ratio banking sector ke liye ek important factor bana hua hai, isliye kai institutions stable, long-term capital capture karne ke liye specific products launch kar rahe hain. Reserve Bank of India (RBI) bhi banks ko ye foreign currency deposits manage karne mein regulatory support deti hai, jisme specific tenures ke liye hedging costs absorb karna bhi shamil hai. Ye regulatory environment banks ko liquidity badhane ke liye zyada foreign currency lane ko encourage karne ke liye design kiya gaya hai.

Kya gadbad ho sakta hai?

Shareholders ke liye sabse bada risk cost-benefit balance hai. Agar bank in higher rates par bahut saare deposits attract karta hai lekin usse enough high-quality lending opportunities nahi milti hain, toh in deposits ki cost bank ki profitability ko negatively affect kar sakti hai. Iske alawa, in schemes ki success global investment alternatives dwara offer kiye gaye interest rates par depend karti hai. Agar global interest rates significantly increase hoti hain, toh bank deposit rates kam attractive ho sakte hain, jisse campaign ki success limited ho sakti hai.

Investors ko kya track karna chahiye?

Sabse important factor jo track karna chahiye woh hai bank ka deposit growth numbers upcoming quarterly updates mein. Investors management se 'cost of funds' par commentary bhi dekh sakte hain aur yeh check kar sakte hain ki kya unhe in deposit initiatives se margin pressure dikh raha hai. Credit-to-deposit ratio ko monitor karna bhi yeh insight dega ki bank in naye funds ko kitni efficiency se use kar raha hai. Finally, hedging costs ya foreign currency inflows par RBI ke regulatory stance mein koi bhi change in schemes ki long-term viability ko samajhne ke liye important hoga.