Aakhir numbers mein kya gadbad hui?

Dekho, Tata Motors ne Q3 FY26 mein ₹15.9 billion ka Profit After Tax (PAT) report kiya hai, jo analysts ke ₹18.4 billion ke estimate se kam hai. Iske peeche sabse bada reason hai company ka margin jo ki 12.8% raha, jabki expect kiya ja raha tha ki yeh 13.2% hoga. Ye margin squeeze hua hai badhti hui input costs ki wajah se. Simple words mein, cheezein banane ka kharcha badh gaya hai.

Aur ek chinta ye bhi hai ki company apna market share bhi thoda kho rahi hai kuch important vehicle segments mein. Yeh problem Iveco acquisition se pehle se hi thi, par ab global market ki uncertainties ke karan ispar aur dhyan dena padega.

Iveco acquisition: Yeh deal game changer banegi ya risk?

Tata Motors ne haal hi mein Iveco ko acquire kiya hai €3.8 billion mein, jo unki sabse badi deal hai. Isse company ka commercial vehicle (CV) business aur global presence badhegi. Lekin, is deal ke saath hi Tata Motors par global economic slowdown ka risk bhi aa gaya hai. Agar market mein demand theek se nahi badhi, toh stock valuation par bhi pressure aa sakta hai.

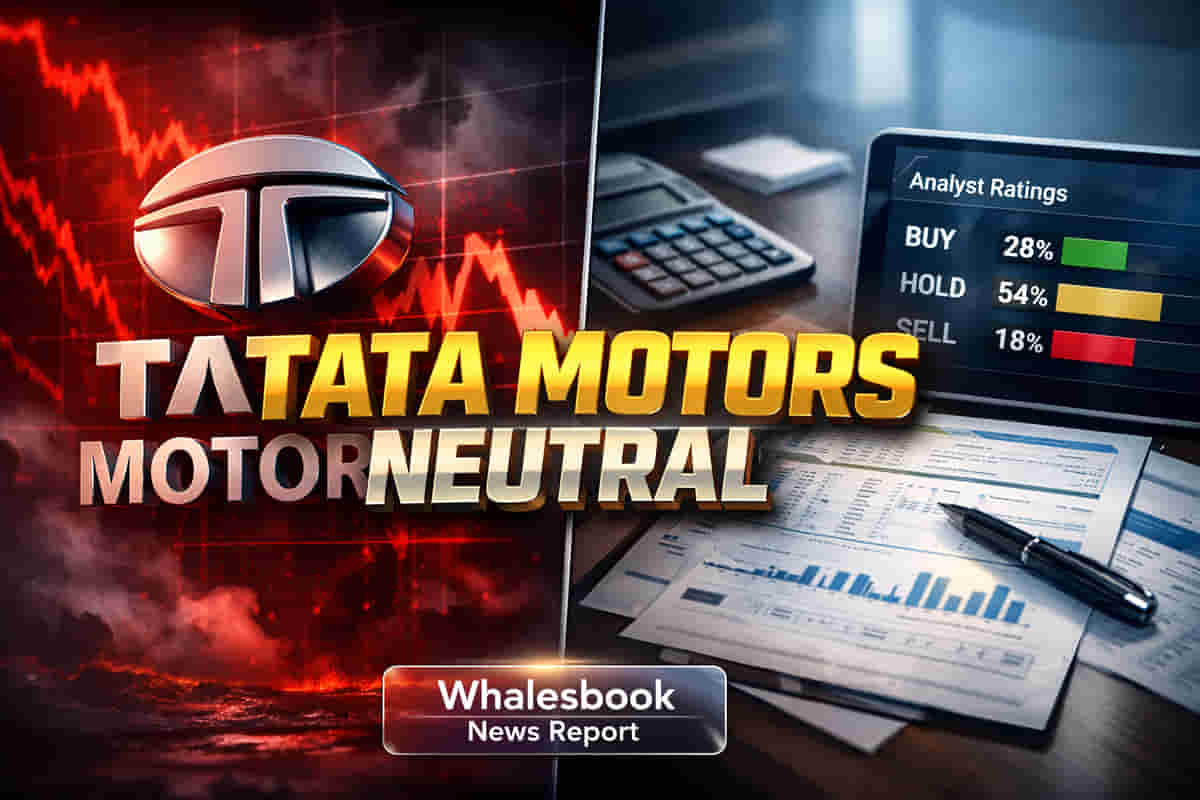

Analysts kya keh rahe hain?

Motilal Oswal jaise analysts ka kehna hai ki domestic CV demand FY25 se FY28 ke beech 9% CAGR se grow kar sakti hai, aur margins bhi around 13% rehne ki umeed hai. Lekin, haal hi mein stock ki rally ke baad, yeh abhi FY27E ke liye 24.1x aur FY28E ke liye 21.8x EPS par trade kar raha hai. Motilal Oswal ke hisaab se yeh valuation theek-thaak hai, isliye unhone 'Neutral' rating maintain ki hai aur target price ₹431 rakha hai. Unhone ye valuation core business par 13x Dec '27E EV/EBITDA multiple laga kar aur Tata Capital stake ke liye ₹13 add karke nikala hai.

Baki, India mein commercial vehicle market ka outlook kaafi strong lag raha hai, aur Tata Motors passenger vehicle segment mein bhi India ki doosri sabse badi car maker ban gayi hai January 2026 tak. Electric vehicle market mein toh yeh leader hai hi, 70% se zyada share ke saath. Lekin EU se import hone wale vehicles par potential tariff reduction ki khabar bhi stock par asar daal sakti hai.