NPS Policy Overhaul Eases Withdrawal Rules

National Pension System (NPS) માં તાજેતરમાં થયેલા નોંધપાત્ર policy shifts માત્ર નિયમોમાં સુધારો નથી. The standard 60/40 split of lumpsum to annuity now requires rethinking, especially as market realities evolve and retirees seek better ways to preserve and grow their capital.

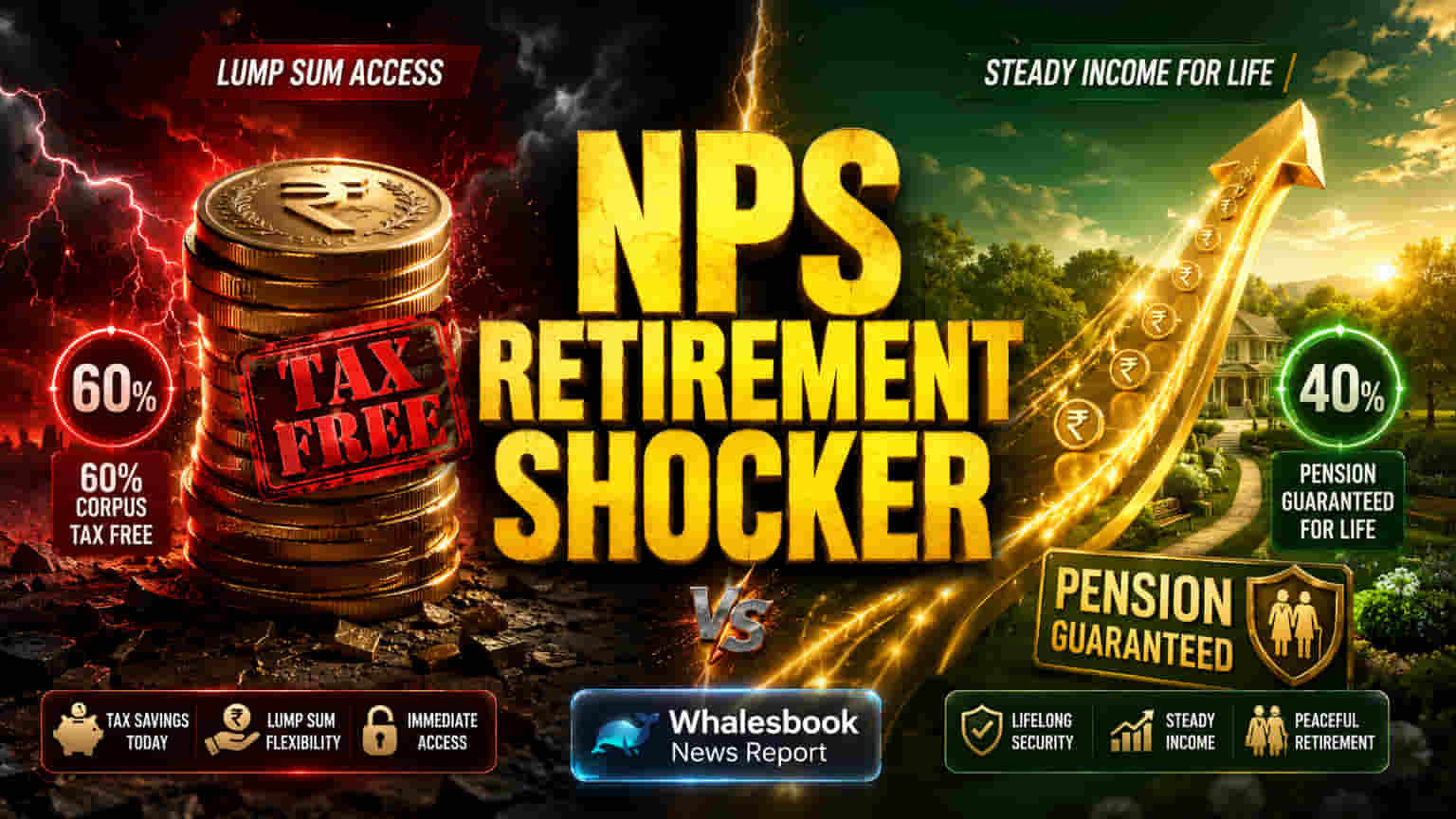

Key Changes to Annuity Mandate

પરંપરાગત રીતે, 60 વર્ષની ઉંમરે પહોંચ્યા પછી, NPS subscribers ને તેમના retirement fund નો ઓછામાં ઓછો 40% ભાગ annuity માં રોકાણ કરવો પડતો હતો, જે આજીવન pension પૂરું પાડે છે. બાકીના 60% lumpsum તરીકે tax-free લઇ શકાતા હતા. જોકે, તાજેતરમાં થયેલા regulatory reforms એ આ સ્થિતિને નાટકીય રીતે બદલી નાખી છે, ખાસ કરીને non-government subscribers માટે. The mandatory annuity component ને ઘટાડીને માત્ર 20% કરી દેવામાં આવ્યો છે, જેનાથી corpus નો 80% સુધી lumpsum withdrawal અથવા systematic withdrawal plans દ્વારા મેનેજ કરી શકાય છે. આ મુખ્ય બદલાવનો હેતુ retirees ને તેમના funds પર વધુ control અને access આપવાનો છે, કારણ કે fixed annuity payouts ગતિશીલ આર્થિક વાતાવરણમાં અપૂરતા સાબિત થઈ શકે છે.

Annuity Shortfalls and Growth Limits

વધેલી withdrawal flexibility હોવા છતાં, mandatory annuity portion પર હજુ પણ ધ્યાન આપવાની જરૂર છે. Annuity rates in 2025 સામાન્ય રીતે વાર્ષિક 5.5% થી 7.5% ની વચ્ચે રહી છે. જ્યારે આ guaranteed income આપે છે, ત્યારે તે ઘણીવાર inflation (જે સરેરાશ 6.65% રહી છે) સાથે તાલ મિલાવી શકતી નથી. આ gap નો અર્થ છે કે fixed annuity payments સમય જતાં ખરીદ શક્તિ ગુમાવે છે. Retirees માટે, આ erosion તેમના standard of living પર નોંધપાત્ર અસર કરી શકે છે. વધુમાં, NPS equity exposure ને મર્યાદિત કરે છે (ઐતિહાસિક રીતે 75% સુધી, કેટલાક frameworks માં 100% સુધી શક્ય), જે વધુ aggressive, market-linked investment strategies ની તુલનામાં potential capital appreciation ને પ્રતિબંધિત કરે છે. છેલ્લા વર્ષમાં, NPS equity schemes માં 20% ના મધ્યથી 30% ના ઊંચા returns જોવા મળ્યા છે, જે capped allocation સાથે ગુમાવી શકાય તેવી growth potential દર્શાવે છે.

Risks from Annuities and Market Volatility

ઓછા કરેલ 20% mandatory annuity પણ કુલ portfolio returns પર drag તરીકે કાર્ય કરે છે. આ fixed-income instruments સામાન્ય રીતે market-linked investments કરતાં ઓછું વળતર આપે છે, જે એક opportunity cost રજૂ કરે છે. વધારામાં, annuity income વ્યક્તિના income tax slab મુજબ કરપાત્ર છે, જ્યારે lumpsum withdrawal tax-free રહે છે. એક મુખ્ય risk 'sequence of returns' નું છે. આનો અર્થ એ છે કે retirement ના શરૂઆતના તબક્કામાં નબળા market performance અથવા ઊંચો inflation પોર્ટફોલિયોને નોંધપાત્ર રીતે ઘટાડી શકે છે, ખાસ કરીને જ્યારે corpus નો મોટો ભાગ low-return annuities માં ફસાયેલો હોય. 'Safe Withdrawal Rate' (SWR) ની કલ્પના, જે સામાન્ય રીતે sustainable portfolio longevity માટે 4-4.5% હોય છે, તે પ્રાપ્ત કરવી વધુ મુશ્કેલ બની જાય છે જ્યારે corpus નો એક ભાગ fixed, સંભવિત રીતે underperforming annuities માં lock થયેલો હોય. તાજેતરના surveys દર્શાવે છે કે ઘણા retirees retirement માટે ઓછી preparation ધરાવે છે, increased awareness હોવા છતાં, સૂચવે છે કે તેઓ withdrawal phase ને અસરકારક રીતે મેનેજ કરવામાં સંઘર્ષ કરી શકે છે, જેનાથી annuity portion થી risks વધી શકે છે.

Outlook for Retirees

તાજેતરના regulatory shifts, જે withdrawal flexibility માં વધારો દર્શાવે છે, તે annuity ની મર્યાદાઓની awareness દર્શાવે છે. The reduction in the mandatory annuity percentage અને phased withdrawals અથવા higher lump-sum access માટે વધેલા વિકલ્પો હકારાત્મક પગલાં છે. જોકે, retirement income ની લાંબા ગાળાની sustainability આખરે તેના પર નિર્ભર રહેશે કે retirees કેટલી અસરકારક રીતે guaranteed પરંતુ સંભવિતપણે અપૂરતી annuity payments ને market-linked growth ની તકો સાથે સંતુલિત કરી શકે છે. Proactive financial planning, જેમાં ઉપલબ્ધ હોય ત્યાં inflation-adjusted annuity વિકલ્પો પર કાળજીપૂર્વક વિચારણા કરવી અને lumpsum portion નો strategic deployment શામેલ છે, તે post-retirement જીવનને comfortable બનાવવા માટે crucial રહેશે.