S&P Global Ratings has upgraded Adani Ports and Special Economic Zone (APSEZ) to 'BBB' from 'BBB-', citing robust cash flows and improved debt levels. This credit upgrade supports the company's ambitious plan to scale domestic port capacity to 1 billion metric tonnes by 2030. Investors may watch how this improved credit profile impacts future borrowing costs.

What Happened

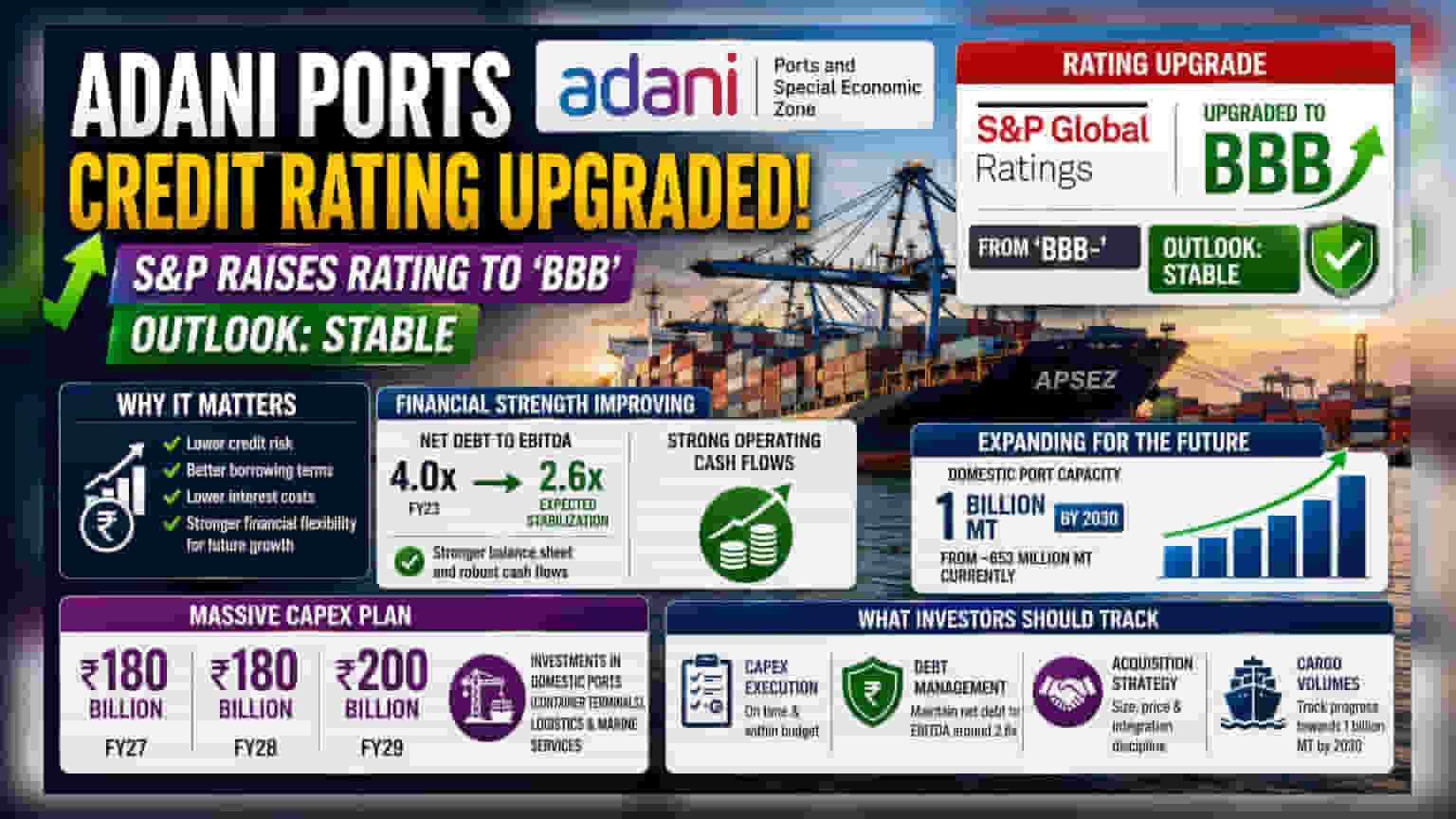

S&P Global Ratings has raised the long-term issuer credit rating for Adani Ports and Special Economic Zone Ltd. (APSEZ) to 'BBB' from the previous 'BBB-' designation. The rating agency also assigned a stable outlook to the company. This upgrade, announced on June 25, 2026, reflects the port operator's improved financial health, characterized by robust operating cash flows and a strengthening balance sheet.

Why This Matters For Investors

A credit rating upgrade from a global agency typically signals lower credit risk, which can lead to better borrowing terms and lower interest costs when the company raises debt in the future. For APSEZ, this improved standing comes at a crucial time as it executes a massive capital expenditure program. The company is actively working to expand its domestic port capacity to 1 billion metric tonnes by 2030, a significant increase from its current capacity of approximately 653 million metric tonnes.

The Financial And Expansion Picture

The upgrade is supported by a marked improvement in the company's leverage ratios. S&P expects APSEZ's net debt-to-EBITDA ratio to stabilize around 2.6x, a notable improvement from the 4.0x level seen in fiscal year 2023. This disciplined approach to managing debt provides the company with more financial flexibility to fund its planned expansion.

APSEZ has outlined significant investment plans, with capital expenditure projected to rise to approximately ₹180 billion annually for fiscal years 2027 and 2028, increasing further to ₹200 billion in fiscal 2029. Much of this capital is earmarked for domestic port expansion, particularly container terminals, along with logistics and marine services. These investments are intended to drive volume growth and sustain earnings quality over the coming years.

What Investors Should Track

While the credit upgrade provides a positive signal, investors should continue to monitor several factors as the company moves through its high-growth phase:

- Capex Execution: With substantial spending planned through 2029, the ability to execute projects on time and within budget will be a key driver of long-term returns.

- Debt Management: While the current leverage trend is downward, sustaining a net debt-to-EBITDA ratio of around 2.6x during a period of heavy investment will be essential to maintaining this credit rating.

- Acquisition Strategy: The company has indicated it may remain acquisitive to achieve its growth goals. The size, price, and integration of any new assets will influence future cash flows and earnings quality.

- Cargo Volumes: Success relies on achieving the 1 billion metric tonne target by 2030. Monitoring quarterly volume updates and utilization rates of new facilities will help assess the success of these expansions.

Overall, the market will likely view this upgrade as validation of the company's ability to balance aggressive infrastructure development with a disciplined financial profile.