The Valuation Gap

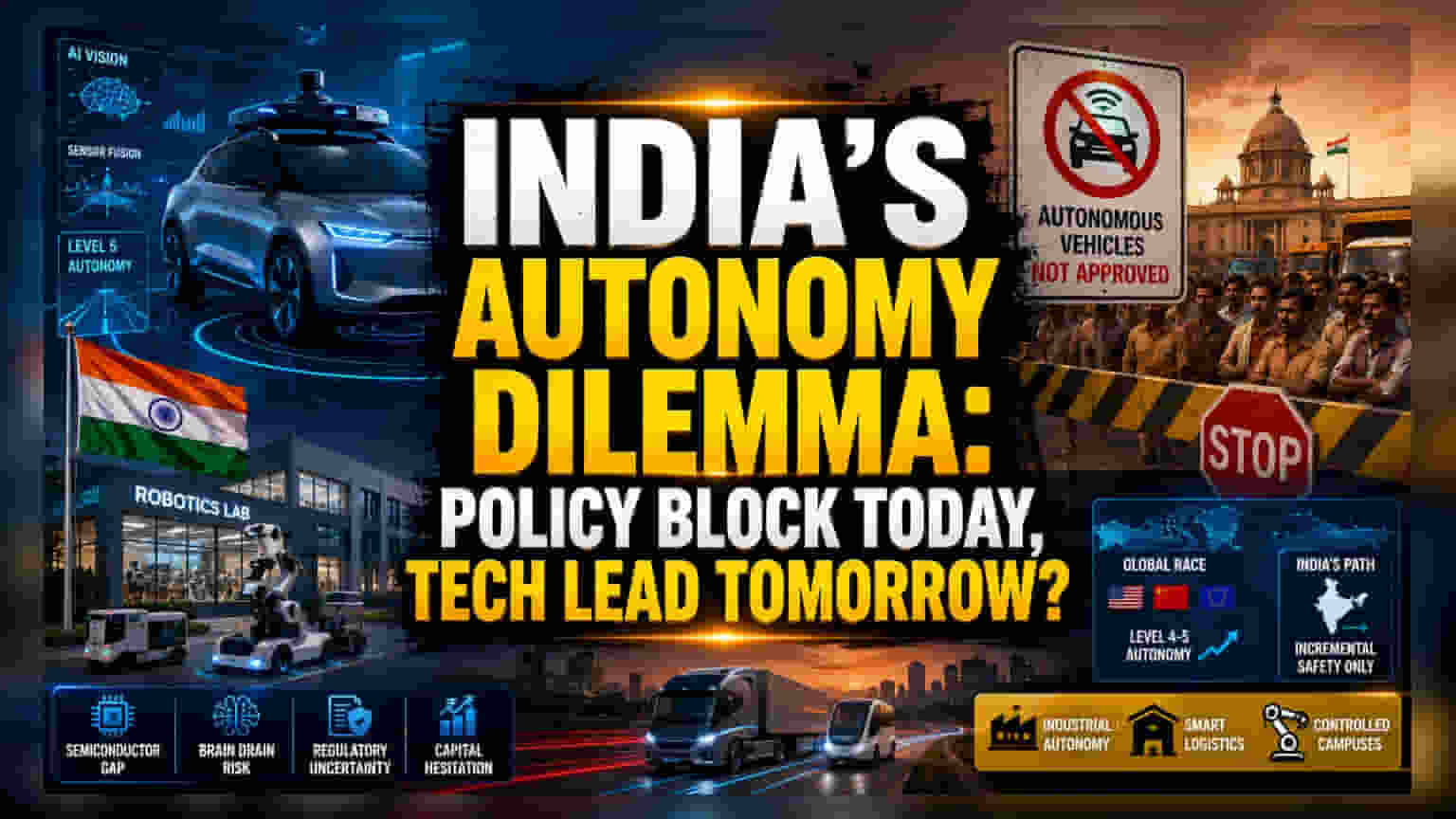

The Indian government’s refusal to sanction autonomous vehicles—driven by the stated concern of displacing millions of commercial drivers—has created a divergence between domestic policy and global industry trajectories. While transport authorities focus on preventing job displacement, the underlying technology shift is already occurring through non-vehicular applications and industrial automation. The core issue remains that while the domestic market prioritizes labor stability, global competitors are rapidly building out the foundational AI, sensor fusion, and data stacks that will define the next generation of logistics and transport. By restricting testing, India effectively limits the scale of local R&D, forcing native firms to either pivot toward industrial-only applications or relocate their testing facilities abroad to refine their autonomous systems.

The Analytical Deep Dive

Comparing India’s stance to global counterparts reveals a widening divergence. As nations like the U.S. and China accelerate toward Level 4 and Level 5 automation, India’s current strategy leans heavily into semi-autonomous, safety-focused interventions, such as the mandatory Vehicle-to-Vehicle (V2V) communication systems slated for 2026. This focus on incremental safety features acts as a temporary buffer but does little to capture the broader economic value of full-stack autonomy. Historic underinvestment in semiconductors and advanced battery manufacturing serves as a cautionary tale; the country now risks repeating that cycle within the autonomous vehicle stack. Despite this, a vibrant private ecosystem including startups and technical institutions continues to develop vision-based systems and niche robotics, often operating in a regulatory vacuum. These entities remain the primary hope for maintaining even a modest competitive foothold in the global mobility hierarchy.

The Forensic Bear Case

Risks for the domestic sector are structural and substantial. The reliance on legacy, labor-intensive business models creates a high barrier to the adoption of advanced automation. Critics of the current policy argue that by suppressing R&D, the government is incentivizing a 'brain drain' of top engineering talent to more permissive markets. Furthermore, the absence of a comprehensive regulatory framework for liability, algorithmic accountability, and data governance leaves the industry vulnerable to both internal disruption and external technological capture. Unlike global peers that have established clear testing corridors, Indian companies face persistent capital hurdles as investors shy away from sectors where the path to commercialization remains blocked by long-standing ministerial opposition.

The Future Outlook

Looking ahead, the sector is likely to see further bifurcation. Commercial logistics and industrial campuses, which operate in controlled environments, will likely serve as the primary sandbox for autonomous innovation, circumventing public road prohibitions. Market analysts anticipate that the shift toward software-defined vehicles will force a policy re-evaluation, particularly as the domestic automobile industry seeks to retain its global relevance. Until then, the sector will likely remain characterized by high-intensity innovation in limited industrial silos rather than broad-based public adoption.