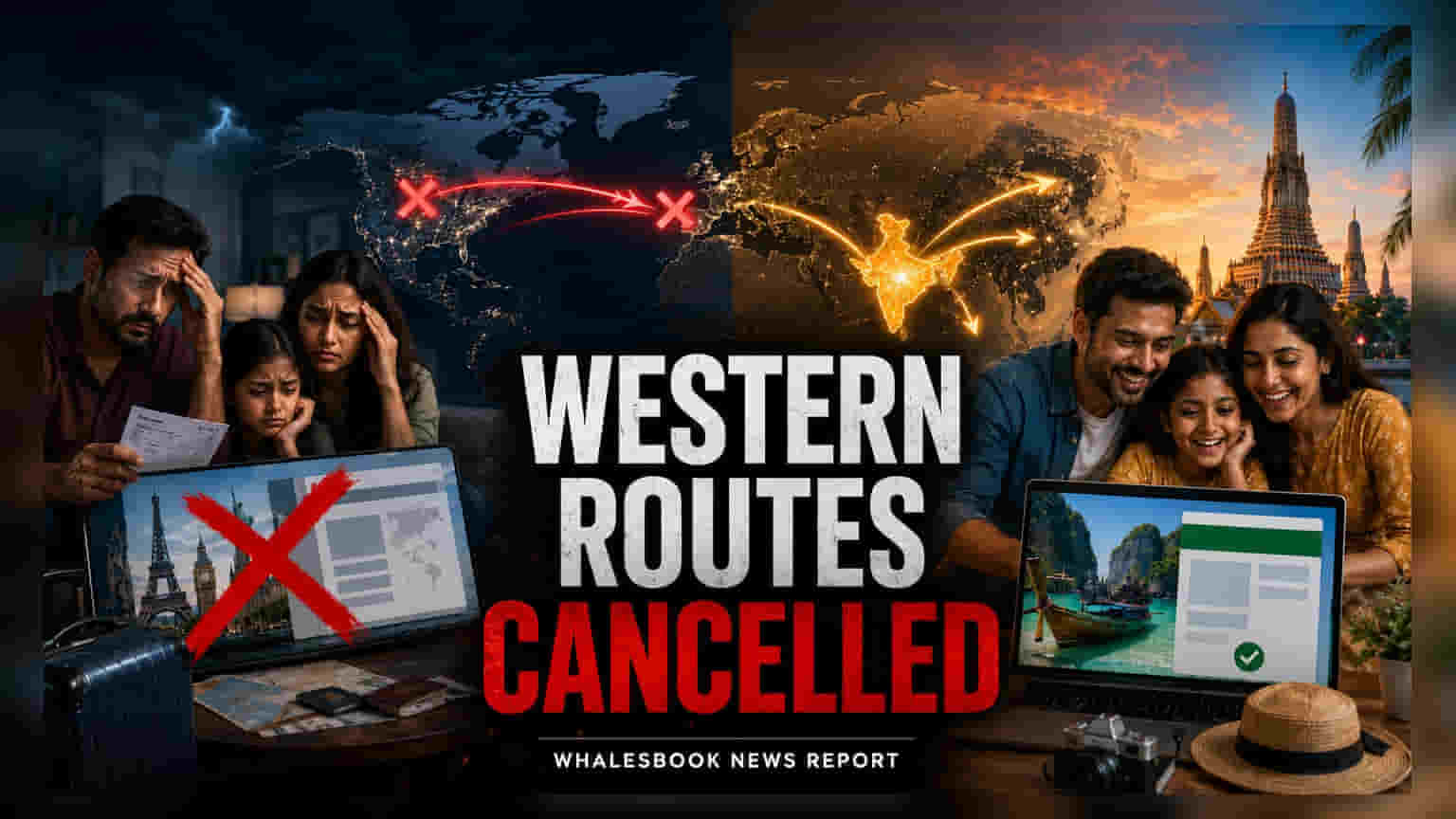

The Shift in Traveler Economics

The current exodus from traditional Western long-haul markets is not merely a preference for local culture; it is an involuntary reaction to a broken pricing model in international aviation. With trans-continental airfares reaching premiums that render the traditional European summer vacation prohibitively expensive for the middle-to-upper-tier Indian demographic, the market is witnessing a fundamental compression in travel distance. Carriers and tour operators are seeing yield dilution on long-haul routes as demand softens, forcing a reliance on high-volume, lower-margin regional traffic to Southeast Asia and domestic hidden gems.

The Operational Realignment

Companies like Thomas Cook (India) are actively recalibrating their inventory to accommodate this migration. The surge in demand for short-haul markets—specifically the Philippines, Vietnam, and Thailand—has created a liquidity trap for operators heavily invested in European or American logistics. Meanwhile, the domestic sector is absorbing this displaced capital. The triple-digit booking growth seen in secondary Indian destinations, such as Jaisalmer, reflects a broader trend where travelers are opting for experiential, spiritual, or niche leisure travel that can be accessed without the friction of multi-leg, high-cost international itineraries. This shift benefits domestic hotel chains and regional logistics providers at the expense of international airlines struggling with fleet availability and fuel price pass-throughs.

Structural Weaknesses and Sector Risks

While the surge in domestic travel provides a buffer, it masks deep-seated structural issues in the Indian tourism infrastructure. The extreme concentration of visitors in northern hill stations and primary leisure spots like Goa has resulted in localized overcrowding and service degradation, which creates a significant risk of brand erosion for hospitality providers. Furthermore, the reliance on spiritual and seasonal tourism creates high volatility in revenue cycles. Unlike diversified global travel conglomerates that benefit from year-round multi-regional operations, Indian operators focusing heavily on domestic spikes are vulnerable to sudden shifts in regional weather patterns or localized infrastructure failures. The current pricing environment for travel services is also dangerously close to a ceiling; any further inflationary pressure on fuel or labor will likely lead to rapid demand destruction as the discretionary income of the average traveler remains under pressure from persistent domestic inflation.

The Future Outlook

Market consensus suggests that the current trend toward regionalization will persist through the fiscal year as airlines continue to grapple with high operational expenses. Industry analysts anticipate that until global aviation capacity stabilizes and long-haul ticket pricing reconciles with purchasing power parity, the structural pivot toward Southeast Asian and domestic hubs will remain the primary growth engine for the travel and tourism sector. Operators that fail to optimize their offerings for these shorter, more frequent trips will likely see continued margin compression.