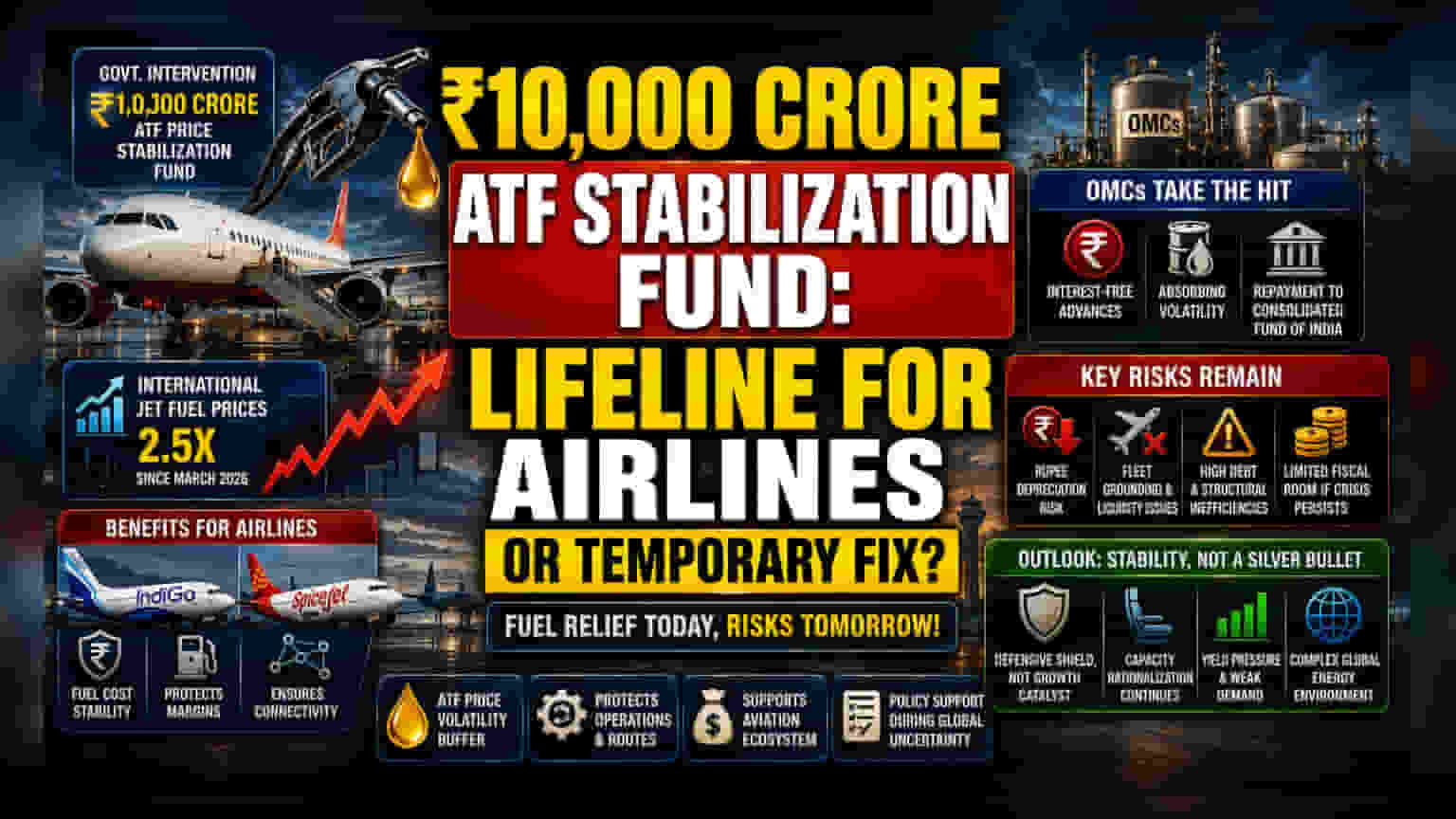

The Structural Pivot in Aviation Finance

The creation of a Rs 10,000 crore ATF Price Stabilization Fund marks a departure from purely market-linked fuel pricing for the Indian aviation sector. By providing interest-free advances to oil marketing companies (OMCs), the government is effectively creating a buffer against the 2.5-fold increase in international jet fuel prices observed since March 2026. This intervention is designed to decouple domestic operational viability from extreme geopolitical premiums, ensuring that carriers—which have recently faced EBITDAR margin compression into single digits—can maintain connectivity without aggressive fare hikes.

The Refiner-Airlines Balancing Act

While this initiative offers a lifeline to carriers like IndiGo and SpiceJet, it recalibrates the risk profile within the energy value chain. State-owned OMCs, already managing the domestic fuel price freeze, are now tasked with the heavy lifting of absorbing volatility. Because these refiners are often mandated to prioritize macro-economic stability over immediate quarterly profitability, this move could lead to sustained under-recovery in their downstream segments. The recovery mechanism, which stipulates that funds will be repaid to the Consolidated Fund of India once global prices normalize, essentially establishes a revolving credit facility for the aviation industry, backed by the taxpayer.

The Forensic Risk Assessment

The aviation sector remains in a fragile state despite this cash injection. A primary risk factor is the continued depreciation of the rupee, which exacerbates costs for aircraft leasing, maintenance, and foreign airport charges—expenses that this ATF fund does not cover. Furthermore, the operational capacity of carriers like SpiceJet, which has faced significant fleet grounding and liquidity constraints in recent quarters, remains highly vulnerable. There is a distinct risk that even with subsidized fuel, structural inefficiencies such as high debt loads and older fleet profiles will continue to drag on profitability. Investors should also be wary of the potential for 'policy fatigue' if the West Asia conflict persists beyond the expected duration, as the fiscal room to keep topping up this fund is not infinite.

Sector Outlook and Operational Reality

For the near term, the focus shifts to how airlines utilize this predictability. While the fund prevents the 'worst-case' scenario of widespread grounding, it does not solve the fundamental issue of yield pressure in a hyper-competitive, price-sensitive market. Capacity rationalization remains the dominant trend, with major carriers already cutting back on non-viable domestic and international routes to preserve cash. The stabilization fund should be viewed as a defensive shield for the sector rather than a catalyst for explosive earnings growth, as any improvement in margins will likely be dampened by sluggish demand and the ongoing costs of navigating a complex global energy environment.