Safe Passage, Lingering Concerns

The recent safe passage of two Indian-flagged LPG tankers through the Strait of Hormuz offers a brief respite from immediate supply worries. However, this event occurs amid heightened geopolitical tensions that expose underlying weaknesses in India's energy import strategy, highlighting ongoing vulnerabilities and imposing significant costs on the nation's economy.Rising Costs Amid Tensions

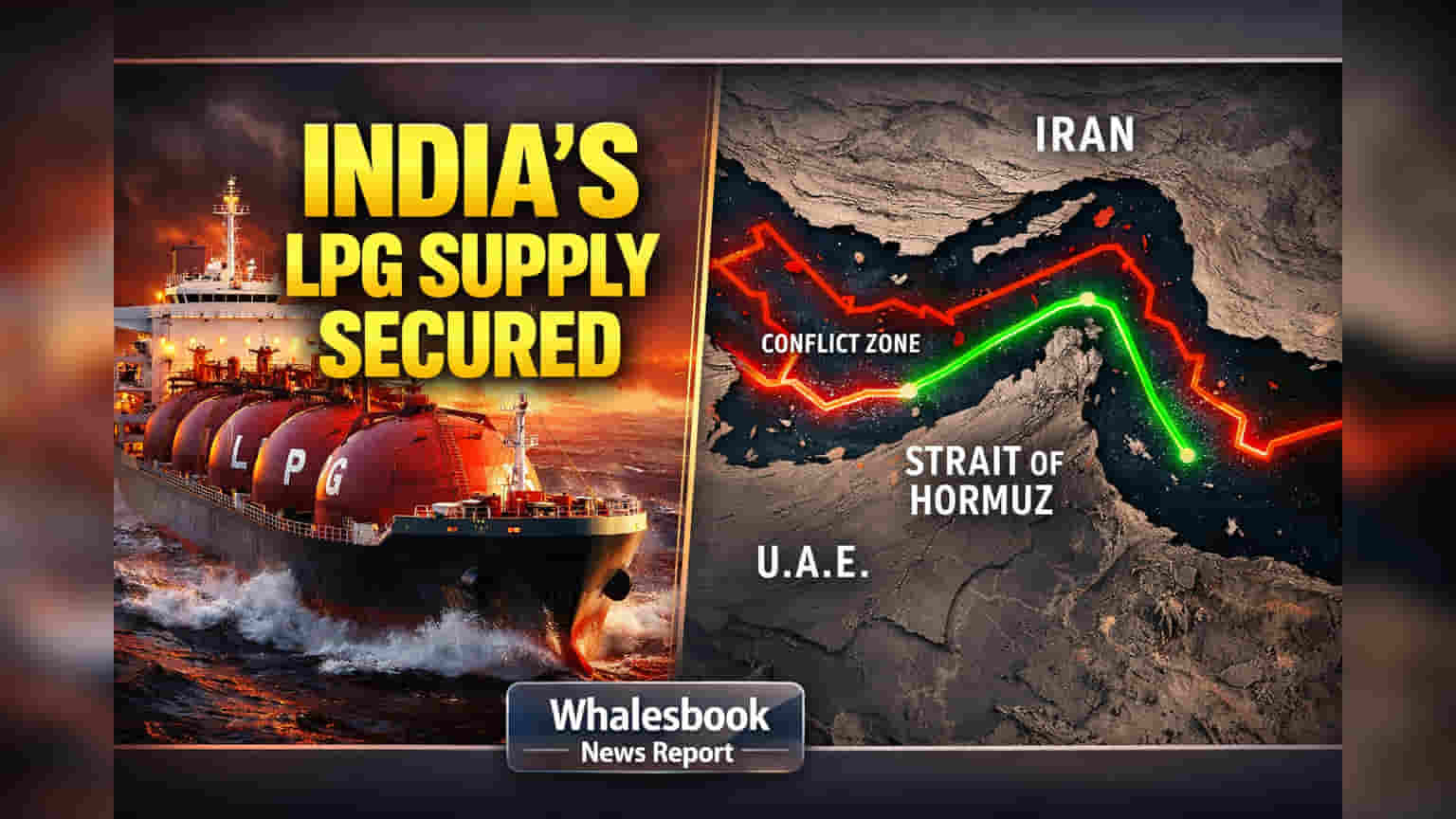

The successful navigation of the Strait of Hormuz by LPG tankers Pine Gas and Jag Vasant, carrying roughly one day's national supply of cooking gas, is a tactical win. Yet, this achievement is overshadowed by surging global energy transit costs. Brent crude prices have climbed past $110 per barrel, driven by conflict in West Asia, a level not seen since early 2022. This reflects a significant geopolitical risk premium that has inflated shipping and marine insurance costs. Despite the transit, the broader market remains under pressure from constraints on this vital waterway.Geopolitical Tightrope and Verification Costs

Iran's approach to the Strait of Hormuz now involves a vetting and registration system for vessels. India is in direct talks with Tehran to ensure passage, reportedly requiring detailed disclosure of vessel ownership and cargo to Iran's Islamic Revolutionary Guard Corps (IRGC). Evidence suggests some vessels may have paid fees, possibly millions of dollars, to transit Iranian waters via a designated corridor. This process adds direct financial costs and complex diplomatic maneuvers, turning transit into a negotiation.India's Persistent Dependency

India's energy security is significantly exposed due to its reliance on imports via the Strait of Hormuz. Around 80-85% of its LPG imports, mainly from the Gulf, pass through this chokepoint. Unlike crude oil, India lacks strategic LPG reserves, making it highly vulnerable to supply disruptions. While crude oil imports transit Hormuz at figures between 40% and over 60%, and sourcing nations have expanded to around 40, the critical LPG segment remains highly concentrated. Efforts to increase domestic LPG production by roughly 25-36% and secure imports from countries like Argentina and the US are underway but may not fully offset the scale of dependency.Regional Energy Security Strategies

Across Asia, nations face similar dependencies and are speeding up diversification. China is seeking alternative sources and boosting domestic production while managing its own reliance on Gulf oil. Japan and South Korea, highly dependent on Hormuz for oil imports, face acute vulnerability, with Japan relying on the strait for about 90% of its needs. Strategies include increasing renewables and nuclear power, and forging new logistical ties outside the Middle East. However, adapting infrastructure and contracts for major shifts remains a significant long-term challenge.Historical Market Reactions

Persistent geopolitical instability in the Strait of Hormuz has historically caused significant market volatility for Indian energy stocks. In early March 2026, shares of major Oil Marketing Companies (OMCs) like Indian Oil Corporation (IOC), Hindustan Petroleum Corporation (HPCL), and Bharat Petroleum Corporation (BPCL) fell sharply (6-7%) as Brent crude neared $120 per barrel and later exceeded $112. This sell-off was linked to fears of supply disruption and margin pressure on OMCs that absorb higher costs without immediate retail price changes. Minor geopolitical events have often boosted upstream producers while pressuring downstream refiners.Key Risks for India's Energy Sector

Structural Vulnerability: India's reliance on the Strait of Hormuz for a critical percentage of its LPG imports (85-95% of Gulf shipments) means any disruption carries systemic risk. The absence of substantial strategic LPG reserves heightens this weakness. Even with diplomacy, Iran's control over passage introduces uncertainty and potential costs, turning a key trade route into a geopolitical bargaining chip.

Economic Strain: Sustained high oil prices have profound economic repercussions. Each $10 crude price increase could add $13-14 billion to India's annual import bill, widening the current account deficit and pressuring the rupee. State-owned oil marketing companies like IOCL, BPCL, and HPCL have already absorbed significant losses, estimated in the tens of thousands of crores over recent years, to keep retail fuel prices stable. This financial strain can reduce profitability and future investment capacity.

Competitive Weakness & Supply Crunch: While India diversifies crude sources, the LPG supply chain remains a distinct weakness. Import disruptions can cause critical shortages for industrial users, impacting household consumers. Rerouting vessels via longer routes like the Cape of Good Hope, and increased war-risk insurance premiums, further inflate energy import costs, potentially reducing India's product competitiveness.

Geopolitical Entanglement: India's perceived alignment with the US and Israel in the ongoing conflict could complicate diplomatic efforts for favorable passage from Iran. This strategic alignment may indirectly add difficulty in navigating regional sensitivities, especially amid LPG shortages.

Outlook: Persistent Risks and Diversification Challenges

While diplomatic channels are active and India works to secure safe passage for its vessels, the underlying geopolitical risk in the Strait of Hormuz persists. Diversifying energy sources and routes is a long-term, complex trend facing challenges from infrastructure limits, competing global demand, and India's sheer import scale. War-risk premiums and higher freight costs are likely to become a permanent expense for energy imports. Geopolitical tensions are expected to remain the primary driver of sector sentiment, suggesting continued volatility and a focus on energy security strategies.

India LPG Imports: Hormuz Passage Hides Supply Risks, High Costs

TRANSPORTATION

Overview

While Indian-flagged LPG tankers Pine Gas and Jag Vasant successfully navigated the Strait of Hormuz, this isolated event offers limited solace. India's critical reliance on this volatile chokepoint for 80-85% of its LPG imports exposes it to escalating geopolitical risks, increased import costs due to higher war-risk premiums, and potential supply disruptions affecting industrial and household consumers. Despite diversification efforts, the country remains strategically vulnerable, with state-owned oil marketing companies bearing significant financial strain from absorbing rising crude costs.

Disclaimer:This content

is for informational purposes only and does not constitute financial or investment advice. Readers

should consult a SEBI-registered advisor before making decisions. Investments are subject to market

risks, and past performance does not guarantee future results. The publisher and authors are not liable

for any losses. Accuracy and completeness are not guaranteed, and views expressed may not reflect the

publication’s editorial stance.