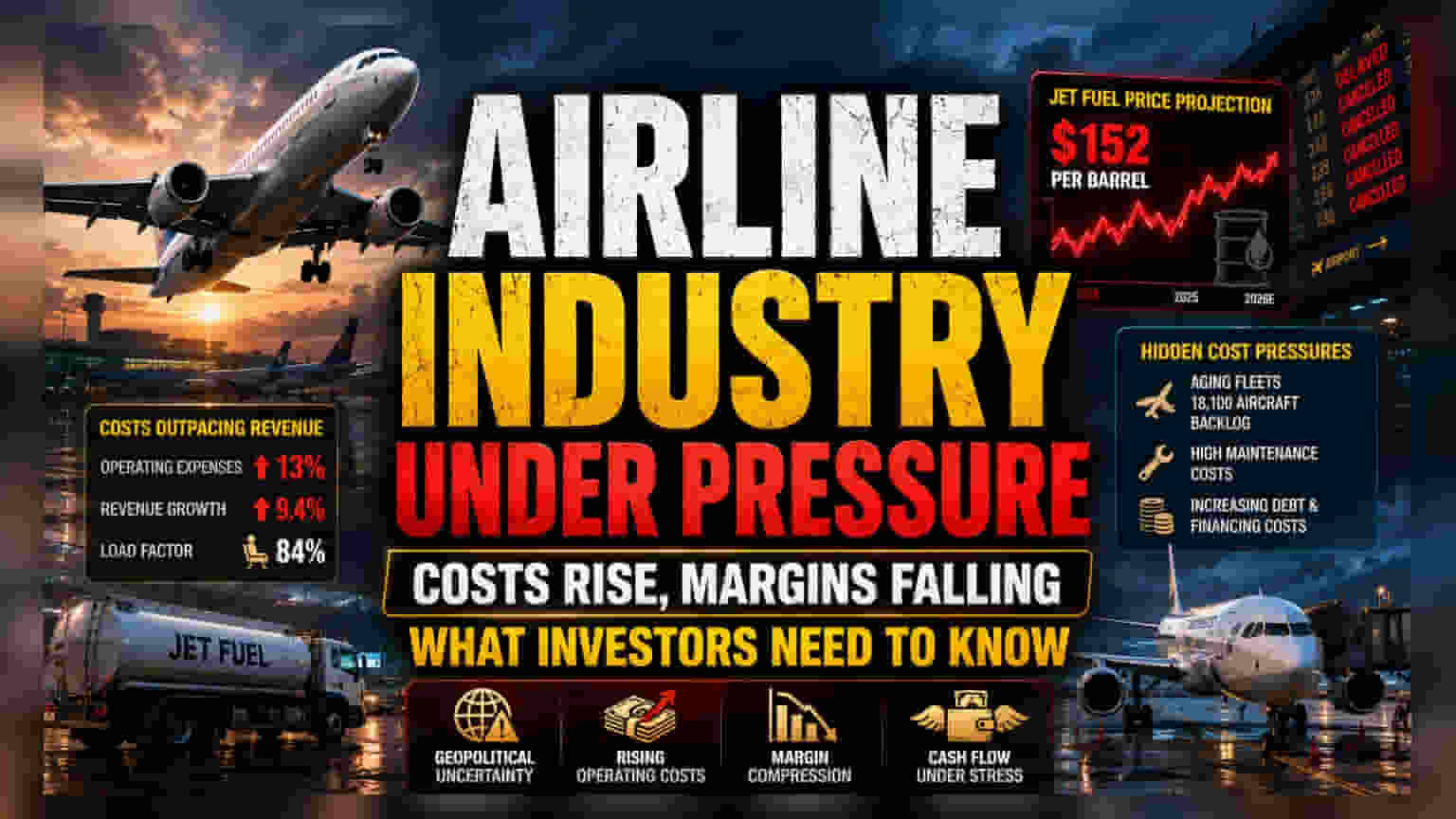

The Structural Margin Squeeze

The narrative of resilient post-pandemic travel is colliding with the reality of an unforgiving cost structure. While top-line revenue growth suggests industry health, the underlying economics reveal a deteriorating environment where even record-breaking load factors of 84% cannot offset the inflationary pressure on operating inputs. The industry is currently trapped in a cycle where operational overhead—specifically the 13% spike in expenditures—is fundamentally decoupling from the 9.4% revenue expansion, creating a widening structural gap that threatens long-term equity valuations across the sector.

The Geopolitical and Fuel Multiplier

The projection of $152 per barrel for jet fuel acts as a direct tax on carrier earnings, stripping away the efficiency gains companies achieved through fleet modernization. Unlike prior cycles where airlines could hedge against such volatility, the current persistence of conflict in the Middle East removes the predictability required for long-term fuel hedging strategies. This uncertainty forces management teams to prioritize liquidity over capital expenditure, stalling the rollout of more fuel-efficient, next-generation aircraft. The market is now factoring in a risk premium that weighs heavily on carriers with high debt-to-equity ratios, as the cost of financing new assets rises in tandem with operating costs.

The Forensic Bear Case

The industry's reliance on secondary revenue streams and elevated fares to drive its $1.165 trillion revenue forecast faces a significant elasticity risk. If the global economy experiences even a moderate cooling, discretionary travel spending will be the first to contract, leaving carriers with high fixed costs and limited ability to adjust capacity. Furthermore, the persistent reliance on aging fleets—driven by a massive 18,100-unit backlog—creates a hidden liability in the form of increased maintenance-to-revenue ratios. Carriers that delayed fleet turnover are now facing an unsustainable climb in 'A-Check' and 'C-Check' maintenance costs, which are rarely captured in surface-level revenue reports but exert a direct, negative drag on free cash flow.

Future Outlook and Sector Resilience

Analysts are watching for further downward revisions to earnings per share (EPS) guidance as carriers digest the impact of these elevated costs. While North American and European operators maintain a wider cushion than their Middle Eastern counterparts, the trend toward margin normalization is likely to persist through the remainder of the year. Investors are pivoting away from simple passenger growth metrics, focusing instead on CASM (Cost per Available Seat Mile) and the ability of management to maintain unit revenue yield in an environment of constrained consumer spending.