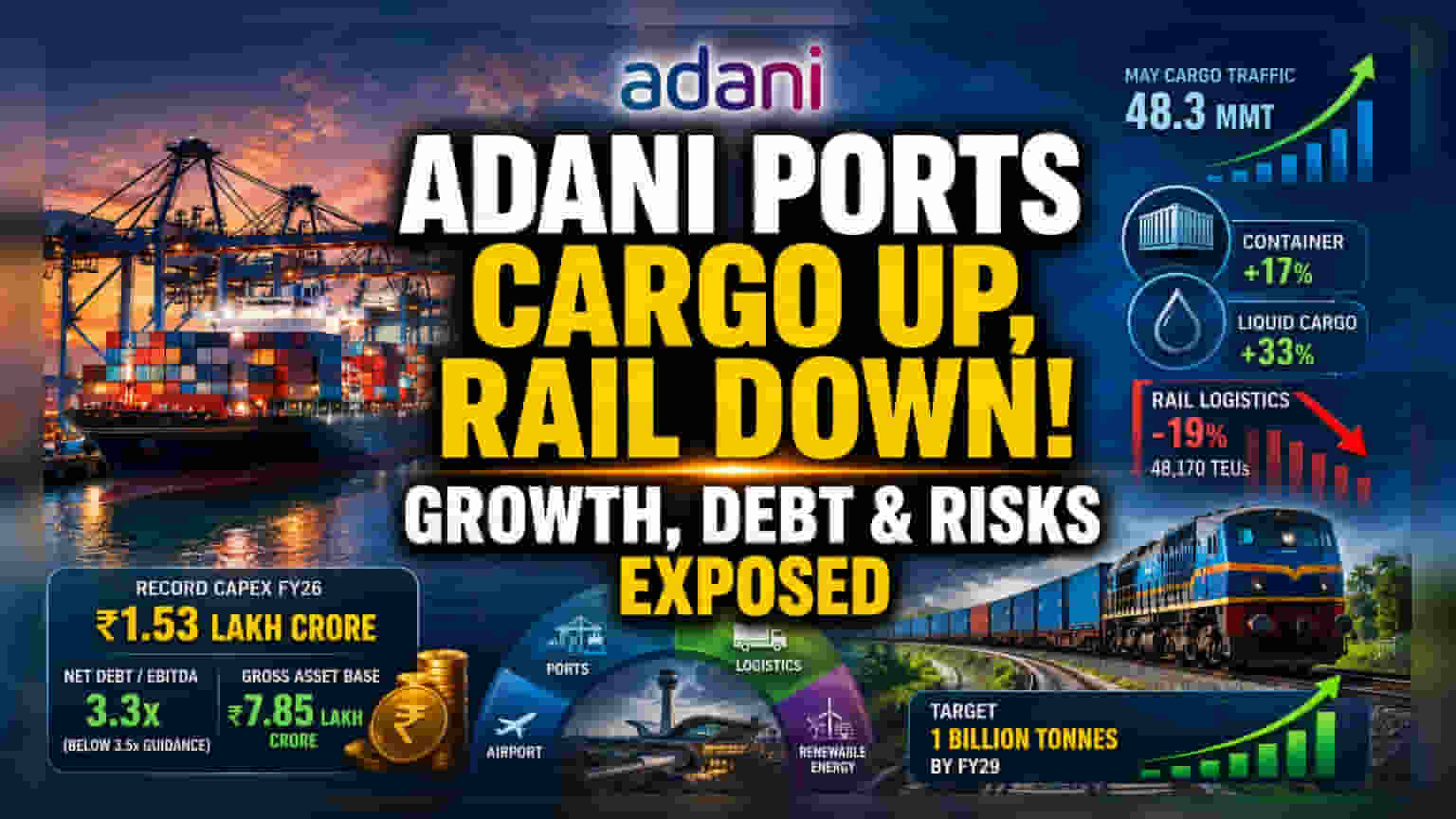

The Cargo Growth Divergence

The recent announcement of 48.3 million metric tonnes (MMT) in May cargo traffic highlights a clear divide in operational performance. While container volumes climbed 17% and liquid cargo surged 33%, the company’s rail logistics segment remains a point of concern. Reporting a 19% year-on-year drop to 48,170 TEUs, this marks the second straight month of contraction for the rail unit. Because rail freight typically commands higher per-unit margins compared to standard port handling, this persistent weakness could exert pressure on blended EBITDA margins in the coming quarters if the volume trend does not reverse.

Scaling Infrastructure Amid Capex Cycles

Adani Ports’ expansion strategy is entering a capital-intensive phase. The broader Adani portfolio recently disclosed a record-breaking FY26 capital expenditure of ₹1.53 lakh crore, the largest annual outlay by an Indian corporate entity. While this aggressive spending has elevated the conglomerate's gross asset base to over ₹7.85 lakh crore, the market is closely watching how these assets—including recent additions like the Navi Mumbai International Airport and various renewable energy projects—will contribute to cash flow starting in FY27. The company's ability to maintain a net debt-to-EBITDA ratio of 3.3x, staying below its 3.5x guidance, remains a critical metric for institutional investors monitoring leverage risk during this growth cycle.

The Forensic Bear Case

Despite the bullish sentiment from major brokerages, potential structural headwinds persist. The Vizhinjam port project, intended to be a transshipment hub, has historically faced significant operational delays and social friction, including long-standing protests from local fishing communities and environmental concerns regarding coastal erosion. Furthermore, while the company has been designated a 'Large Corporate' with a stable AAA rating, it remains sensitive to the broader economic environment and sector-specific risks. Critics point to the stock's valuation, which trades at a significant premium compared to book value, and note that regulatory scrutiny can emerge rapidly for highly leveraged infrastructure conglomerates. Any further deceleration in high-margin logistics volumes could force a re-evaluation of current price targets if growth does not offset the heavy debt-servicing load required for such massive expansion projects.

Future Outlook and Guidance

Looking ahead, market consensus remains cautiously optimistic, with recent brokerage notes citing the company's integrated logistics network as a defensive moat. Management has set an ambitious target for cargo handling, aiming for 1 billion tonnes by FY29. With average borrowing costs declining to 7.8% in FY26, the company is attempting to optimize its capital structure while scaling its international footprint in regions like Israel and Tanzania. The market will be watching the next quarterly results for evidence that the uptick in port cargo can compensate for the ongoing sluggishness in the rail-linked logistics segment.