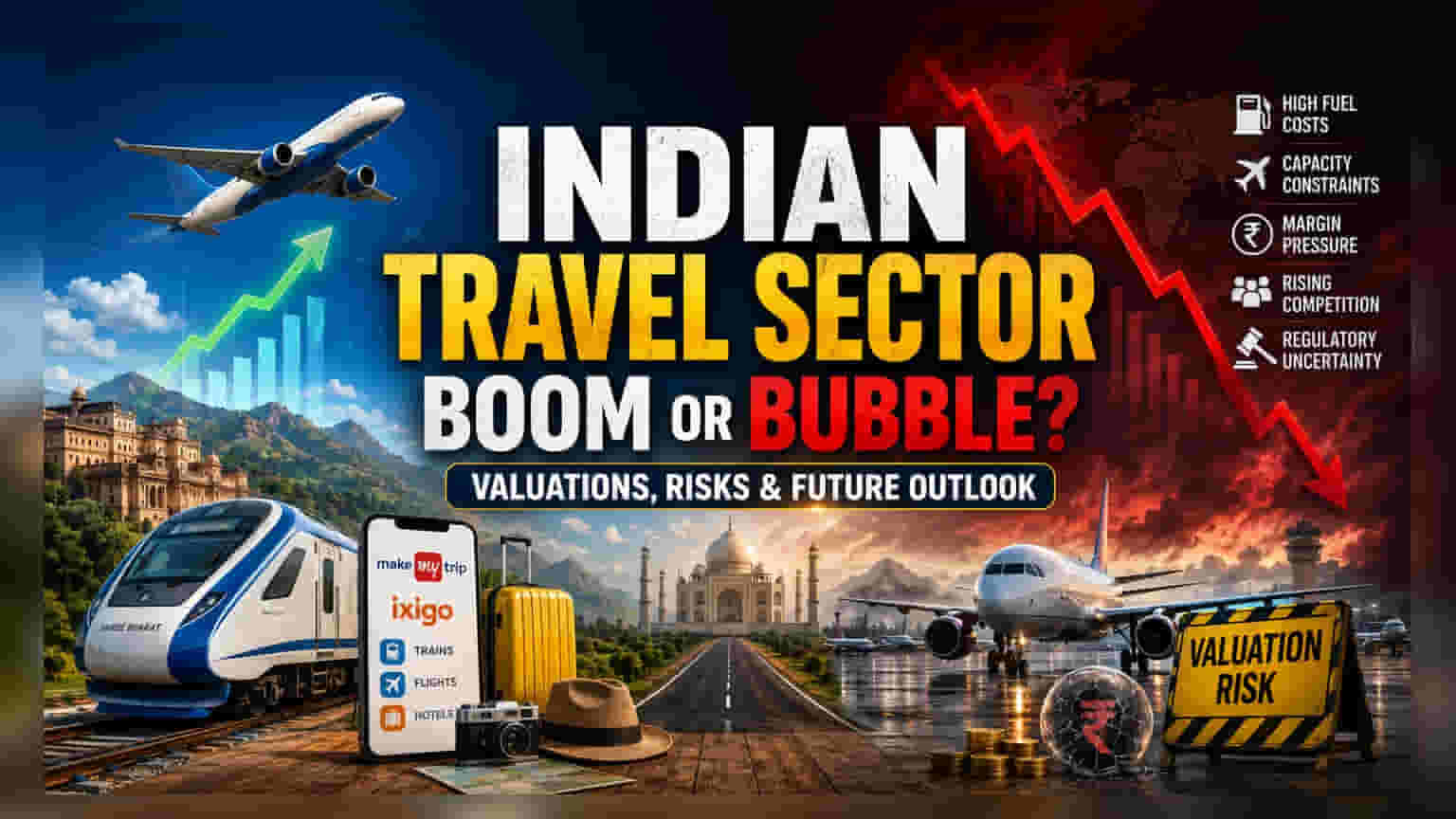

The Valuation Gap and Market Dynamics

The resilience of the Indian travel sector amidst a cost-of-living squeeze reveals a significant structural pivot. While international flight demand has softened due to higher operational costs and geopolitical regional conflicts, domestic activity has filled the gap. Major platforms like MakeMyTrip and ixigo have reported this shift in consumer behavior, where vacationers increasingly opt for intercity road travel and railway bookings over expensive long-haul flights. This substitution is not merely a reaction to current volatility but a reflection of the evolving travel appetite among India’s expanding middle class, which now prioritizes accessibility and predictability over premium, high-risk international ventures.

The Operational Reality of Rising Costs

Airfares have seen a 30-40% annual increase, driven largely by elevated aviation turbine fuel (ATF) prices and constrained fleet capacity. Airline capacity reductions across major domestic and international routes have created a supply-demand imbalance, further pushing ticket prices upward. Consequently, while overall travel intent remains strong—with 60% of Indians planning domestic holidays this year—the composition of this spending is shifting. Budget-conscious travelers are increasingly gravitating toward 'value-driven' destinations such as Vietnam, Sri Lanka, and Thailand, which have seen growth rates as high as 130% year-on-year, effectively displacing previously popular but now cost-prohibitive destinations in Japan and Indonesia.

The Forensic Bear Case

Despite the apparent growth in domestic bookings, the travel tech ecosystem faces mounting headwinds. The dependence of platforms like ixigo on IRCTC railway partnerships exposes them to potential regulatory shifts or commission compression, which would directly impact their customer acquisition cost (CAC) advantage. Furthermore, the high P/E valuations of major travel players, currently trading in the 70x-90x range, suggest that investors have priced in aggressive growth expectations that may be unsustainable if margin compression persists. Airline capacity remains a significant bottleneck; as long as fleets remain grounded due to supply chain issues and fuel costs stay elevated, take-rates for online travel agencies (OTAs) in the air ticketing segment will face persistent downward pressure. Additionally, competitive intensity is rising, with firms like Cleartrip aggressively entering the rail segment, threatening to fragment the market and dilute the incumbent lead of established platforms.

Future Outlook

The shift toward domestic tourism appears structurally anchored by government initiatives like Swadesh Darshan 2.0 and the modernization of religious and cultural corridors. While near-term aviation revenue remains volatile due to geopolitical stressors, the long-term outlook for the Indian travel sector remains anchored by 5-6% projected CAGR growth through 2034. Institutional focus remains on how these platforms manage the transition from simple utility-based booking to value-added service models to sustain profitability in an environment of high operational costs and thinning margins.