The Shift to Sustainable Margins

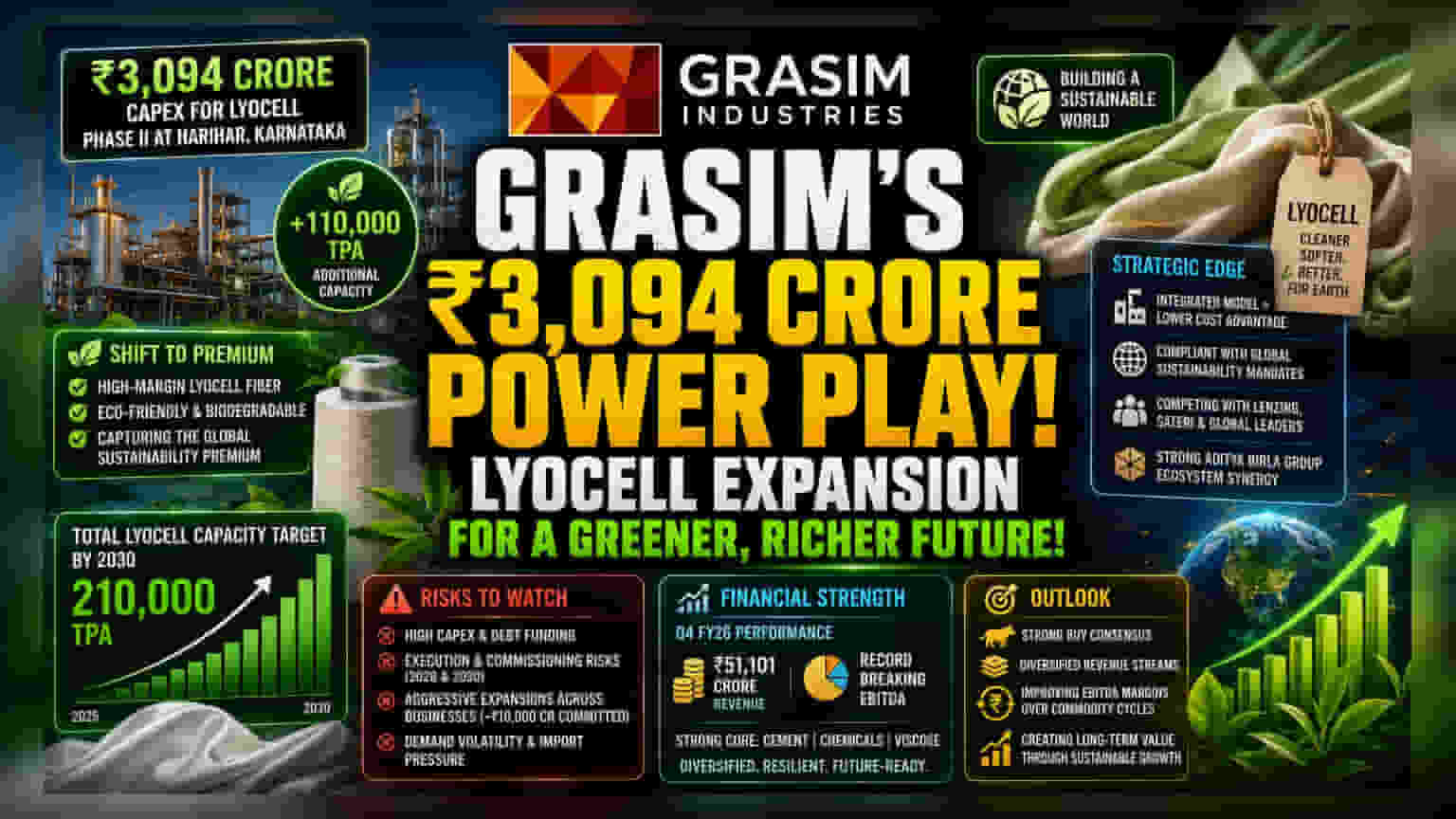

Grasim Industries is betting heavily on the premiumization of its textile division. By greenlighting a ₹3,094 crore capital expenditure for Phase II of its Lyocell production at Harihar, Karnataka, the company is signaling a transition from high-volume, commodity-sensitive viscose to high-margin, eco-friendly textile materials. With the global appetite for biodegradable, closed-loop fibers rising, this capacity addition—an incremental 110,000 tonnes per annum—positions the firm to capture the 'green premium' currently dominated by international players like Lenzing AG.

Strategic Competitive Positioning

Unlike standard viscose staple fiber (VSF) production, which remains vulnerable to raw material volatility, Lyocell production aligns with long-term European and American sustainability mandates. The company’s integrated business model provides a unique moat; by leveraging its existing chemical and pulp manufacturing infrastructure, Grasim keeps input costs controlled while scaling its premium output. Competitors like Sateri and Lenzing have long held the lead in this segment, but Grasim’s entry with a total projected 210,000 tonnes capacity by 2030 aims to fundamentally alter the regional supply chain landscape. This expansion also complements the broader Aditya Birla Group portfolio, which has recently seen record-breaking EBITDA performance in its building materials and chemical segments during FY26.

The Forensic Bear Case

Despite the growth narrative, the expansion is not without structural friction. The project, spread over multiple years with commissions slated for 2028 and 2030, exposes the company to significant execution risks and interest rate sensitivity, given that the investment is partly debt-funded. Furthermore, Grasim is currently navigating an aggressive expansion cycle, having committed approximately ₹10,000 crore to its 'Birla Opus' decorative paints division. Investors are closely watching whether the combined capital allocation strategy—balancing new market entries with legacy fiber upgrades—will compress free cash flow. Additionally, the textile sector has faced headwinds from dumping by neighboring countries and slowing discretionary spending, which could pressure realization rates for fibers if demand does not keep pace with the projected capacity increase.

Forward Outlook

Analysts remain generally bullish, with a 'Strong Buy' consensus reflecting confidence in the company’s ability to diversify revenue streams. The market is pricing in the strength of Grasim’s core cement and chemical divisions, which reported record revenues of ₹51,101 crore in Q4 FY26. However, the success of this fiber-specific capex will be judged by its ability to insulate the firm from future commodity cycles and improve segmental EBITDA margins, which remain the critical performance metric for long-term valuation.