The Capital Allocation Dilemma

The decision to prioritize a substantial cash infusion into Tata Teleservices reflects a defensive posture designed to mitigate systemic risk rather than a pivot toward growth. By absorbing the first major tranche of Adjusted Gross Revenue (AGR) liabilities, Tata Sons is effectively ring-fencing the subsidiary to avoid regulatory default. This capital requirement arrives as the conglomerate simultaneously manages aggressive burn rates across its high-priority portfolios, specifically within the aviation and consumer digital segments. Unlike growth-oriented investments, this allocation serves as a balance-sheet stabilizer for an asset that remains sidelined from the mainstream mobile consumer market.

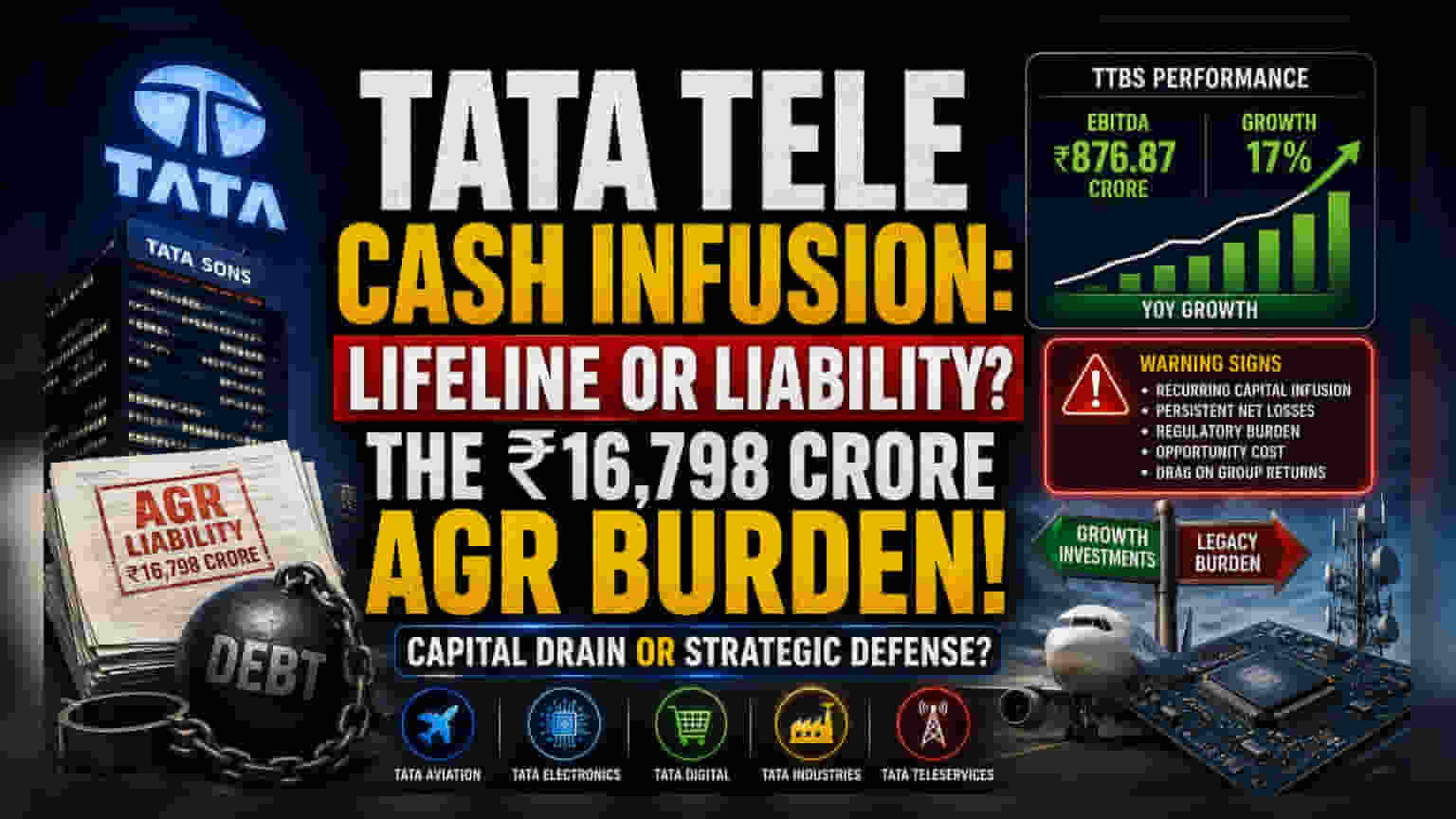

Operational Reality vs. Legacy Burden

While the enterprise-focused Tata Tele Business Services (TTBS) managed a 17% year-over-year increase in EBITDA to ₹876.87 crore, the firm remains hamstrung by its historical financial architecture. The reliance on parent-level equity support underscores a lack of self-sustaining cash flow capable of servicing the ₹16,798 crore total AGR liability. This reliance stands in stark contrast to the competitive dynamics seen with peers like Vodafone Idea, which utilized equity dilution to the government as a survival mechanism. By rejecting that path, Tata Sons has signaled a preference for absolute control, even at the cost of continuous capital drain.

The Forensic Bear Case

The structural health of Tata Teleservices remains questionable when evaluated against the group's broader ambitions. The recurring nature of these capital injections risks creating a "zombie asset" scenario, where parent capital is diverted from high-growth ventures like Tata Electronics—which is currently positioned to capture semiconductor tailwinds—to patch balance sheets in mature, stagnant sectors. Furthermore, the persistence of net losses, even after adjusting for exceptional charges, suggests that the underlying business model is not sufficiently capturing value in the enterprise data market to offset its regulatory cost base. Investors tracking the parent entity should view this as a clear indication that the conglomerate is willing to subsidize non-performing units for extended periods, potentially impacting return on invested capital metrics for the broader group.

Future Outlook and Board Scrutiny

With the upcoming board session on June 12, the conglomerate faces a narrowing window for fiscal rationalization. Management is under pressure to move beyond mere sustenance for its loss-making subsidiaries. The path forward likely involves an attempt to leverage the enterprise infrastructure of TTBS to improve operational margins further, but with a total liability profile spanning the next five years, the subsidiary is expected to remain a drag on the group's consolidated bottom line for the foreseeable future.