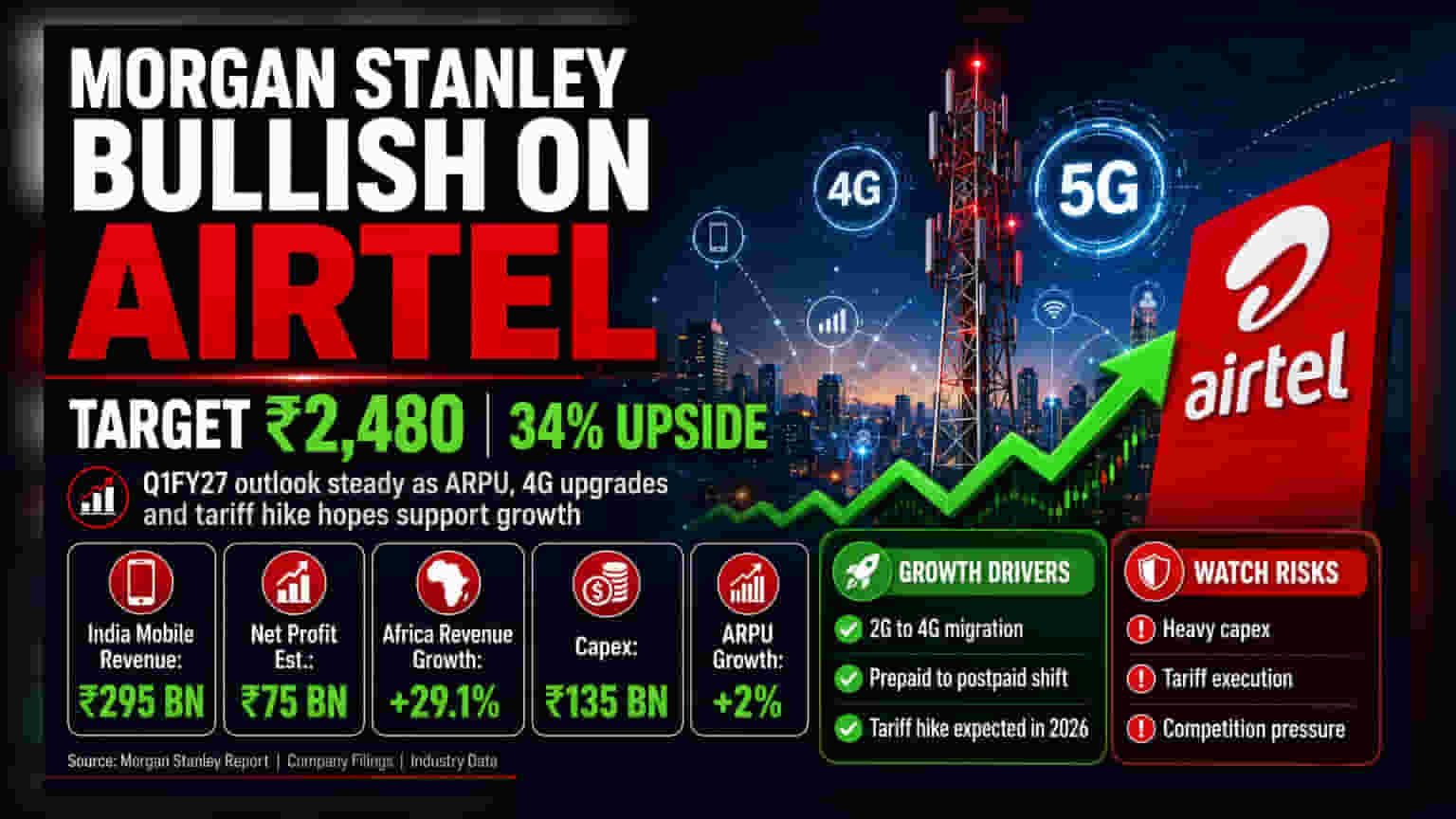

Morgan Stanley has maintained a positive outlook on Bharti Airtel, projecting a potential 34% upside with a target price of ₹2,480. The brokerage highlights that subscriber upgrades and expected industry-wide tariff hikes later in the year are key growth drivers for the telecom operator's upcoming quarterly performance.

What Happened

Morgan Stanley has released a report on Bharti Airtel, maintaining a positive view on the stock with a price target of ₹2,480. This implies a 34% potential increase from recent levels. The brokerage expects the telecom giant to show steady performance in the June quarter (Q1FY27). According to the report, the main reasons for this positive outlook are the ongoing trend of users upgrading from 2G to 4G networks, the shift from prepaid to postpaid plans, and the expectation of a tariff hike—an increase in customer plan prices—planned for later in 2026.

Financial Projections for Q1

For the June quarter, the brokerage estimates Bharti Airtel's India mobile business revenue to grow by 7.8% year-on-year, reaching ₹295 billion. A key metric investors track is the average revenue per user, or ARPU, which is the amount the company earns from each subscriber. Morgan Stanley expects this to rise by 2%, driven by the move toward higher-value plans.

The report also projects a consolidated net profit of ₹75 billion for the quarter. The Africa operations are expected to contribute significantly, with revenue projected to jump by 29.1% year-on-year to $1,827 million, supported by favorable currency movements in markets like Nigeria and Zambia.

Growth Beyond Mobile Services

While mobile services are the core business, the report highlights that other areas of Bharti Airtel are growing even faster. The company’s non-mobile segments—which include home broadband, enterprise solutions, and DTH services—are expected to see a revenue compound annual growth rate (CAGR) of 19% between FY26 and FY29. This is higher than the 12% growth rate expected for the India mobile business over the same period. This suggests the company is successfully diversifying its income streams.

The Capex and Investment Question

Investors should pay close attention to the company's capital spending, often called capex. Morgan Stanley estimates the consolidated capital expenditure for the company at ₹135 billion for the quarter. A large portion of this spending is directed toward the Indian core business, specifically for data center expansion and the company's new NBFC (non-banking financial company) business.

While expansion is necessary for long-term growth, heavy spending requires constant monitoring. High levels of investment can impact short-term cash flow, and investors typically watch whether these investments eventually deliver the expected returns without putting too much pressure on the company's balance sheet.

Risks and What To Watch Next

While the outlook is positive, the telecom sector in India faces several challenges that investors should consider. Competition between the major players remains intense, and pricing discipline is necessary for tariff hikes to be successful. Any delay in executing these planned price increases or a slower-than-expected subscriber migration to 4G could impact the projected growth.

Going forward, the key monitorables will be the actual execution of the expected tariff hikes later in the year, the progress of the company's diversification into areas like the NBFC business, and the ability to maintain profit margins amid heavy capital spending. Investors should also watch for management commentary on the pace of 5G adoption and data monetization in the upcoming earnings call.