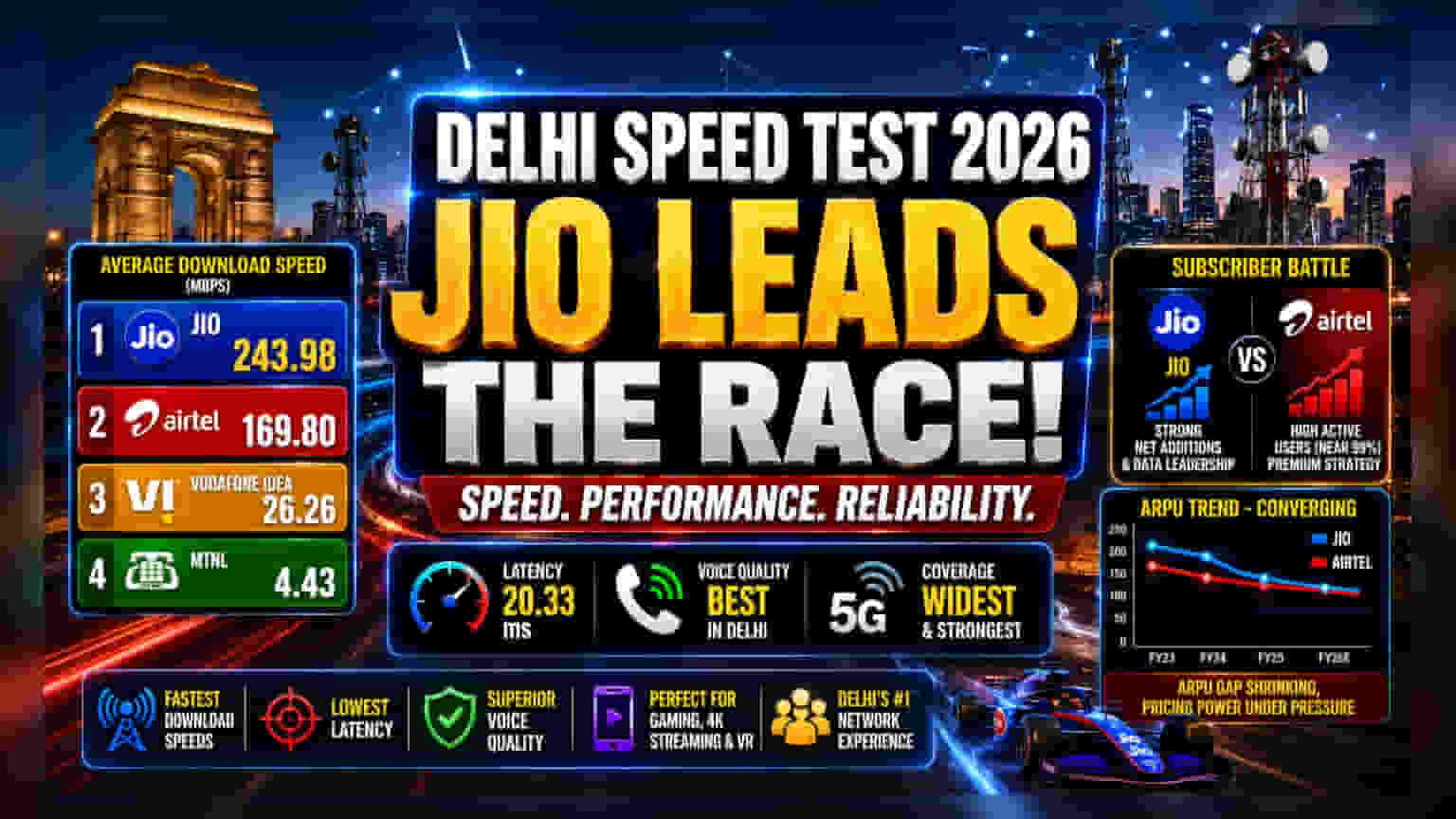

Network Dominance and the Latency Edge

Recent drive tests commissioned by the Telecom Regulatory Authority of India (TRAI) confirm that Reliance Jio continues to command the technical high ground in the Delhi Licensed Service Area. The April 2026 assessment underscores a significant performance gap, with Jio achieving average download speeds of 243.98 Mbps. In contrast, Bharti Airtel trailed at 169.80 Mbps, while Vodafone Idea and MTNL recorded speeds of 26.26 Mbps and 4.43 Mbps, respectively. Beyond sheer throughput, Jio’s 20.33 ms latency provides a crucial edge for high-bandwidth, real-time applications, positioning the carrier as the preferred network for the capital’s data-heavy user base.

The Quality vs. Quantity Trade-off

While Jio excels in laboratory-grade drive tests, the broader Indian telecom market presents a more complex narrative. Recent subscription data reveals that Bharti Airtel frequently challenges Jio in terms of net subscriber additions and active user engagement. Airtel’s network strategy focuses on high-quality subscriber acquisition, maintaining an exceptional active user ratio—often hovering near 99%—which suggests a loyal customer base that prioritizes reliability over raw speed metrics. For investors, this creates a divergent valuation thesis: Jio functions as the infrastructure and capacity leader, whereas Airtel leverages its high active-user efficiency to drive premiumization and maximize revenue per user.

The Forensic Bear Case: Structural Risks

Despite the recent win, the sector faces substantial headwinds. Vodafone Idea, despite struggling in technical performance metrics, continues to capture market interest as a high-volatility play, yet its financial sustainability remains questionable compared to its larger peers. Furthermore, the industry-wide push for higher Average Revenue Per User (ARPU) is nearing an inflection point. Analysts note that as prepaid and postpaid ARPU levels converge, the ability to pass on price hikes to consumers is diminishing. Reliance Industries, while bolstered by its digital and telecom moat, must contend with a broader macroeconomic environment where high interest rates and capital expenditure requirements for 5G and future 6G development continue to weigh on balance sheets. If the 'network effect' is diluted by aggressive pricing aimed at chasing short-term ARPU, there is a risk that even top-tier networks could see subscriber churn to budget-conscious alternatives.

Future Outlook and Sector Trajectory

Looking toward the remainder of FY26, the battle for Delhi and the wider Indian market will likely pivot from raw speed to service monetization. While Jio’s lead in speed and voice quality provides a defensive moat, the real value for stakeholders will be determined by how effectively these firms transition from pure connectivity to digital service ecosystems. Consensus among market participants suggests that as the 5G rollout matures, profitability will increasingly rely on sticky, value-added services rather than the mere volume of wireless additions.