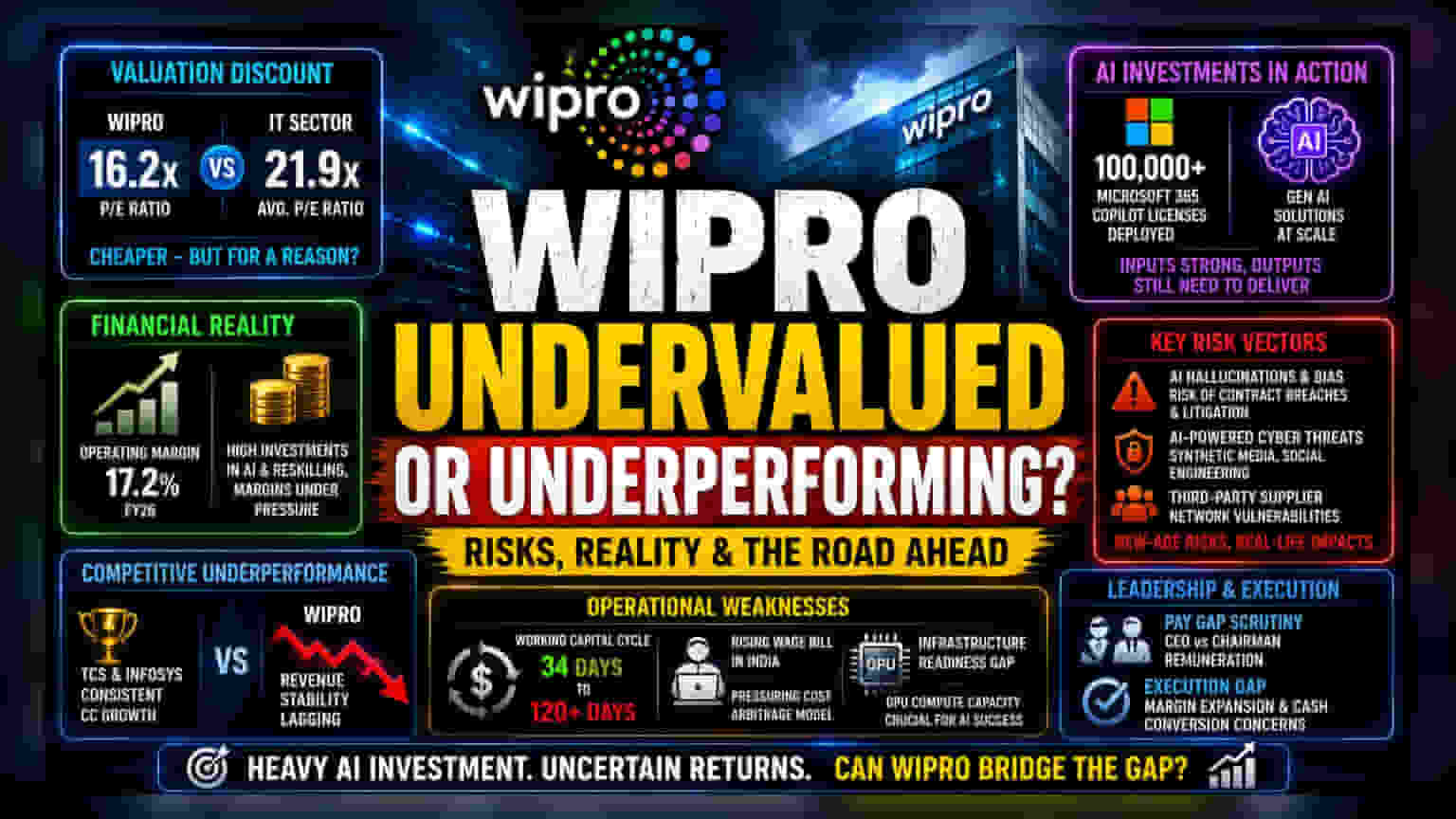

The Valuation and Operational Gap

Wipro’s recent performance reflects a firm caught in a transition. While the company maintains a valuation discount compared to the broader IT sector—trading at a P/E ratio of approximately 16.2x against an industry average hovering near 21.9x—this 'value' positioning is increasingly viewed through the lens of structural caution. Despite successful initiatives to scale generative AI, including the deployment of over 100,000 Microsoft 365 Copilot licences, the tangible conversion of these inputs into high-margin economic output remains a hurdle. The firm's operating margins for FY26 stood at 17.2%, illustrating the struggle to maintain profitability while simultaneously investing heavily in proprietary AI solutions and reskilling its workforce.

The Forensic Risk Landscape

The company’s latest annual report clarifies a shift in the threat model facing traditional IT services. Beyond the well-documented macroeconomic slowdown in the Americas and Europe—which account for roughly 89% of Wipro's revenue—management has spotlighted AI as a primary risk vector. The potential for 'hallucinating' or biased algorithms to result in contractual breaches or client litigation is now considered a significant liability. Furthermore, the escalation of AI-powered cyber threats, such as synthetic media and advanced social engineering, has widened the vulnerability window for both Wipro and its third-party supplier network. Unlike more resilient peers that have successfully transitioned to higher-value consulting-led models, Wipro remains sensitive to discretionary spending cuts, exacerbated by the rising wage bill in India that continues to pressure the traditional cost-arbitrage model.

Competitive Weakness and Leadership Outlook

Unlike industry leaders such as TCS or Infosys, which have demonstrated greater consistency in constant-currency growth, Wipro has faced a period of relative underperformance in revenue stability. Management remuneration structures, which highlight a significant pay gap between the CEO and the Chairman, have also drawn scrutiny as the company navigates this turbulent cycle. Critics point to the fact that while other firms have managed to show margin expansion through rigorous execution, Wipro's working capital cycles have lengthened, moving from roughly 34 days to over 120 days. This trend underscores a potential weakness in cash conversion that, if unchecked, could further limit the company's flexibility to pursue aggressive R&D in a sector where infrastructure readiness—specifically regarding GPU-backed compute capacity—is now the primary determinant of long-term success. The market remains focused on whether the upcoming quarters can finally bridge the gap between heavy AI investment and bottom-line expansion.