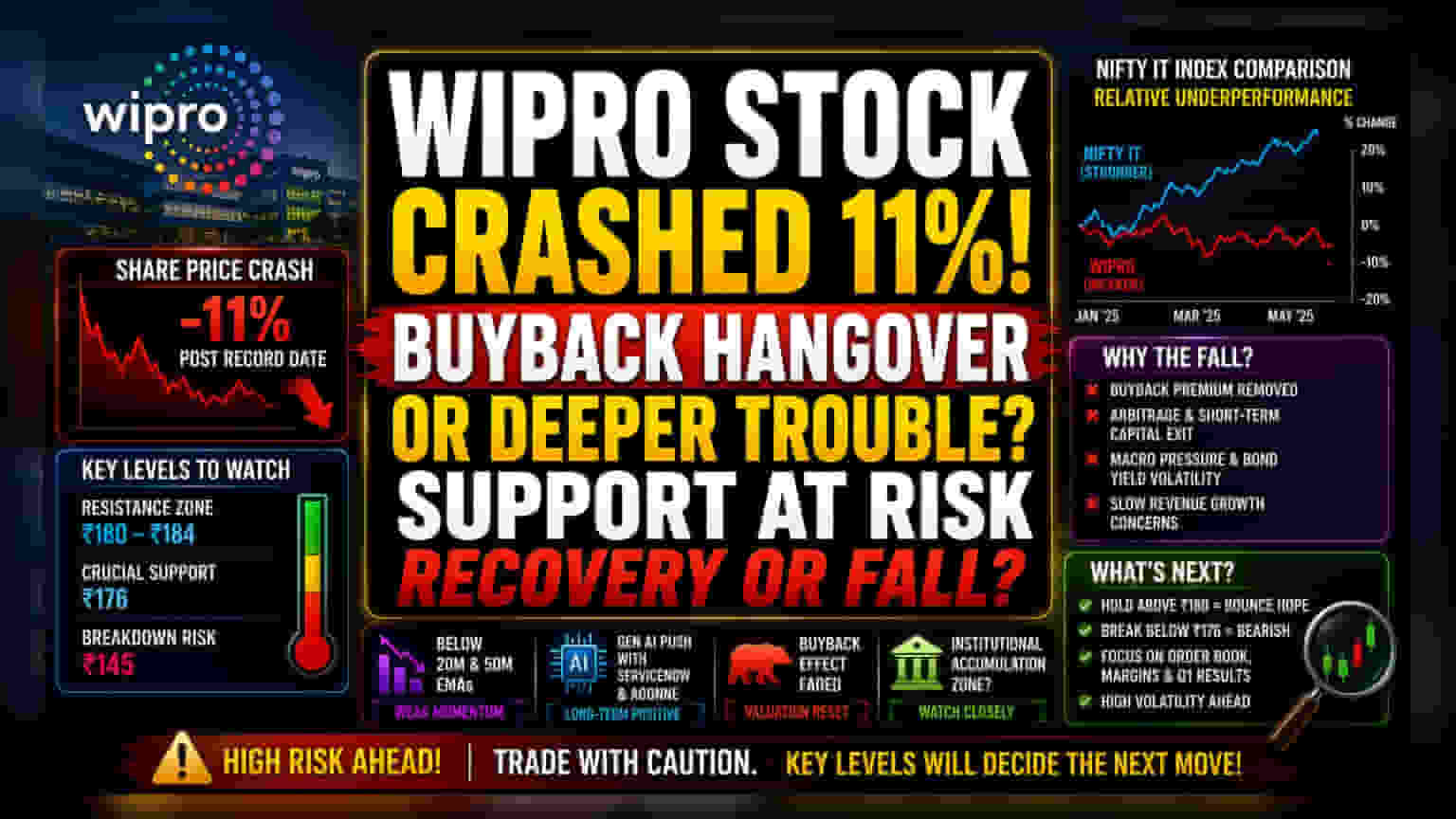

The Mechanical Correction

The recent 11% retracement in Wipro shares represents a common market phenomenon where the removal of corporate action premiums triggers an immediate liquidation of arbitrage-focused capital. With the June 5 record date now passed, the stock has transitioned from its elevated pre-buyback valuation into a period of aggressive price discovery. This sharp volatility is less a commentary on immediate operational performance and more an indication of the speed at which institutional portfolios adjust for the absence of further buyback-driven support.

The Valuation Floor and Sector Benchmarking

Investors are currently monitoring the Rs 180 to Rs 184 range, a zone that has historically served as a magnet for institutional accumulation. While Wipro’s recent expansion into generative AI through its partnership with ServiceNow and the integration of Aggne Global provide long-term narratives, the stock’s current price action is heavily dictated by the broader Nifty IT index. Unlike peers in the large-cap space that have shown greater resilience to bond yield volatility, Wipro remains tethered to a weaker momentum profile, evidenced by its persistent trading below both 20-month and 50-month exponential moving averages. The lack of relative strength against the wider tech benchmark suggests that external macro variables, particularly interest rate expectations, are currently neutralizing company-specific growth drivers.

The Forensic Bear Case

The prevailing optimism regarding a support-led recovery overlooks the structural vulnerabilities inherent in the current setup. If the Rs 176 support level fails to hold, technical indicators suggest a rapid deterioration of market structure, potentially exposing the stock to a test of the Rs 145 psychological floor. Furthermore, the reliance on buybacks to prop up equity value often masks underlying stagnation in organic revenue growth. While management emphasizes transformation efforts, the company continues to navigate a demanding environment where client discretionary spending remains guarded. Investors should be wary of the risk that this correction is not merely a post-buyback dip but a repricing of the stock’s inability to outpace its peers in high-margin segments.

Future Trajectory

Looking ahead, market consensus remains divided between those viewing the current valuation as a reduced-risk entry point and those anticipating further downside due to sluggish momentum. The immediate focus for traders will be the weekly closing price, as a sustained breach of the Rs 180 mark would likely invalidate the current recovery thesis. Institutional sentiment will likely remain cautious until Wipro demonstrates a sustained uptick in order book conversion and a stabilization of operating margins in the upcoming quarterly disclosures.