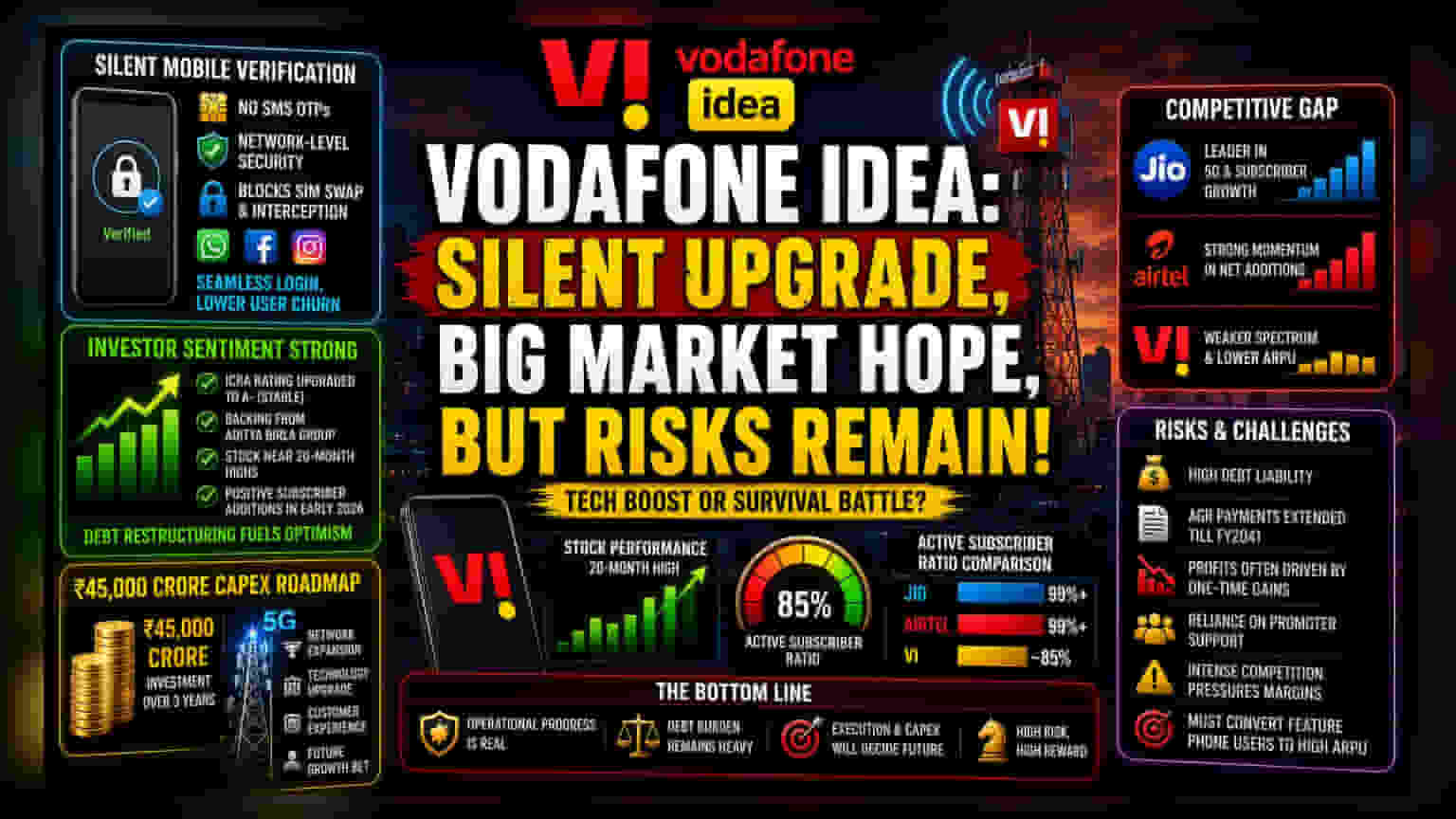

The Shift to Silent Authentication

Vodafone Idea’s implementation of silent mobile verification (SMV) represents a move to modernize its digital infrastructure by replacing traditional SMS-based one-time passwords (OTPs) with seamless network-level authentication. By validating user identity directly against network records, the platform seeks to eliminate the inherent vulnerabilities of SMS, such as SIM swapping and interception, which have become significant points of failure for Indian consumers. This integration with WhatsApp, Facebook, and Instagram is designed to lower user churn during registration and login processes by removing the friction of manual credential entry.

Market Sentiment vs. Operational Reality

The initiative arrives as Vodafone Idea attempts to capitalize on a period of renewed investor interest. Following recent credit rating upgrades—including a shift by ICRA to A- with a stable outlook—and continued backing from the Aditya Birla Group, the stock has recently seen significant price appreciation, trading near 20-month highs. Investors appear to be pricing in the company’s recent debt-to-equity restructuring and the potential for a stabilizing subscriber base, which saw positive monthly additions in early 2026 for the first time in years. However, the market’s enthusiasm remains tethered to long-term survival metrics, contrasting sharply with the company’s need to fund a massive ₹45,000 crore capital expenditure roadmap over the next three years.

The Competitive Gap

Despite the technological upgrade, Vodafone Idea remains disadvantaged compared to industry leaders Reliance Jio and Bharti Airtel. While this partnership improves the user experience, the competitive divide in spectrum holdings and average revenue per user (ARPU) persists. Rivals like Airtel and Jio continue to dominate both 5G penetration and wireless subscriber growth, with Airtel recently demonstrating stronger momentum in net additions. Vodafone Idea’s active subscriber ratio, which hovers around 85%, continues to lag behind the 99%+ efficiency seen at its larger peers, underscoring the gap between headline subscriber counts and actual revenue-generating users.

Risk Factors and Structural Weakness

Investors must distinguish between operational updates and the company's underlying debt challenges. While government relief measures and adjusted gross revenue (AGR) rescheduling have extended the company’s repayment runway to fiscal year 2041, the firm still manages a substantial liability burden. Past quarterly results often reveal that headline profits are heavily skewed by exceptional one-time gains rather than core operational profitability. Any reliance on consistent capital infusion from promoters to meet debt obligations creates a fragile recovery path. Future success depends entirely on whether the company can execute its capex plan to stem subscriber churn and successfully elevate its feature-phone users to high-ARPU smartphone segments before the competitive intensity of the telecom sector further erodes its margins.