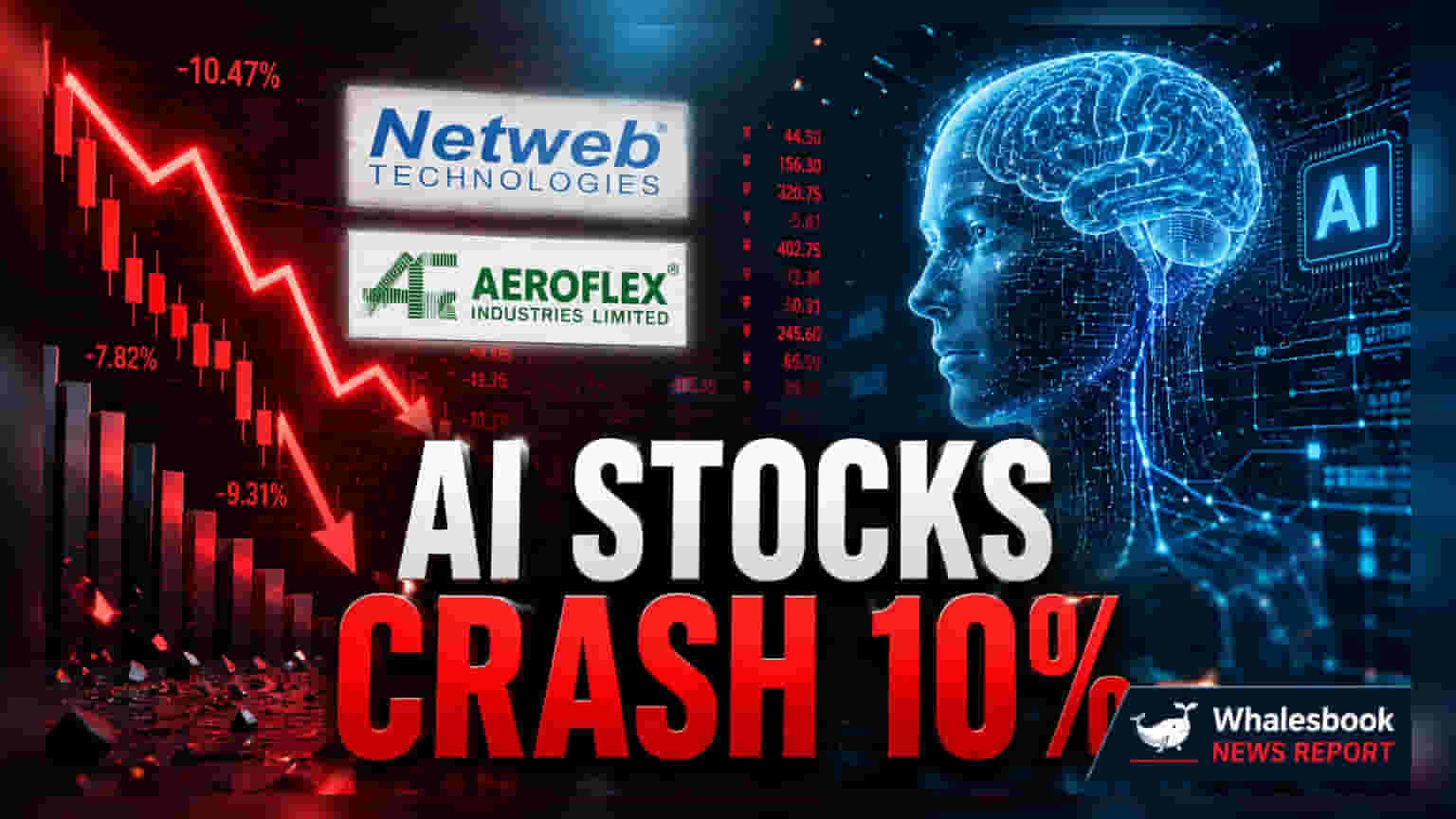

Shares of Indian AI-linked companies like Netweb Technologies and E2E Networks fell by up to 10% on July 7, 2026. This decline followed a global downturn in technology stocks as investors questioned if the rapid AI rally could justify current high valuations. The sell-off impacted major chipmakers worldwide, shifting investor focus from AI enthusiasm to potential risks like overcapacity and cyclical demand patterns.

Indian technology stocks with exposure to artificial intelligence faced intense selling pressure on July 7, 2026. Companies such as Netweb Technologies, Aeroflex Industries, E2E Networks, and Black Box saw their share prices drop by as much as 10% during the trading session. This sharp decline mirrored a broader global correction in technology stocks as markets across Asia and Europe reacted to concerns that the recent surge in AI-related valuations may have moved ahead of company fundamentals.

Global Tech and Chip Sector Correction

The market mood turned cautious after the MSCI Asia Pacific Index experienced a notable decline of 1.5%. The pressure was particularly visible in the semiconductor sector, a critical component of the AI supply chain. In Europe, the STOXX Europe 600 Technology index fell by nearly 2%. Major global semiconductor equipment manufacturers, including ASML Holding, Infineon Technologies, and STMicroelectronics, saw their shares slide by approximately 5% each. South Korea’s tech market was hit especially hard, with Samsung Electronics shares dropping 10% and SK Hynix sliding 6%, despite recent reports of strong profit growth at Samsung.

Concerns Over Expansion and Overcapacity

Investors are now weighing the impact of massive spending on new manufacturing facilities by major global chip players. While the demand for AI data centers remains high, some market analysts are raising questions about the future of this growth. Specifically, there is a debate over whether the current, rapid pace of expansion in chipmaking capacity will lead to a supply glut. If supply grows faster than actual demand, it could cause the current shortage of DRAM memory chips to disappear quickly, potentially hurting the profit margins of these companies.

This sentiment has been influenced by cautionary views on the cyclical nature of the memory chip industry. Even when demand for technology hardware is strong, the industry remains prone to cycles where high investment in new plants can eventually lead to overcapacity and price drops for products. For investors, this shift highlights the risk that companies spending heavily on expansion may face significant challenges if demand does not keep pace with new production capacity.

The key monitorable for shareholders in this sector will be management commentary on order execution, actual capacity utilization rates, and the sustainability of profit margins in coming quarters. Investors may watch how these domestic technology companies navigate the potential for slowing global demand and whether their specific niche in the AI value chain provides enough protection against the broader cyclical downturn affecting global semiconductor manufacturers.