CE Info Systems, the parent company of MapmyIndia, has reported a record order book of Rs 1,754 crore, marking a 17% growth compared to the previous year. While the company deals with the challenge of converting these orders into revenue following past execution delays, its debt-free status and improving margins in the IoT segment provide a significant point of interest for investors. The key focus remains on how quickly the company can turn these existing contracts into actual financial results.

What Happened

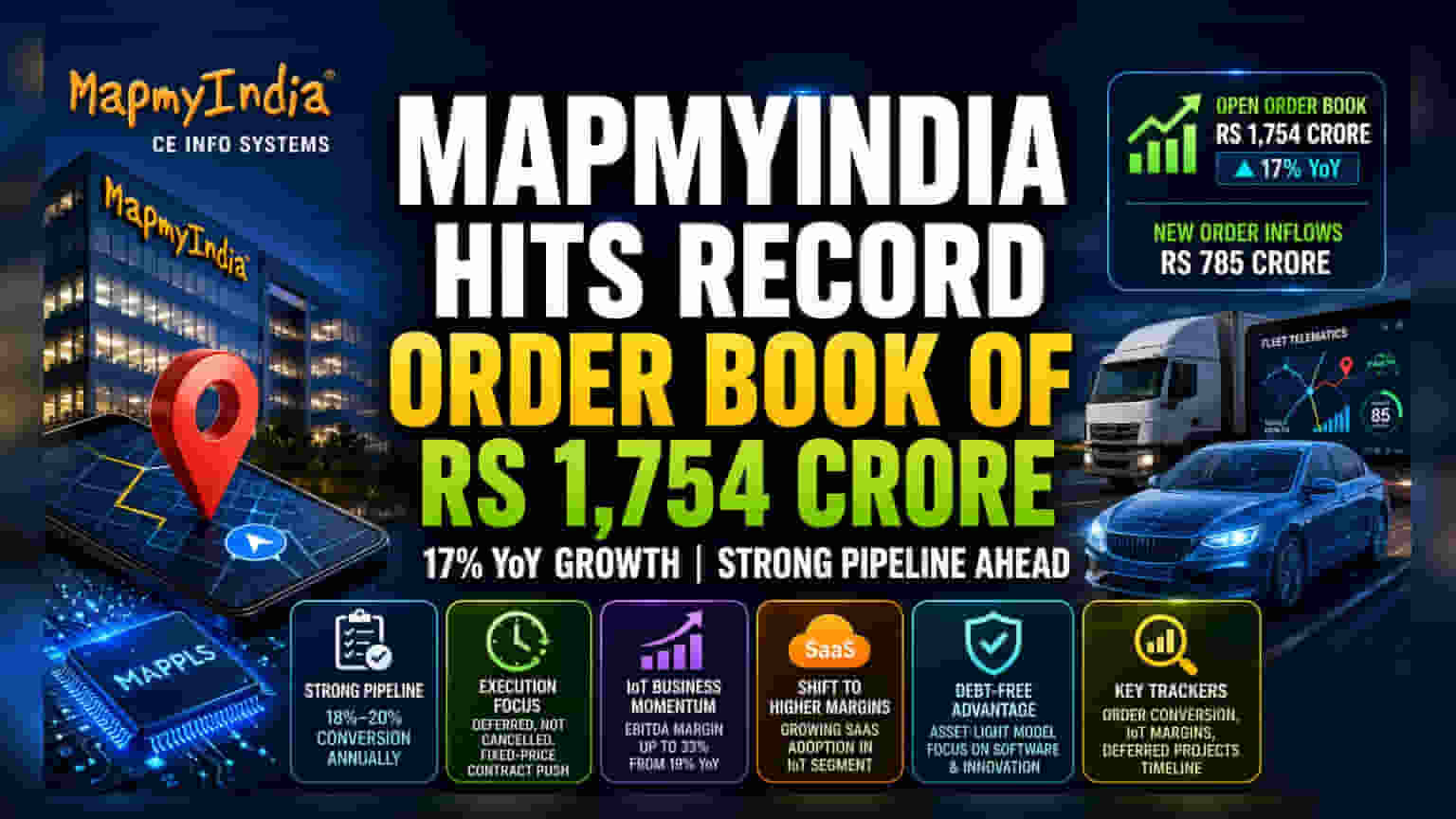

CE Info Systems, popularly known as MapmyIndia, has reported a significant development regarding its business pipeline. The company closed the 2026 financial year with a record open order book of Rs 1,754 crore. This represents a 17% increase year-on-year. During the year, the company secured new order inflows totaling Rs 785 crore. This large backlog is a crucial indicator for investors, as it represents the future work that the company has committed to deliver and bill for in the coming quarters.

Why The Order Book Matters

For investors, a large order book is typically a sign of strong demand. However, the true value of an order book lies in its conversion—that is, how much of that work actually gets finished and converted into revenue. Historically, MapmyIndia sees roughly 18% to 20% of its opening order book turn into revenue within a single year. Therefore, this Rs 1,754 crore figure provides a clearer picture of potential revenue in the near future, provided the company can execute the projects on time.

The Challenge of Execution

Over the past year, MapmyIndia faced some hurdles with project execution, particularly in the government and automotive sectors. These delays caused the company's stock performance to lag despite the underlying demand for its mapping and technology services. However, it is important for investors to note that management has clarified these projects were deferred rather than cancelled. This means the revenue opportunity remains, just delayed. To improve predictability, the company has increasingly shifted toward fixed-price contracts, which can help in managing revenue expectations more accurately.

The Shift Toward Higher Margins

One of the most notable trends in the company's performance is the improvement in its IoT (Internet of Things) business. In the final quarter of FY26, the EBITDA margin for the IoT segment expanded to 33%, up from 19% in the same period last year. This jump in profitability is primarily driven by the company’s push toward SaaS (Software as a Service) models, which generally carry higher profit margins compared to traditional project-based work. The company is seeing strong adoption of its technology in areas like fleet telematics, logistics, and enterprise applications.

The Business Structure Advantage

MapmyIndia benefits from being a debt-free and asset-light company. This means it does not carry the burden of heavy interest payments or the need for massive capital spending on physical machinery, which often pressures the balance sheet of manufacturing or infrastructure firms. This structure allows the company to focus its resources on software development and scaling its Mappls ecosystem, which includes navigation, connected vehicle tech, and ADAS (Advanced Driver Assistance Systems) programs.

Risks and Concerns

While the order book is promising, the primary risk for investors remains execution. If the company continues to face delays in project rollouts—whether due to customer-side issues, testing requirements, or government approvals—the revenue growth could remain uneven. Additionally, the company operates in a competitive technology space where it must consistently prove the value of its proprietary mapping data and software against global giants and emerging local players. Investors should be aware that until the company consistently converts its order book into actual revenue at a steady pace, execution risk will remain a central theme.

What Investors Should Track

Moving forward, the key monitorable is the speed and consistency of project conversion. Investors will be looking for signs that the backlog is turning into cash flow efficiently. Additionally, it will be important to watch the maintenance of margins in the IoT segment; sustained high profitability in this area would suggest that the software-focused business model is scaling effectively. Finally, management updates regarding the timeline for the deferred projects in the government and defense sectors will provide clarity on whether the previous execution hurdles are truly behind the company.