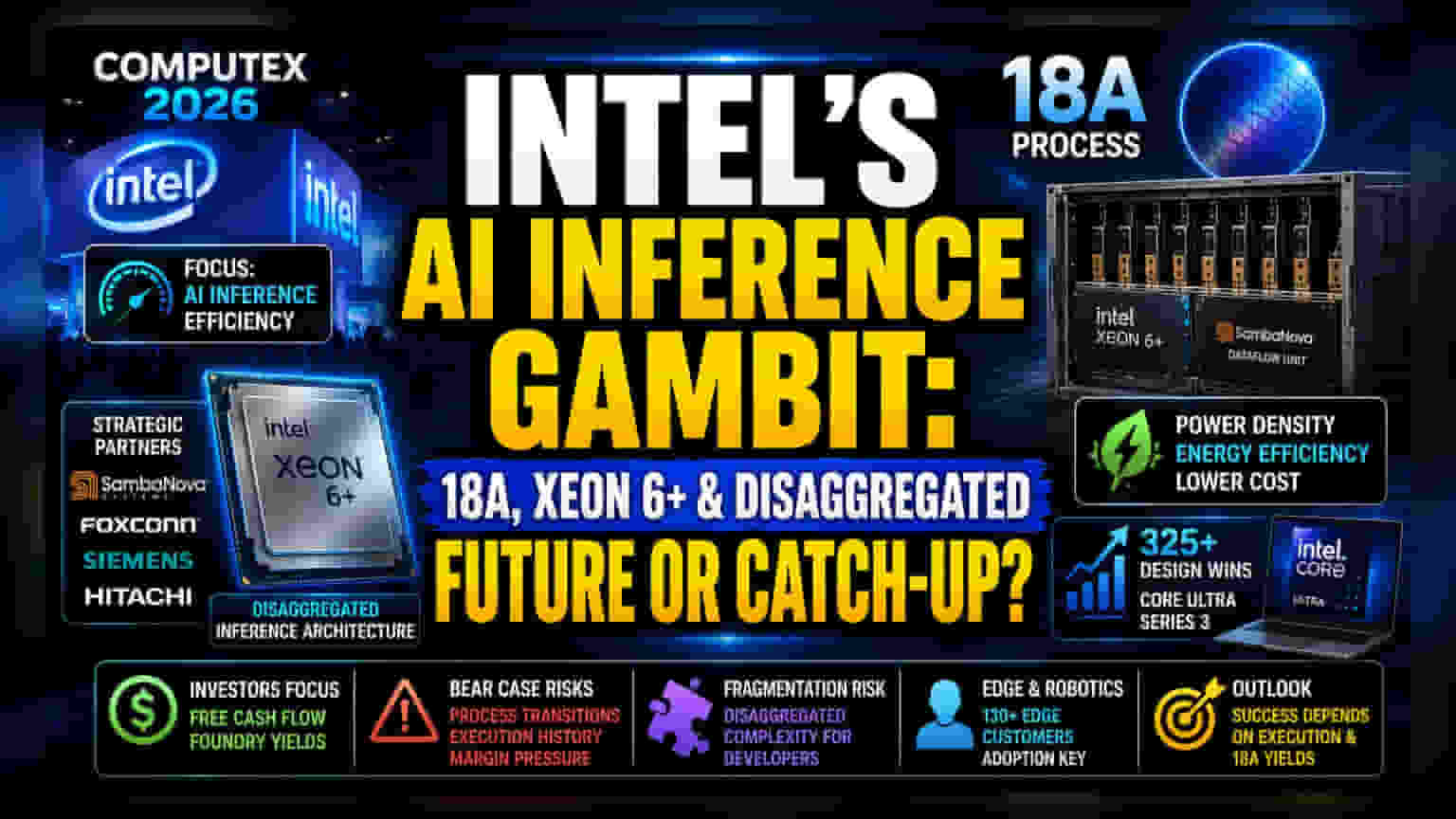

The Shift Toward Inference Efficiency

The narrative emerging from Computex 2026 centers on Intel’s tactical retreat from trying to out-scale competitors in raw training power, opting instead to dominate the high-growth niche of AI inference. By integrating Xeon 6+ processors with SambaNova’s dataflow units, the firm is attempting to commoditize infrastructure costs. The real value proposition here lies in power density and energy efficiency—metrics that have become the primary battleground for enterprise data centers facing massive electricity constraints. While the partnership with Foxconn for manufacturing is designed to lower hardware barriers, the market remains fixated on whether these disaggregated inference systems can erode the software-defined moat currently enjoyed by rivals.

Valuation and Competitive Context

Intel’s transition to the 18A process node arrives at a time when capital expenditure in the semiconductor space is facing extreme scrutiny. Unlike previous cycles where pure hardware performance drove stock valuation, current investors are prioritizing Free Cash Flow and foundry yields. Compared to foundry peers like TSMC, which maintains a dominant share of advanced-node manufacturing, Intel’s reliance on 18A success is high-stakes. While 325 design wins for Core Ultra Series 3 suggest strong consumer-side penetration, the margin profile of these client-side devices typically pales in comparison to the high-margin enterprise accelerator segment that Nvidia continues to command.

The Forensic Bear Case

The optimism surrounding the 18A rollout must be tempered by Intel’s historical challenges with process node transitions and the recurring pressure of operating margins. While the company touts a vast ecosystem involving Siemens and Hitachi, these ventures are often long-cycle, capital-intensive, and slow to reflect on the balance sheet. Skeptics note that the move toward 'disaggregated inference'—while technically sound—risks fragmentation, potentially complicating the developer experience compared to more unified, monolithic hardware stacks. Furthermore, Intel’s history of executive turnover and delayed product roadmaps keeps the institutional discount high, suggesting that until 18A yields reach parity with leading-edge competitors, the market may continue to view these announcements as 'catch-up' rather than 'innovation-leading.'

Future Outlook

Management continues to prioritize the integration of edge computing and robotics, betting that the next wave of AI will occur outside the cloud. If adoption among the 130-plus edge computing customers translates to enterprise-scale deployment by late 2026, the company could see a stabilization in its data center revenue. However, brokerage sentiment remains mixed, with analysts largely waiting for verifiable evidence of foundry profitability before adjusting current price targets. The success of this strategy rests entirely on the execution of the Xeon 6+ roadmap and the ability to maintain manufacturing volume without further capital dilution.