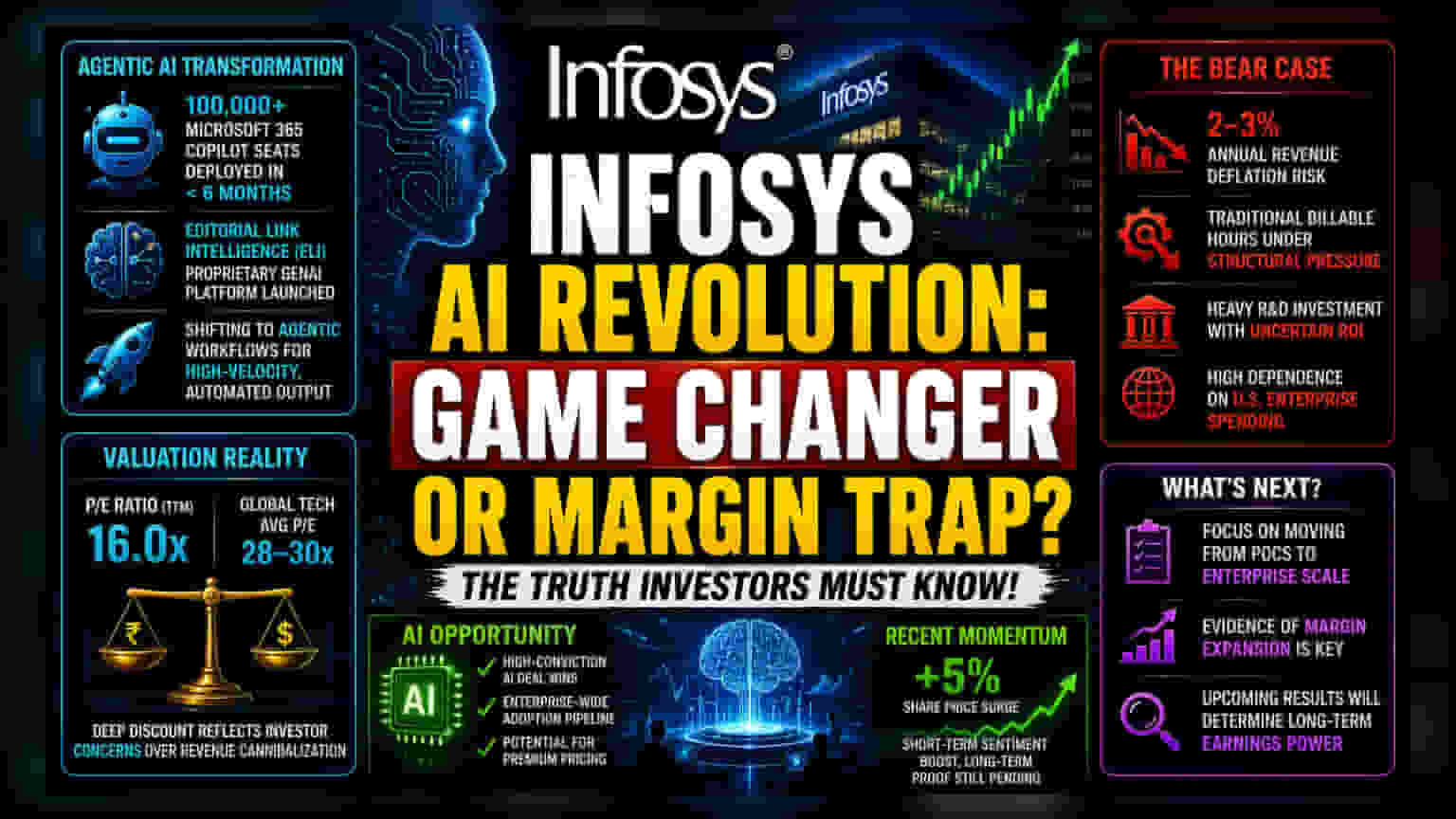

The Shift to Agentic Workflows

Infosys is rapidly transitioning its service delivery model toward agentic AI, underscored by the deployment of over 100,000 Microsoft 365 Copilot seats. This move, executed in under six months, signals an attempt to shift from manual coding to automated, high-velocity output. The launch of proprietary tools like the Editorial Link Intelligence (ELI) further demonstrates an intent to monetize GenAI offerings directly, rather than relying solely on third-party service integration. Despite these technological strides, the core challenge remains the monetization of these efficiencies in a sector historically tethered to billable hours.

The Efficiency Paradox and Valuation

While Morgan Stanley maintains a constructive outlook on the broader Indian IT sector, the valuation gap between global tech leaders and domestic stalwarts persists. Trading at a P/E ratio of approximately 16.0, Infosys sits at a significant discount compared to broader technology benchmarks. This compression reflects deep-seated investor anxiety regarding the cannibalization of traditional revenue streams. As productivity gains translate into faster cycle times, the underlying time-and-material billing models face structural headwinds. Market participants are increasingly monitoring whether Infosys can command premium pricing for AI-driven outcomes or if it will be forced into a race to the bottom on service costs as basic coding becomes a commoditized utility.

The Bear Case: Structural Margin Risk

Beneath the surface of AI optimism lie significant risks that could impede long-term performance. Unlike peers that maintain lower leverage or higher margin visibility, Infosys must navigate the dual pressure of heavy internal R&D investment and potential deflation in traditional service revenues, which some analysts project could see 2-3% annual pressure over the coming years. Furthermore, the reliance on US enterprise spending makes the company highly vulnerable to shifting macroeconomic conditions. Should the anticipated demand for high-end AI transformation fail to materialize as a replacement for traditional contract losses, the current rally may prove to be a short-term reaction to sentiment rather than a fundamental shift in earnings power.

Future Outlook

Brokerage sentiment remains selective, focusing on firms capable of handling the transition from 'proof-of-concept' pilots to enterprise-wide adoption. While the recent 5% surge in share price highlights short-term momentum, the long-term viability of this AI-centric strategy hinges on Infosys’s ability to move beyond service-based billing. Analysts are now looking toward upcoming quarterly results for concrete evidence of margin expansion resulting from these AI deployments, as the initial excitement of high-conviction deal announcements begins to give way to rigorous scrutiny of bottom-line impact.