Indian IT stocks are undergoing a major valuation reset, with the Nifty IT index now trading around 18 times trailing earnings. As large players like TCS and Infosys see significant multiple contraction, investors are questioning if current valuations are justified compared to global peers like Accenture. The central focus is whether future growth can support these valuations amid uncertainty from AI disruption.

What Happened

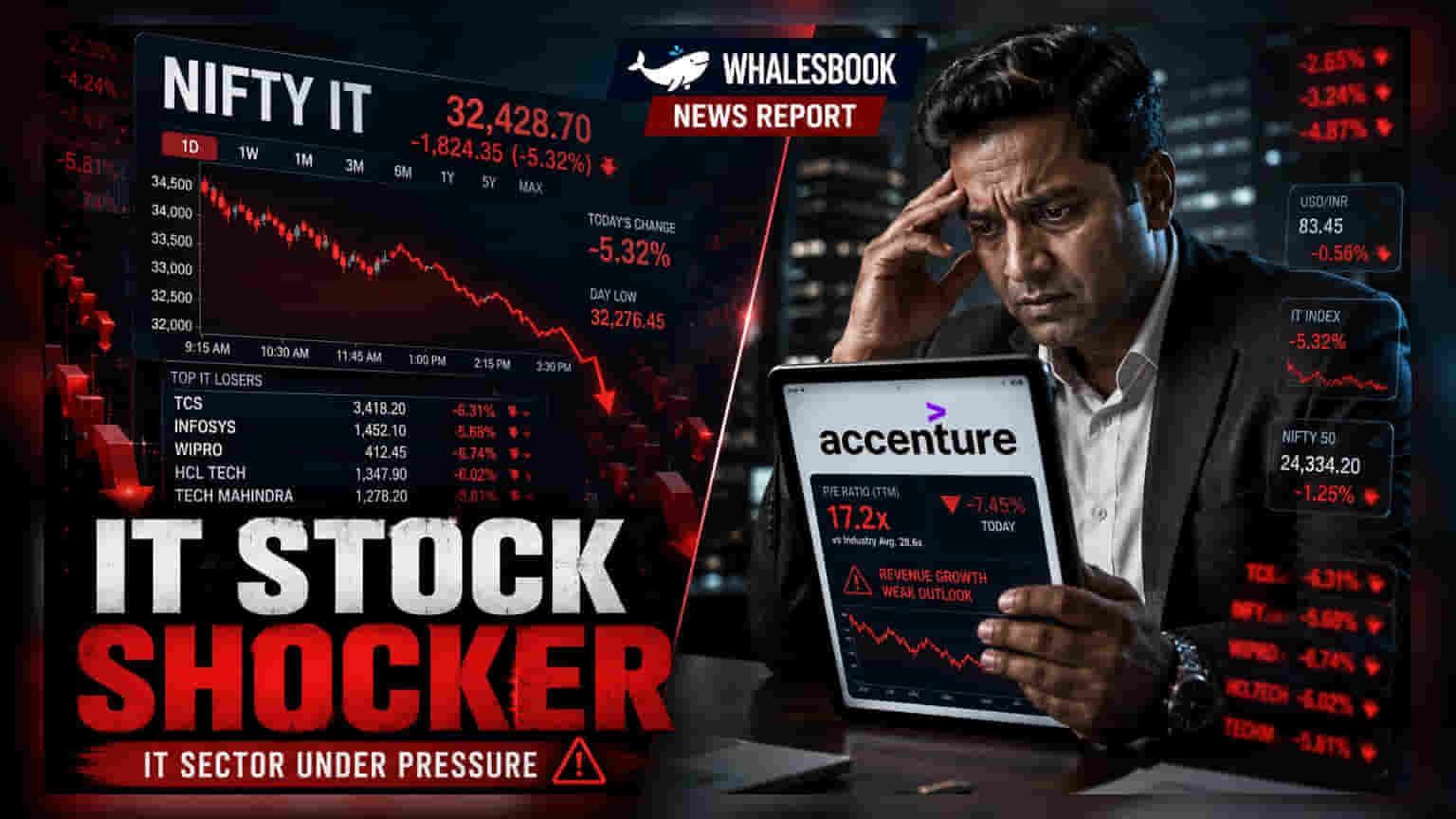

Major Indian information technology (IT) companies are currently experiencing a significant period of valuation adjustment. Over the past year, the Nifty IT index has corrected by approximately 30%, leading to a compression of price-to-earnings (P/E) multiples. The index is now trading at roughly 18 times its trailing earnings. This shift reflects a broader market re-evaluation of the sector, which has moved away from the high-multiple era experienced during the post-COVID period.

Valuation Contraction in Large-Cap IT

The market landscape for India's largest IT firms—TCS, Infosys, and Wipro—has changed considerably. These companies, which previously traded at P/E multiples ranging from 30x to 40x, are now trading at approximately 14 to 15 times trailing earnings. HCL Technologies is currently trading at a slightly higher multiple of around 18 times. This correction is particularly notable for TCS, whose valuation multiple has reduced significantly from its peak levels, highlighting the shift in investor sentiment regarding the growth prospects of these industry giants.

Global Peers and Performance Gap

Investors are increasingly comparing Indian IT firms with global counterparts such as Accenture. Historically, Accenture often traded at a valuation premium compared to Indian IT majors. However, current data shows a shift, with Accenture trading at roughly 10 times trailing P/E. When looking at long-term performance, Accenture’s projected U.S. dollar earnings per share (EPS) growth rate for the 2016-2026 period is estimated at 10%. In contrast, Indian majors like TCS, Infosys, and HCL Technologies are projected at approximately 6%, with Wipro around 3%. This discrepancy between the valuation multiples and the relative growth performance has prompted a debate about the sustainability of the remaining valuation premiums held by Indian IT stocks.

AI Uncertainty and Growth Prospects

The primary concern for the $250 billion Indian IT sector is the sustainability of future growth in the face of ongoing technological disruption, particularly from artificial intelligence (AI). While dividend yields, such as TCS’s 5.2%, provide some level of support for shareholders, there is ongoing speculation about whether current growth forecasts are realistic. Companies like KPIT Technologies have already faced market pressure following negative outlook announcements, and many mid-cap IT firms continue to trade at elevated multiples of 30x to 40x despite the sector-wide correction.

What Investors Should Track

The key monitorable for investors is whether these companies can demonstrate growth rates that justify their current valuations. Beyond tracking quarterly revenue and profit growth, market participants may watch how firms balance capital allocation between shareholder payouts, like dividends, and necessary investments in AI and new technologies. The market is also evaluating whether the current valuation levels have fully priced in potential headwinds or if further adjustments are necessary based on the sector’s ability to navigate changing global demand.