India’s smartphone market faces a structural slowdown as consumers extend device replacement cycles to 36 months. Rising component costs, driven by a global memory shortage, are pushing up prices and cooling demand. Investors should watch how major brands adapt their product strategies as volume-led growth shifts toward a value-driven model.

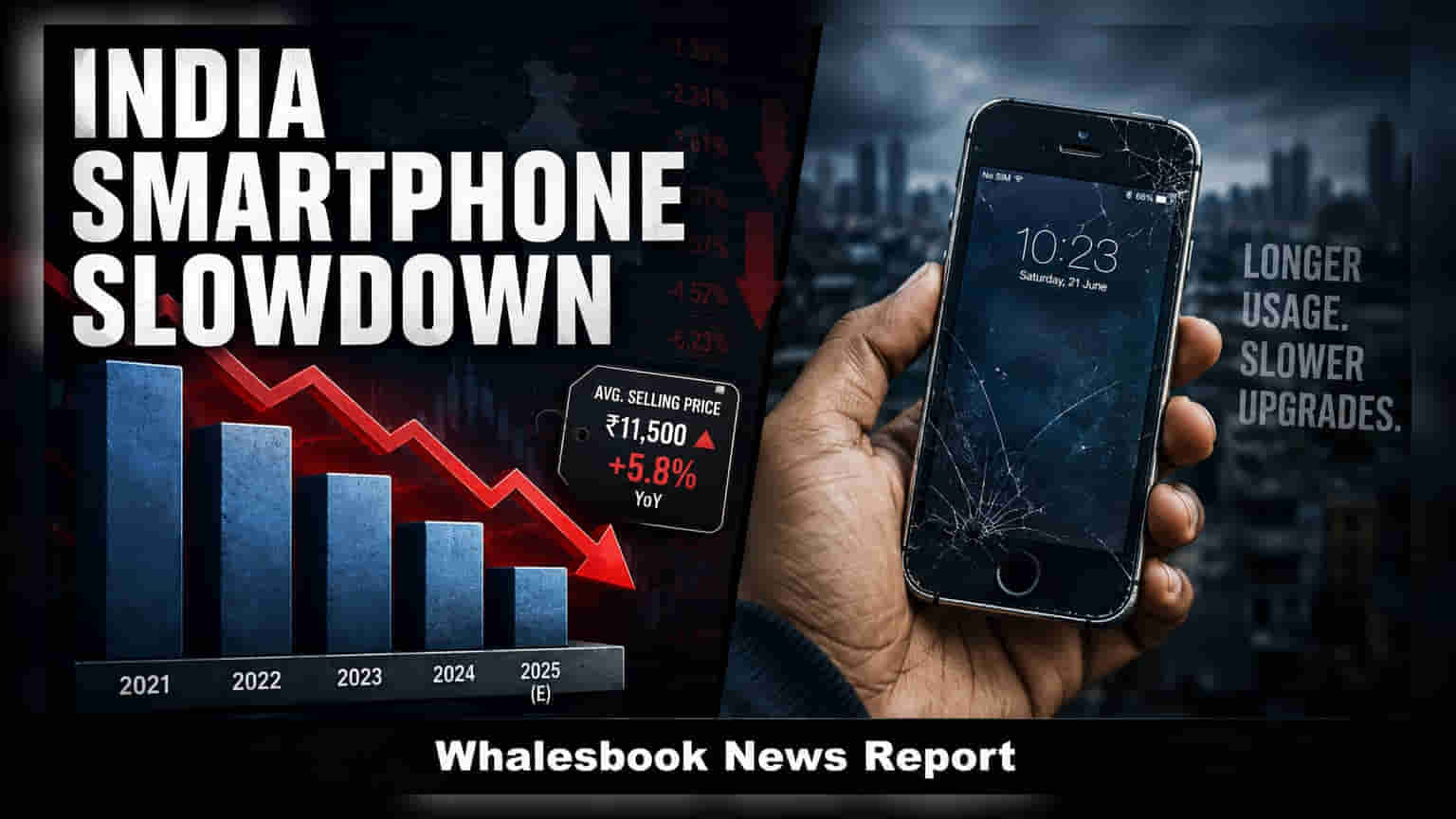

India’s smartphone sector is entering a period of significant change as the fast-paced upgrade cycles that defined the industry for years begin to slow down. Data from IDC indicates that smartphone shipment volumes are expected to decline by nearly 10% in the first half of 2026, with total shipments projected to hit between 63 million and 65 million units. This shift marks a departure from historical trends where consumers typically replaced their devices every 18 to 24 months.

Impact of Rising Costs on Device Pricing

The current market slowdown is largely driven by cost pressures rather than a simple lack of consumer interest. A global shortage in memory components, often referred to as 'memflation,' has pushed up the bill of materials for manufacturers. While brands previously absorbed many of these cost increases to maintain sales volume, the scale of current shortages has made this strategy difficult to sustain. As a result, average selling prices are projected to rise significantly, moving from $275 in the first half of 2025 to over $320 in the first half of 2026. For the Indian consumer, this translates into potential price hikes of ₹3,000 to ₹5,000 for mid-range handsets, while entry-level devices may see price points climbing toward the ₹12,000 to ₹14,000 range.

Changing Consumer Behavior and Market Maturity

Beyond cost concerns, the smartphone itself has reached a level of maturity that naturally discourages frequent upgrades. Newer models now feature durable hardware and extended software support, making the previous trend of rapid model turnover less attractive. As incremental improvements in cameras and processors become the norm, consumers are increasingly choosing to hold onto their existing phones for 36 months or longer. This behavioral change is particularly visible in the entry-to-mid price segments, where price sensitivity is highest. Many users are now turning to the refurbished or second-hand market, which offers a cost-effective alternative to purchasing new devices.

Strategic Shifts for Brands

The market’s transition from a volume-led upgrade cycle to a value-driven one is forcing brands to rethink their business models. Instead of relying on rapid product launches to drive revenue, companies are focusing on higher-value premium segments to protect their profit margins. IDC anticipates that the second half of 2026 may see an even sharper decline in shipments, potentially dropping by over 15% compared to the same period in 2025. Investors should monitor whether these companies can successfully transition their focus toward premium products and how effectively they manage their inventory levels in a market where demand is increasingly tied to actual necessity rather than frequent replacement.