V Vaidyanathan, MD & CEO of IDFC First Bank, states that Artificial Intelligence is essential for MSMEs to scale nationally and globally. He emphasized that digital adoption is a prerequisite for growth and accessing credit. This shift aims to help small businesses bridge the gap between traditional operations and modern, data-driven market demands.

What Happened

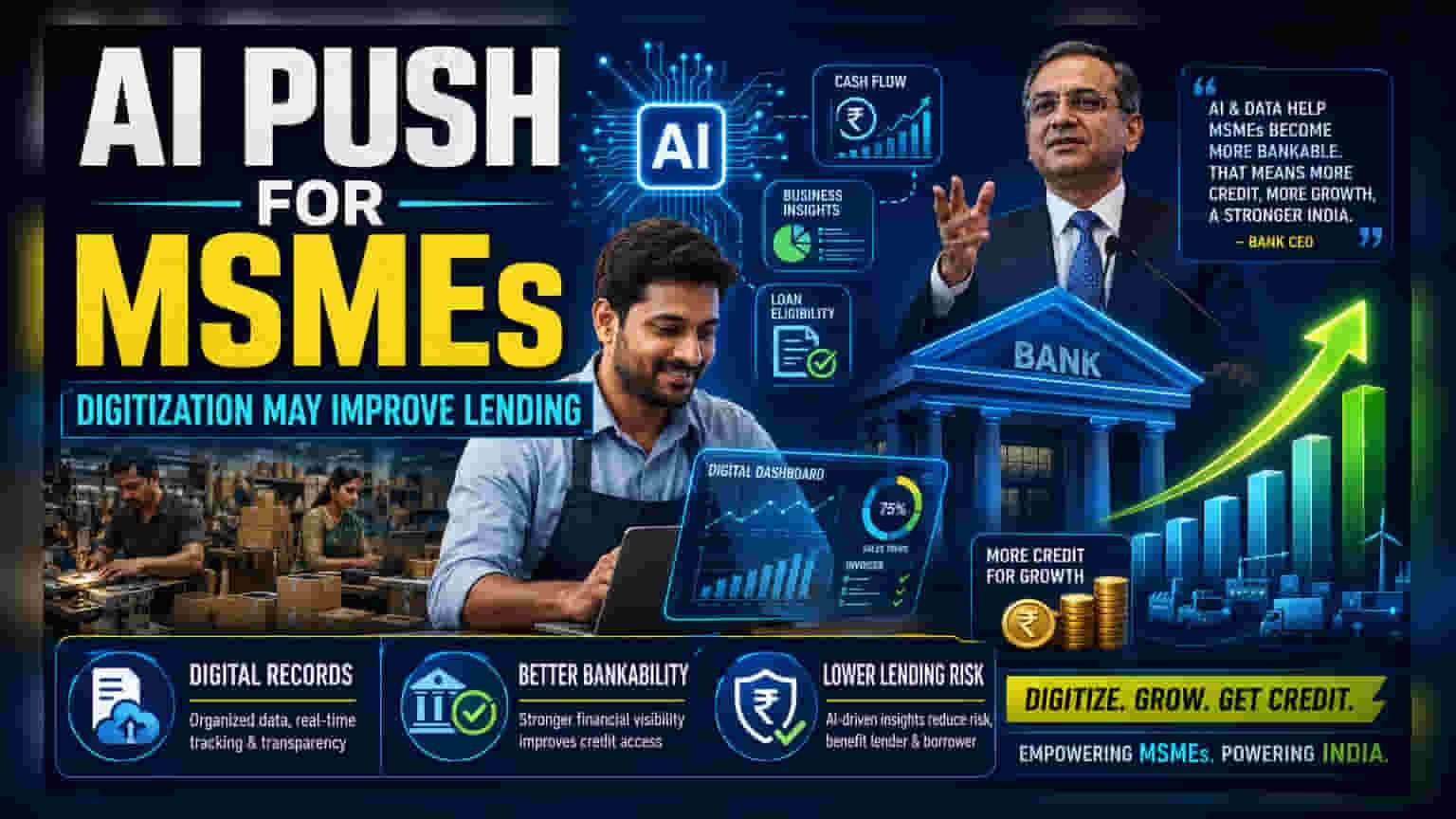

V Vaidyanathan, the Managing Director and CEO of IDFC First Bank, recently highlighted that Artificial Intelligence (AI) and digitization are no longer optional for Indian Micro, Small, and Medium Enterprises (MSMEs). Speaking at a recent industry event, he explained that AI serves as a powerful equalizer, allowing smaller firms to run marketing campaigns and operations with the efficiency of larger corporations. He urged business owners to move beyond local operations and focus on scaling at a national or global level, warning that avoiding digital tools could lead to missing significant growth opportunities.

The Link Between Tech And Lending

For investors, this focus from a bank CEO has a specific business implication. Banks are generally more comfortable lending to businesses that have clear, digital, and verifiable records of revenue and cash flow. When an MSME moves its business online, it creates data that helps banks understand its actual financial health.

This makes the business "bankable." If small firms adopt digital tools, they effectively reduce the information gap that often prevents banks from lending to them. Since IDFC First Bank has a significant focus on retail and MSME lending, their strategy is naturally aligned with getting their target borrowers to become more digitally efficient and, consequently, lower-risk clients.

The Funding Gap Reality

Vaidyanathan also addressed a structural challenge in the Indian business ecosystem. He noted that while digital-first businesses are growing, a vast majority of entrepreneurs still lack access to venture capital (VC). He pointed out that VCs typically invest in only a tiny fraction of businesses.

This creates a difficult cycle for the "remaining 95%" of entrepreneurs. Without equity capital, it becomes harder for these businesses to secure the debt financing they need to expand. This comment highlights the ongoing difficulty that many smaller, non-tech-native firms face when trying to raise capital in a market that is increasingly focused on high-growth, digital-first models.

Why MSME Digitization Matters

The transition from traditional offline models to digital systems changes how banks measure risk. If a business digitizes its accounting, sales, and supply chain, the data provides banks with a clearer view of the business's stability. For investors, the health of the MSME loan portfolio at banks is closely tied to how well these businesses manage their transition to digital platforms. If digitization leads to better cash flow management and more transparent operations, the risk profile of these loans improves, which benefits the lender.

What To Watch Next

The key monitorable for investors is not just the buzz around AI, but the tangible impact of digital adoption on loan performance. Investors may track future management commentary from banks on how tech-led underwriting is performing within their MSME portfolios. Additionally, watching the growth rate of MSME loan books versus the default rates in those segments will help gauge whether this strategy of encouraging business digitization is successfully reducing risk for the lenders.