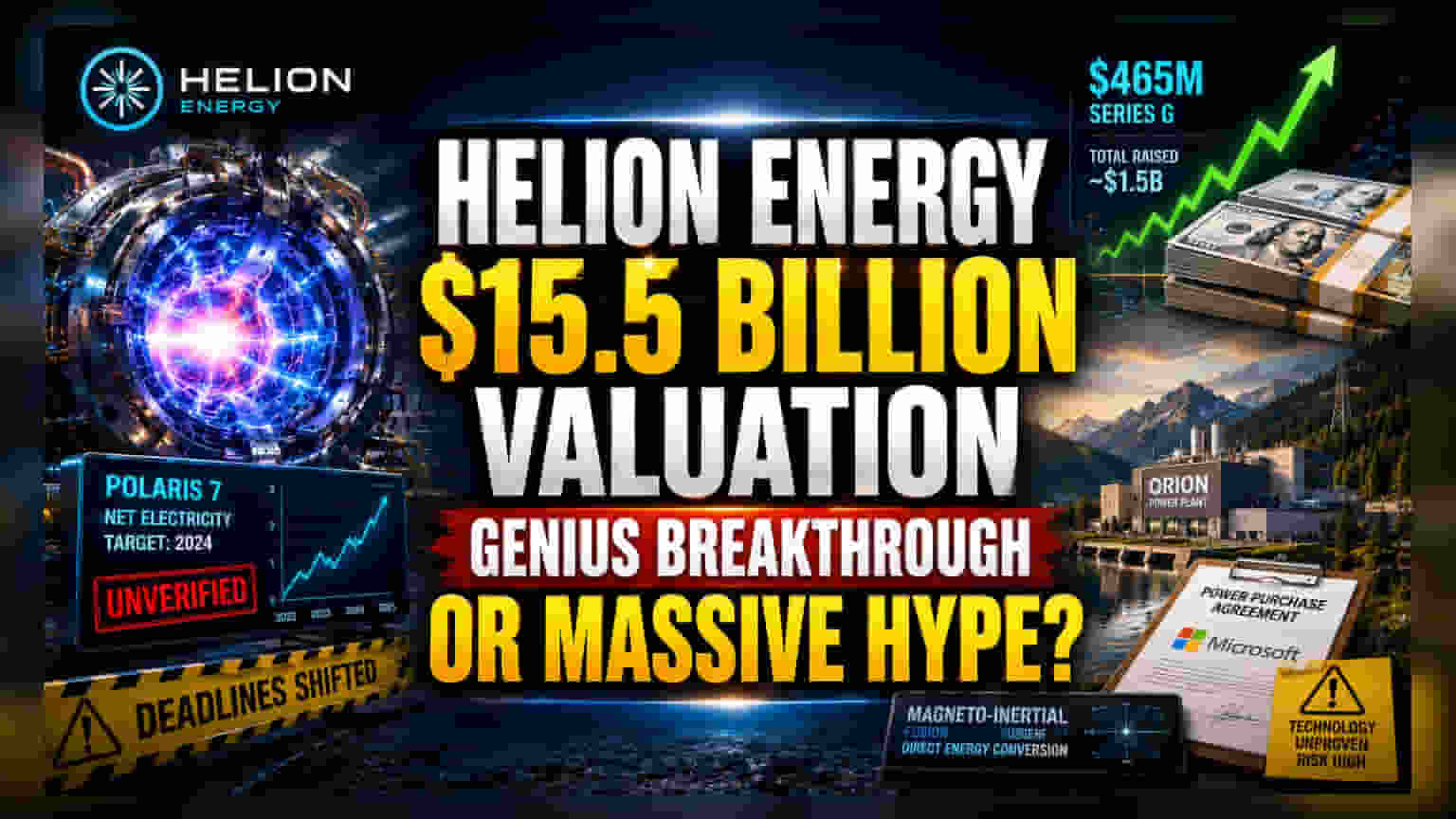

The Valuation Disconnect

Helion Energy has finalized a $465 million Series G funding round, pushing its post-money valuation to an eye-watering $15.5 billion. Led by Thrive Capital, the raise brings the Everett-based company’s total capital intake to approximately $1.5 billion. This surge in valuation—nearly tripling the firm’s previous standing from early 2025—occurs even as the startup faces intensifying pressure to substantiate its technological claims. The capital is earmarked to scale manufacturing and accelerate the construction of the Orion power plant in Chelan County, Washington, a project that serves as the centerpiece of a high-stakes power purchase agreement with Microsoft.

The Direct Capture Gamble

While the broader fusion sector converges on various iterations of tokamak and inertial confinement designs, Helion continues to pursue a high-risk, high-reward divergence: magneto-inertial fusion. The core of their strategy is a direct energy conversion system intended to harvest electricity from plasma expansion against magnetic fields, theoretically bypassing the traditional steam cycle used in conventional power plants. Proponents argue this could lead to vastly more efficient, modular systems. However, physicists and industry skeptics warn that this approach remains largely theoretical. Crucially, the company has provided minimal peer-reviewed experimental data to support its progress, leading many in the scientific community to view its 2028 commercial delivery target with significant apprehension.

The Regulatory and Performance Hurdle

Despite the optimism surrounding its 2028 grid injection target, Helion remains dogged by a history of shifted deadlines. The firm’s seventh-generation prototype, Polaris, was initially positioned to demonstrate net electricity generation by 2024, a milestone that remains unverified in the public domain. The lack of transparency has created a credibility gap that distinguishes Helion from other sector participants who frequently publish findings in reputable journals. Furthermore, the company’s internal operations have previously drawn scrutiny following reports of internal personnel conflicts, adding a layer of management-related risk to an already complex engineering mission.

The Bear Case: A Tech Sector Mirage?

From a cynical financial perspective, Helion’s valuation appears decoupled from verifiable engineering breakthroughs. Unlike established nuclear sectors or even maturing renewable technologies, fusion remains a sector defined by persistent delays and capital-intensive experimentation. Competitors and analysts suggest that even if Helion achieves its engineering goals, the economic viability of its proprietary D-He3 fuel cycle and direct capture system may struggle to compete with the rapidly declining costs of solar PV and battery storage. If the company fails to produce a tangible net energy gain in its upcoming tests, the current $15.5 billion valuation could face a severe correction, potentially undermining investor confidence in the entire private fusion ecosystem.