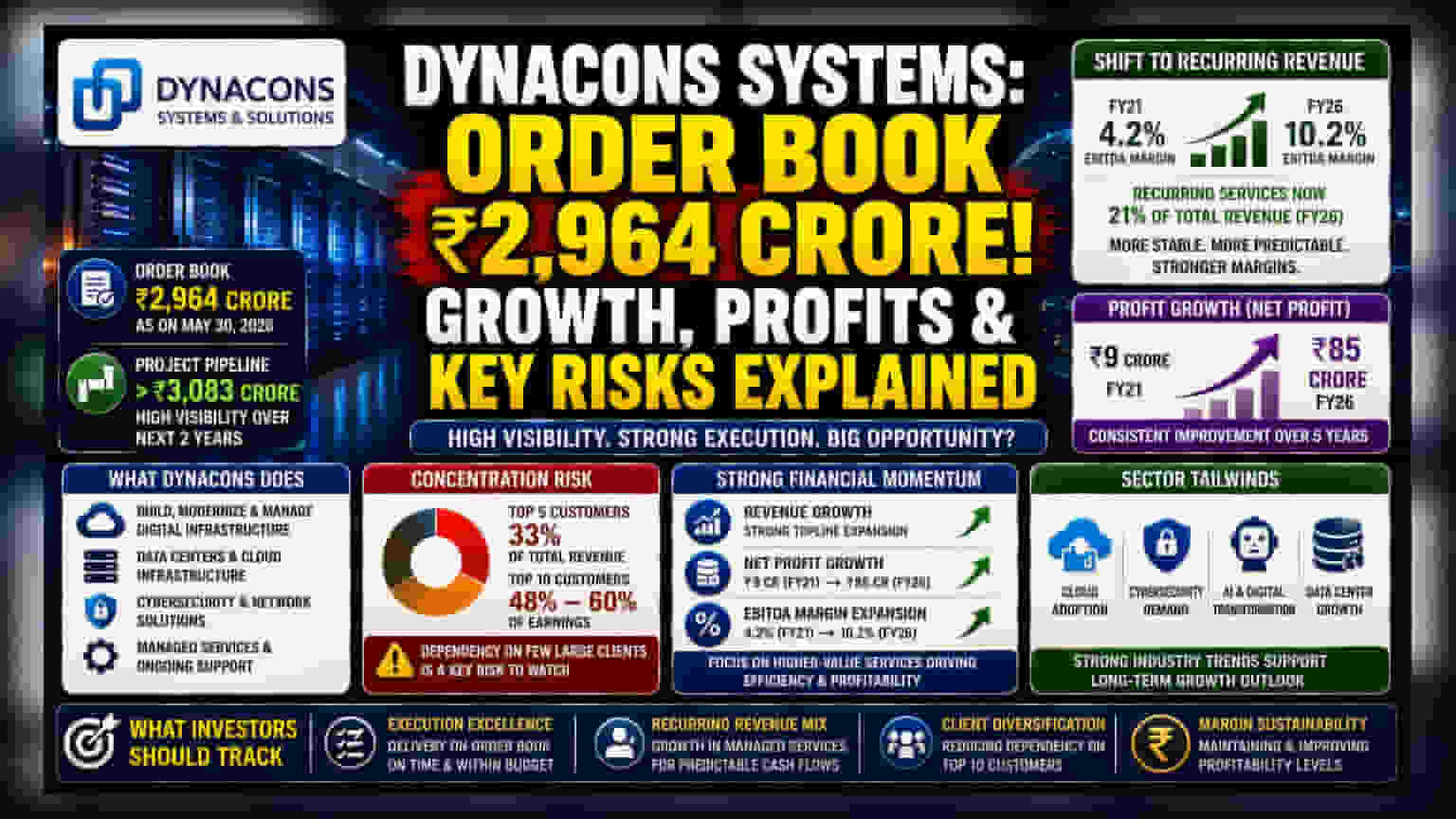

What Happened

Dynacons Systems & Solutions, a small-cap IT infrastructure company, has announced a significant order book of Rs 2,964 crore as of May 30, 2026. This order backlog, combined with a potential project pipeline exceeding Rs 3,083 crore, indicates high visibility for the company’s business over the next two years. Dynacons plays a specialized role in the tech ecosystem, helping organizations build, modernize, and manage digital infrastructure, ranging from data centers to cybersecurity setups.

Why The Shift To Recurring Revenue Matters

Historically, many IT infrastructure providers relied on selling hardware, which is often a one-time, volatile source of revenue. Dynacons has been actively transitioning away from this model. The company is now focusing on "Managed Services," where it earns fees for ongoing support, maintenance, and monitoring. This shift is crucial for investors because service-led revenue tends to be more predictable and steady than product sales.

As of fiscal year 2026, these recurring service contracts represent about 21% of total revenue. This change has had a visible impact on the bottom line. The company reported net profits of Rs 85 crore in FY26, a substantial increase from Rs 9 crore five years ago. Furthermore, EBITDA margins—a measure of operational profitability—have improved to 10.2% in FY26, up from 4.2% in FY21, suggesting that the move toward higher-value services is successfully boosting efficiency.

The Concentration Risk

While the order book and profit growth appear positive, investors should be aware of a specific structural risk: customer concentration. The company relies heavily on a small group of large clients. Its five largest customers account for 33% of its total revenue, and the top 10 clients have historically contributed between 48% and 60% of earnings.

In the small-cap IT space, this type of dependency is a double-edged sword. While it provides strong revenue stability during growth phases, it also means that the loss of a single major contract or a budget cut from a top-tier client could disproportionately affect the company’s financial health. For any investor looking at the long term, monitoring the stability and retention of these key accounts is essential.

Sector Context And Valuation

Dynacons operates in a competitive environment, acting as an intermediary between global tech giants like Cisco, Microsoft, and Dell, and their end-users. The company's focus on high-demand areas like cloud infrastructure, cybersecurity, and AI adoption aligns with broader industry trends where companies are rushing to modernize legacy systems.

Currently, the stock trades at approximately 22 times earnings. This valuation suggests that the market has high expectations for the company's future growth. For investors, the challenge is determining whether this valuation is justified by the company's ability to maintain its margin expansion and successfully execute its order book, or if the current price already reflects much of the anticipated success.

What Investors Should Track Next

Moving forward, the primary monitorable is execution. An order book is only valuable if the company can successfully deliver the projects on time and within budget. Investors may also want to track the mix of recurring revenue; if the share of managed services continues to climb, it could further improve the predictability of cash flow. Additionally, any updates regarding client diversification will be important, as reducing reliance on the top 10 customers would significantly lower the company's risk profile.