Dixon Technologies received a 'buy' rating upgrade from JM Financial, which raised its price target by 27% to Rs 14,200. The optimism centers on the potential of the company's joint venture with Vivo to boost smartphone volumes. However, investors are watching for risks related to margin pressure, execution timelines, and the broader competitive landscape in electronics manufacturing.

What Happened

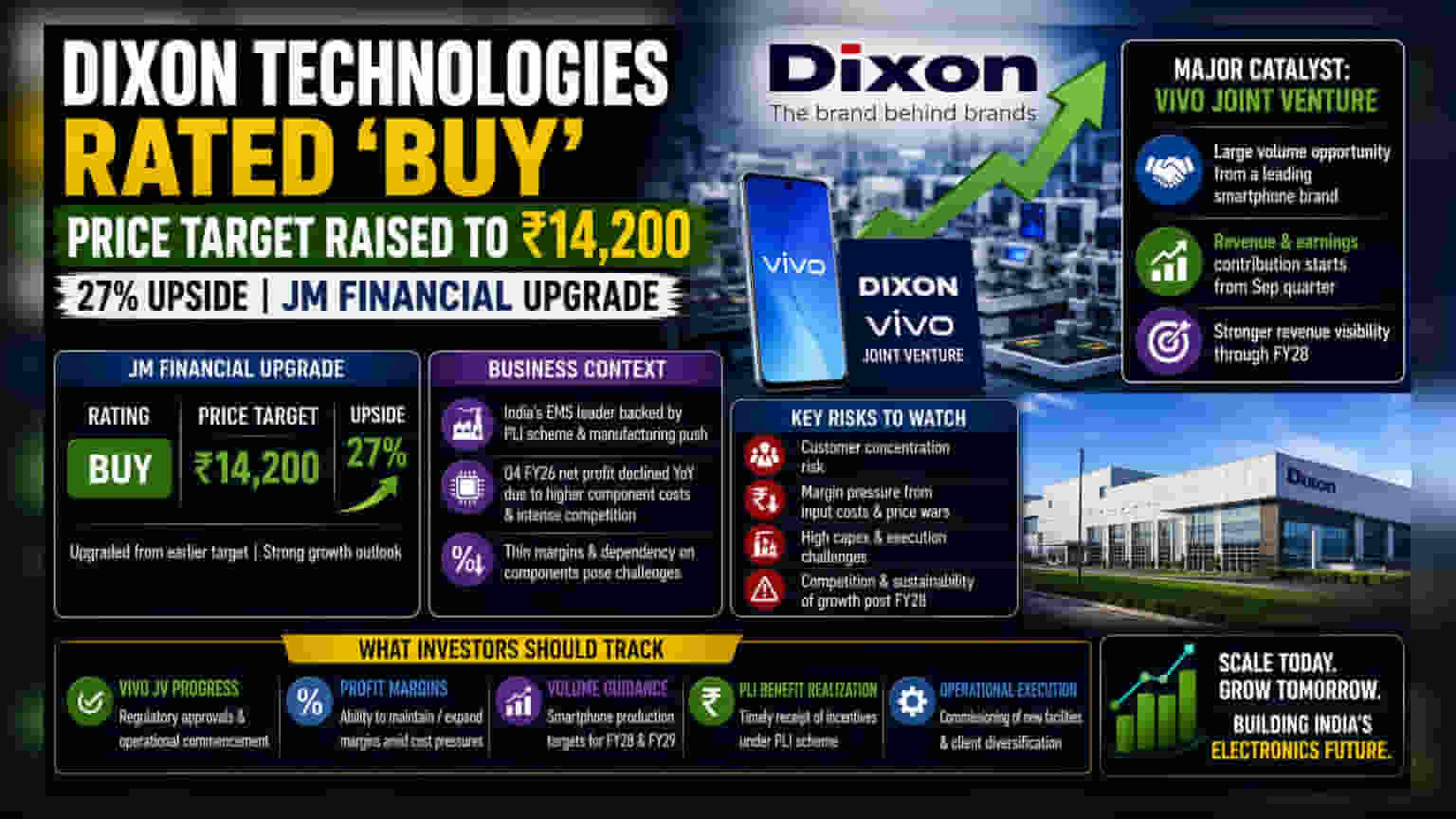

JM Financial has upgraded its rating on Dixon Technologies to 'buy' and increased its price target to Rs 14,200, representing a 27% upside from its previous estimate. The brokerage expects the electronics manufacturing services (EMS) company to see a significant uptick in its financial performance, driven largely by its proposed joint venture with smartphone manufacturer Vivo. This upgrade comes after recent investor meetings where the company highlighted its growth trajectory and expansion plans, despite a challenging quarter in the electronics sector.

The Vivo Partnership Logic

The central thesis for the upgrade is the Vivo joint venture, which is viewed as a major catalyst for Dixon's future smartphone volumes. Vivo remains a significant player in the Indian market, and a successful partnership could integrate a large portion of its manufacturing into Dixon's ecosystem. Analysts anticipate that this deal, once fully operational, will contribute to Dixon’s revenue and earnings starting from the September quarter. By manufacturing a substantial share of Vivo’s annual unit volumes, Dixon aims to solidify its position as a primary domestic EMS provider, effectively using its scale to improve revenue visibility through fiscal year 2028.

Business Context and Sector Pressure

While the market sees growth potential in Dixon's expansion, the company operates in a sector currently dealing with structural challenges. The EMS industry, while benefiting from India's electronics manufacturing push and the Production-Linked Incentive (PLI) scheme, faces significant margin risks. In the quarter ending March 2026, the company reported a year-on-year decline in consolidated net profit, which some market observers attribute to increased input costs for components like RAM and semiconductor chips, alongside intense price competition. The company's heavy reliance on assembly-based manufacturing means that even minor disruptions in the supply chain or fluctuations in component pricing can compress operating margins, which are already structurally thin.

Risks and Execution Hurdles

The road ahead for Dixon is not without obstacles. Analysts have pointed to several monitorable risks, including potential customer concentration—where a large share of revenue is dependent on a few key clients—and the pressure to manage capital expenditure. The transformation from a contract manufacturer to a more integrated electronics infrastructure player requires high operational efficiency. Additionally, some brokerages remain cautious, citing concerns over the sustainability of high revenue growth beyond FY28 if competition intensifies from new market entrants. The company must prove it can scale its capacity without sacrificing profitability, especially while balancing the upfront costs of new projects like display fabrication and mobile manufacturing facilities.

What Investors Should Track

For investors, the immediate focus will be the final regulatory progress and operational commencement of the Vivo joint venture. Beyond the deal, key monitorables include:

- Profit Margins: Whether the company can maintain or expand its operating margins amid elevated component costs.

- Volume Targets: Progress on the smartphone production guidance for FY28 and FY29.

- PLI Benefit Realization: Any delays or changes in the government's Production-Linked Incentive scheme that could impact cash flow.

- Operational Execution: The pace of commissioning for new manufacturing facilities and the company's ability to diversify its client base to reduce concentration risks.