Citigroup maintains a positive outlook on Eternal Ltd., projecting significant growth in its food delivery and quick commerce businesses for the June quarter. The brokerage anticipates better profit margins and increased order volumes, despite ongoing competition in the sector. Investors may track the company's ability to balance rapid expansion with operational efficiency.

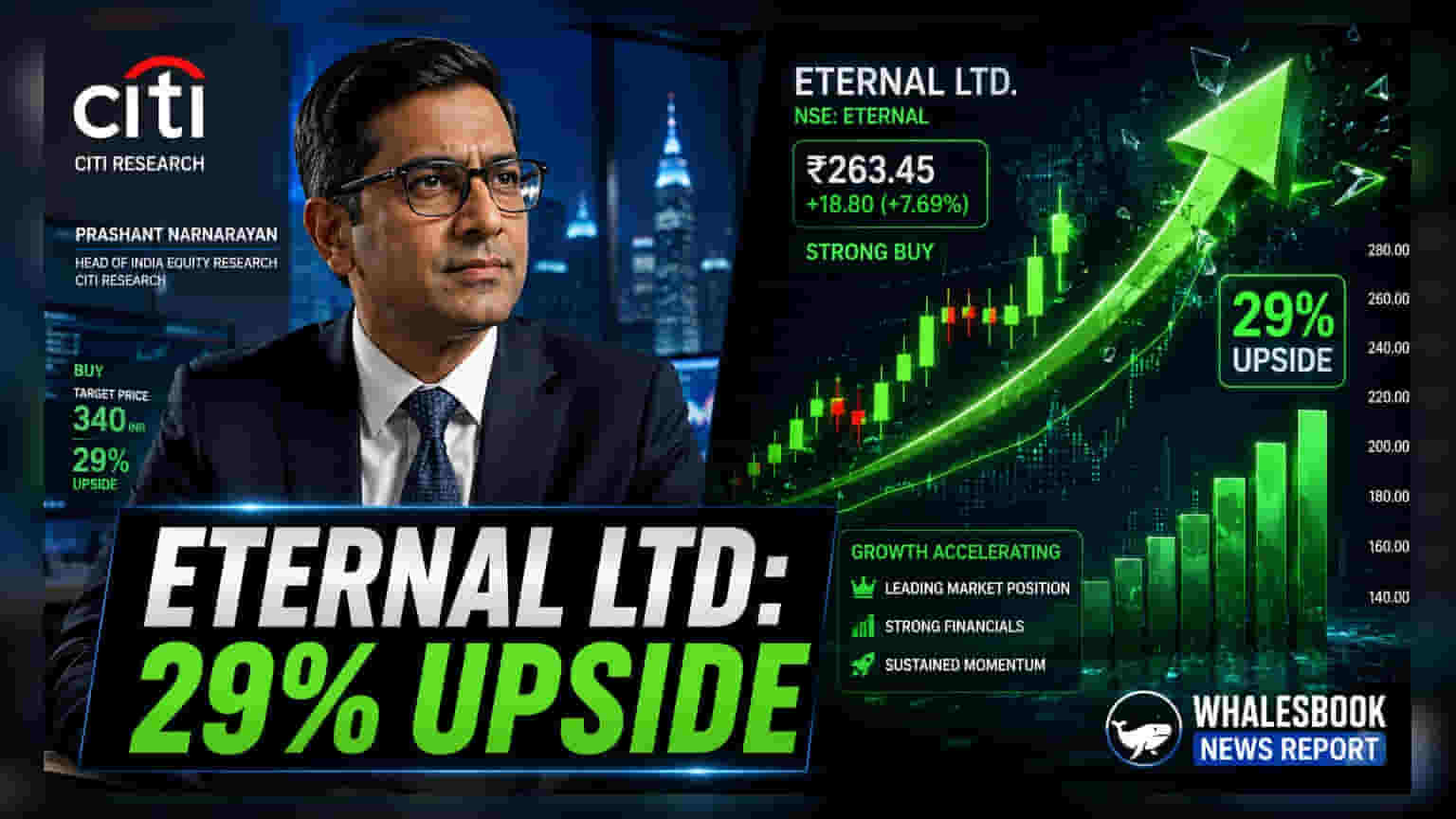

Citigroup has reaffirmed its positive stance on Eternal Ltd., setting a target price of Rs 360 per share. This assessment follows expectations of a strong performance in the upcoming June quarterly results. Analysts point to sustained demand in the food delivery segment and accelerated momentum in the Blinkit quick commerce unit as primary drivers for this outlook.

Food Delivery and Quick Commerce Performance

In the food delivery segment, growth is expected to be supported by a rise in monthly transacting users and higher average order values. Projections suggest a 22% year-on-year increase in gross order value for the quarter. Meanwhile, the quick commerce business, Blinkit, is anticipated to see a 15% quarter-on-quarter increase in net order value. The company’s strategy involves adding approximately 200 new stores, which is intended to improve operational leverage while maintaining a focus on profitability.

Profitability and Margin Trends

Citigroup highlights that margin expansion will be a critical factor for Eternal Ltd. in the coming months. The brokerage forecasts a 29% sequential increase in consolidated adjusted EBITDA to roughly Rs 5.5 billion. For Blinkit, the contribution margin is expected to reach 5.3% of net order value, reflecting a 140 basis point improvement year-on-year. These figures suggest that the company is moving toward greater efficiency even as it continues to invest in business growth.

Competitive Environment and Risks

While the outlook remains positive, the quick commerce sector is marked by intense competition and rapid changes. Investors should note that the company faces risks related to high cash spending, potential shifts in regulations, and the challenges of managing multiple high-growth business units. A critical factor for the company will be its ability to maintain profit margins while scaling its store count and customer base. The long-term performance will depend on whether Eternal can sustain its execution track record amid these competitive pressures.

Future updates that shareholders may monitor include the actual pace of store additions, the stability of contribution margins in the quick commerce segment, and management commentary regarding competitive pricing strategies. The company’s ability to manage its balance sheet while funding these aggressive expansion plans will also remain a primary area of focus for the market.