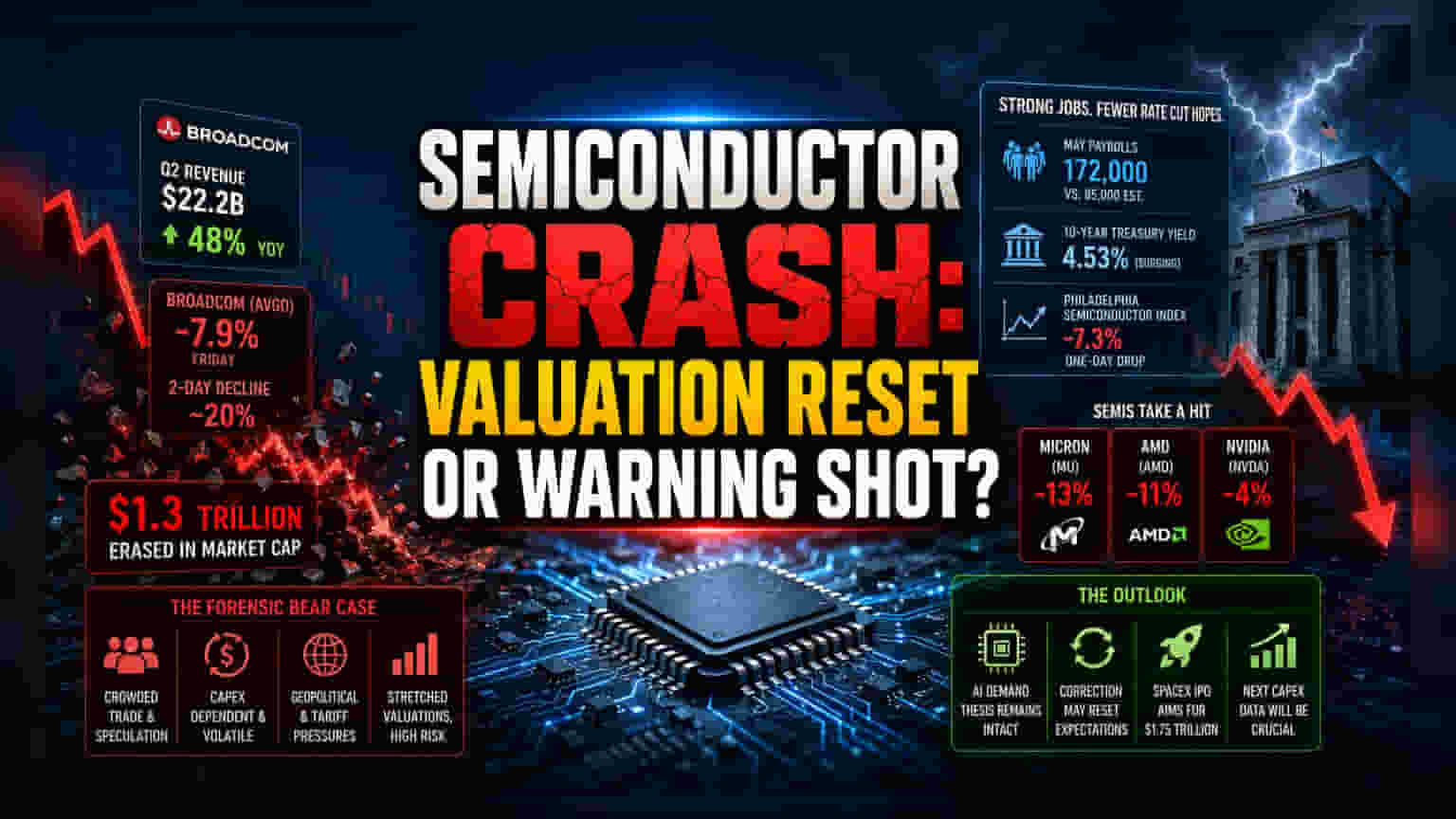

The Valuation Reality Check

The abrupt downturn in semiconductor equities this week serves as a stark reminder that perfection is the only metric rewarded in the current artificial intelligence trade. While Broadcom posted record quarterly revenue of $22.2 billion—a 48% year-over-year increase—the market’s reaction was punishing. Investors, who had priced the sector for exponential, unwavering growth, treated the company’s decision to maintain, rather than raise, its full-year AI revenue outlook as a structural failure. The resulting 7.9% decline in Broadcom on Friday, capping a two-day slide of nearly 20%, acted as the primary catalyst for a sector-wide contagion that erased $1.3 trillion in aggregate value.

Macro Tailwinds Turn into Headwinds

The semiconductor rout was significantly deepened by a cooling in broader market sentiment following a U.S. labor report that exceeded all expectations. The addition of 172,000 nonfarm payrolls in May, well above the 85,000 consensus, signaled a level of economic resilience that effectively crushed market hopes for imminent Federal Reserve rate cuts. With Treasury yields surging above the 4.50% threshold, the cost of capital has risen, presenting a punishing environment for high-valuation, long-duration growth assets. The Philadelphia Semiconductor Index, which had reached record highs just days prior, saw its valuation premium compressed in a single session as capital rotated toward more defensive, value-oriented corners of the market.

The Forensic Bear Case: Overcrowding and Speculation

Beyond the immediate macro pressures, the selloff highlights an increasingly fragile technical structure within the AI trade. Proprietary traders have noted that the sector’s 73% year-to-date gains were fueled by a "blindly buy-the-dip" mentality, a speculative habit that reached its limit this week. The sector’s extreme outperformance compared to the broader S&P 500 created a crowded trade where any deviation from perfection triggers reflexive profit-taking. Unlike more stable technology sub-sectors, many semiconductor participants are now tethered to volatile infrastructure spending cycles. Companies like Micron and AMD, which were hit with 13% and 11% declines respectively, remain highly vulnerable to capital expenditure fluctuations from hyperscale cloud providers. Furthermore, the industry is grappling with new geopolitical complexities, including Section 232 tariffs and the energy-intensive demands of data centers, which threaten to compress margins for manufacturers currently trading at historically high earnings multiples.

The Future Outlook

Despite the violent volatility, the long-term thesis for semiconductor dominance in the AI ecosystem remains intact for many institutional analysts. The current correction is viewed by some as a necessary reset of investor expectations rather than a breakdown of the underlying technology trend. As the market looks toward the upcoming SpaceX IPO, which aims for a record-setting $1.75 trillion valuation, investors are bracing for further portfolio reallocations. Whether this week's correction signals a tactical pause in the semiconductor bull market or the beginning of a deeper structural shift will likely depend on the next round of capital expenditure data from major tech hyperscalers.