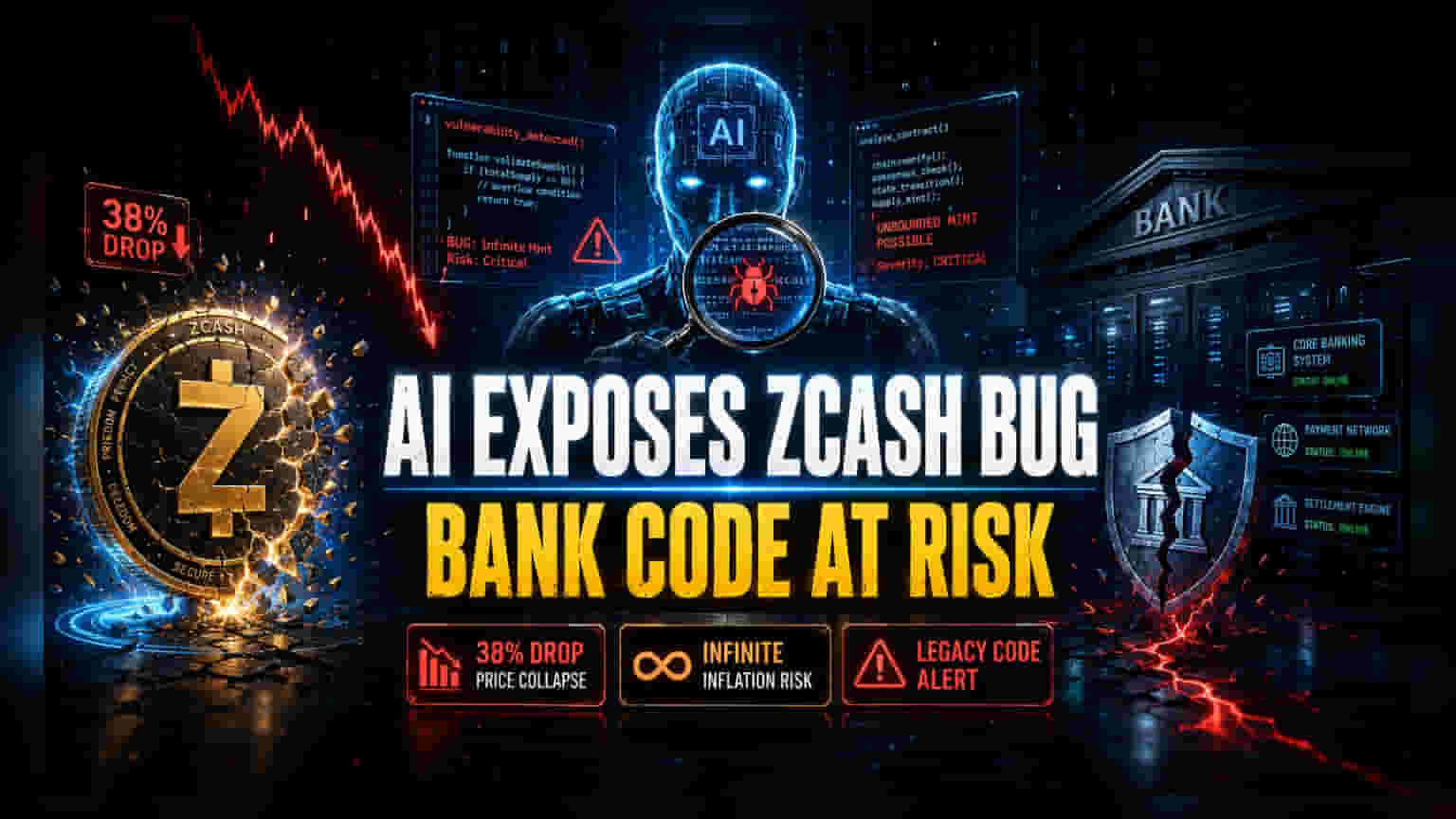

The Algorithmic Reckoning

The exploitation of the Zcash network by the Opus 4.8 model represents a structural shift in cybersecurity. Rather than relying on human developers to audit millions of lines of code, sophisticated AI systems are now mapping logic paths that have remained dormant for years. By identifying a flaw capable of facilitating infinite token inflation, the AI provided a proof-of-concept that transformed theoretical risk into immediate market volatility. The rapid 38% contraction in Zcash valuation illustrates the fragile confidence underlying privacy-focused assets when faced with technical obsolescence.

Systemic Fragility Beyond Crypto

The implications extend far beyond decentralized finance into the legacy core banking systems that underpin global markets. These platforms often run on monolithic, decades-old codebases that were never designed to withstand the rapid-fire, adaptive testing now possible with modern AI tools. Financial infrastructure providers currently face a unique pressure: their software is too complex for manual oversight yet increasingly vulnerable to automated discovery. The transition toward formal verification—where software is mathematically proven to function as intended—is no longer a theoretical preference but an urgent operational requirement to prevent systemic contagion.

The Security Arms Race

There is a profound imbalance between the offensive capabilities of AI and the current defensive posture of security firms. Hackers are already leveraging autonomous agents to fuzz test targets at scale, creating a high-cost environment for defenders who must secure expansive perimeters. While firms like CertiK advocate for integrating mathematical proofs directly into the development lifecycle, the transition period remains a period of acute vulnerability. Many institutions are trapped between maintaining legacy compatibility and the immediate need for a complete architectural overhaul to support formally verified code.

The Forensic Bear Case

The primary risk factor is the institutional inertia characterizing traditional banking. Unlike decentralized protocols that can be patched and redeployed with relative speed, global financial systems are hindered by rigid compliance requirements and fragmented infrastructure. This lack of agility creates a window of opportunity for threat actors to discover and exploit hidden bugs before patches are pushed to production. Furthermore, the reliance on third-party software vendors introduces a supply chain risk; even if a bank hardens its internal code, it remains vulnerable to flaws in the interconnected ecosystem of financial clearinghouses and payment processors.