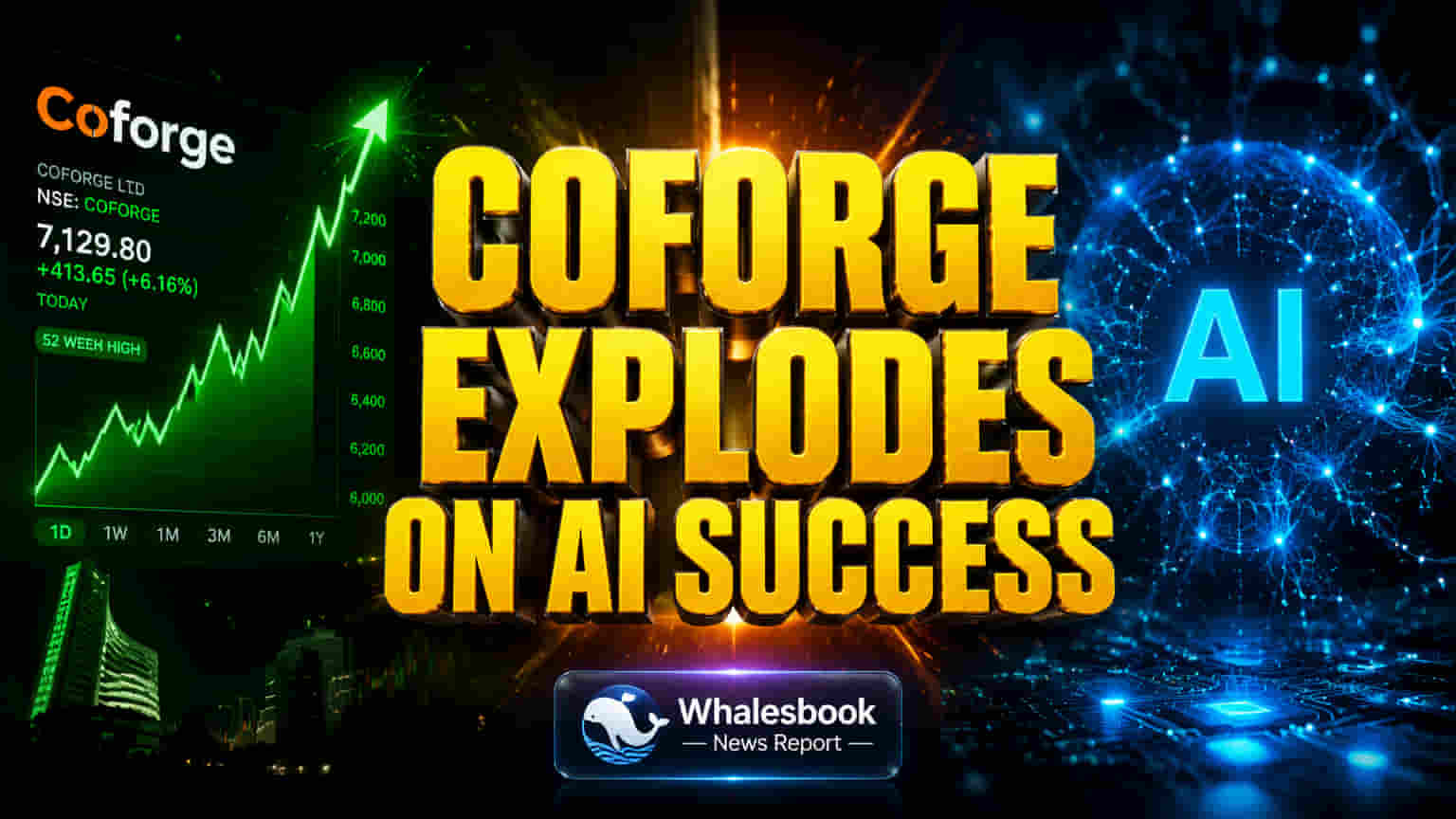

AI Fuels Strong Q4 Growth and FY27 Outlook

Coforge finished fiscal year 2026 with strong financial and operational performance. Revenue grew 29.2% year-over-year, showing strong market demand, while EBIT margins improved by 370 basis points to 14.4%. This was driven by increased use of AI services, boosting revenue and productivity. The company secured USD 648 million in new orders during the quarter. Its order book for the next 12 months grew 16.4% year-on-year to USD 1.75 billion, providing strong revenue visibility for FY27. CEO Sudhir Singh expects robust revenue growth and EBITDA over 20.5% for FY27. AI projects have shortened modernization and migration times, while improving internal operations like employee support and hiring.

AI Drives Growth Across Industries and Services

Growth was widespread across Coforge's industries. Travel, Transportation & Hospitality (TTH) grew 59.2%, Healthcare & HiTech 78.4%, and Government (outside India) 31.3%. Insurance rose 14.5%, and Banking and Financial Services (BFS) grew 5.5%. Service lines also expanded: Engineering up 32.3%, Business Process Management (BPM) by 33.7%, and Cloud & Infrastructure Management Services (CIMS) by 37.7%. The Americas led geographic growth at 34.6%, with Rest of World up 49.9% and EMEA at 14.3%. This broad performance shows strong market acceptance of Coforge's digital and AI services. Coforge cited AI client wins like conversational AI for call centers, AI validation engines in BFS, AI underwriting, GenAI for contract intelligence, and AI engineering platforms.

Valuation vs. Peers: A Premium for Growth

Coforge's valuation reflects investor optimism, with a P/E ratio around 37x. This is much higher than larger peers like Tata Consultancy Services (TCS) at approximately 16.79x, Infosys at 15.88x, and HCL Technologies at 18.76x. While Coforge's growth supports a premium, its P/E is closer to mid-cap firms like Persistent Systems (39.34x) or Tata Elxsi (37.76x). This premium suggests the market expects significant future growth and successful integration of the Encora acquisition. The Encora deal, cleared by regulators in April 2026, is set to create a company with about USD 2.5 billion in revenue, focusing on AI engineering, data, and cloud services.

Key Risks: Client Reliance and Integration Challenges

However, a key concern is growing client concentration. Revenue from the top five clients grew to 21.8% (from 18.3% a year ago), and the top ten clients represented 31.4% (from 27.9%). This reliance on a few major accounts is risky; any disruption or spending cuts from them could significantly affect Coforge's performance. Additionally, the Encora acquisition, while boosting AI and engineering skills, presents a major integration challenge. Merging operations, cultures, and clients smoothly, without harming existing business or adding new concentration risks, is crucial. Current strong performance and analyst 'buy' ratings (predicting up to 54% upside) depend on smooth integration and ongoing AI-driven deal wins. However, global economic uncertainty and delayed IT spending, especially in BFSI and retail, create a challenging demand environment.

Outlook: AI Leadership and Continued Growth

Coforge aims to be an AI-native engineering services leader, using its 'Quasar' AI platform and new capabilities from Encora. The company expects consolidated EBITDA margins over 20.5% for FY27. The Encora acquisition, finalized by April 2026, should strengthen its market position with greater expertise in AI, data, and cloud services. Analysts remain positive, with a consensus 'Buy' rating and average 12-month price targets around ₹1,677.55 INR, suggesting significant upside. Future success hinges on winning more large deals and effectively managing its client base.