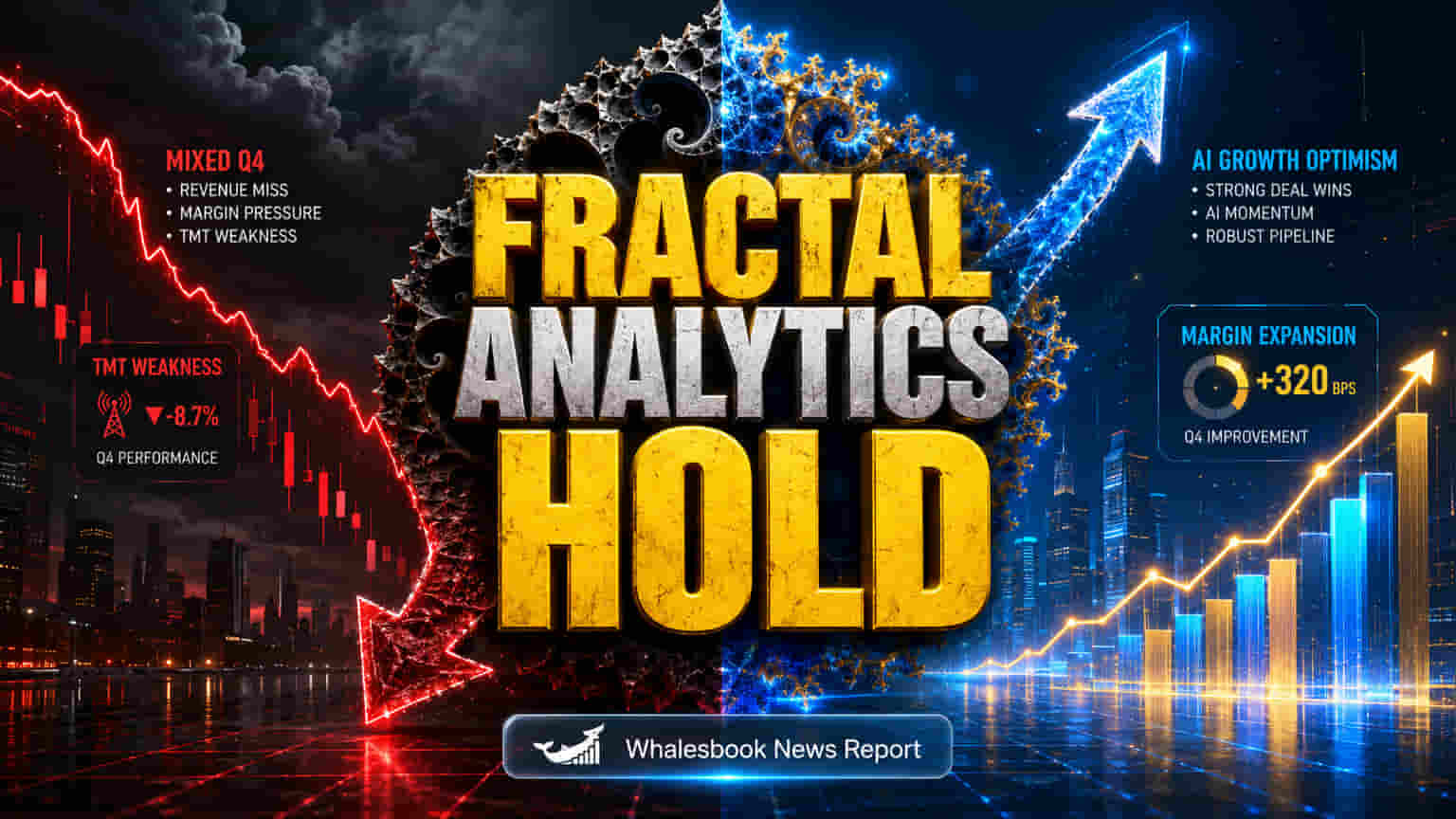

Analyst Downgrades Fractal Analytics After Q4 Mixed Results

Fractal Analytics has been downgraded to 'HOLD' by Prabhudas Lilladher, with a price target of INR 1,040. This move follows a fourth quarter where revenue grew only 3.7% sequentially, missing the 8.3% forecast. The slowdown was primarily due to a 14% drop in the Fractal.ai business, particularly within the Technology, Media, and Telecommunications (TMT) sector. However, the company surprised by expanding EBITDA margins by 530 basis points quarter-on-quarter, significantly exceeding the projected 260-basis point improvement and showcasing strong operational efficiency.

Growth Sectors Shine, Strategy Shifts to Outcome-Based Models

Excluding the TMT segment, Fractal Analytics saw robust growth, with other business areas expanding 27.5% year-on-year in FY26. The Healthcare and Life Sciences (HLS) sector was a standout, with Q4 revenue surging 82% year-on-year and contributing to 66% full-year growth. The Banking, Financial Services, and Insurance (BFSI) sector also posted solid 32% year-on-year growth for the full fiscal year. Management is focusing on shifting revenue models, aiming to increase the contribution of outcome-based contracts from the current 40% to approximately 60% over the next three years. This strategy is supported by a 5% year-on-year increase in revenue per billable Full-Time Employee (FTE) in FY26.

High Valuation Faces Scrutiny Against Peers

Fractal Analytics operates in a growing Indian IT services market. The company's market capitalization is around INR 18,400 crore. Its trailing twelve-month price-to-earnings (P/E) ratio is estimated between 80-115x, which is considerably higher than the industry average P/E for Indian software firms, typically around 19-22x. For comparison, eClerx Services trades at an 11-24x P/E, Latent View Analytics at 32-33x, and Happiest Minds Technologies at 27-32x. Fractal's premium valuation suggests investors expect continued rapid growth and margin expansion, especially from its AI offerings.

TMT Weakness and Client Concentration Pose Risks

Despite strong performance in key sectors, several risks remain. The sharp 19% year-on-year decline in the TMT segment in Q4 FY26 highlights the company's exposure to market downturns or client-specific issues. This segment's weakness, alongside revised analyst estimates cutting FY27/FY28 revenue growth to 16.4%/16.9% from earlier 21.5%/22.7%, points to potential near-term challenges. Client concentration is also a notable risk; for the six months ended September 30, 2025, the Fractal.ai segment received 54.2% of its revenue from its top ten clients, with one client alone contributing 8.2%. While net revenue retention (NRR) was 112% in Q4 FY26, indicating growth from existing clients, dependence on a few large relationships remains a vulnerability.

Outlook Uncertain Amidst Divergent Analyst Views

Fractal Analytics management is confident about medium-term growth, driven by increasing enterprise AI adoption and the shift to outcome-based revenue models. The company's focus on scaling IP-led products and AI transformation partnerships is expected to boost future profitability. However, analyst sentiment is divided. Prabhudas Lilladher moved to 'HOLD', while Goldman Sachs initiated coverage at 'Neutral' and Morgan Stanley at 'Overweight'. Some reports suggest a 'Buy' consensus, but others indicate an overall 'Sell' rating based on varied analyst inputs. These differing views highlight uncertainty about maintaining its premium valuation against segment challenges and the risks of executing its strategic transformation.