ICICI Prudential Life, Axis Bank, and Wipro are currently trading at lower price-to-earnings ratios compared to industry peers. While these valuations may catch an investor's eye, it is important to analyze the specific reasons behind these discounts, ranging from stake-sale pressures to growth expectations and tech-sector transitions.

In the Indian stock market, a low price-to-earnings (P/E) ratio is often the first step in identifying potential value. However, a lower valuation than the industry average does not always mean a stock is a bargain. It often reflects specific company-level situations, regulatory pressures, or sector-wide transitions that investors must weigh carefully against the company’s underlying performance.

ICICI Prudential Life and Regulatory Stake Dynamics

ICICI Prudential Life Insurance currently trades at a valuation discount relative to several private sector peers. Much of this has been linked to a technical overhang rather than a decline in business quality. Prudential plc is required to reduce its stake in the insurer due to its involvement with Bharti Life Insurance. This planned sale has historically created pressure on the stock price. Operationally, the company has shown resilience, recently reporting a 10.9% year-on-year growth in the Value of New Business (VNB) and a VNB margin of 24.7%. Profitability remains strong, with a reported 34.6% increase in net profit, suggesting that the valuation gap may be influenced more by share supply dynamics than by operational fundamentals.

Axis Bank’s Asset Quality Focus

Axis Bank represents a different scenario within the private banking sector. Despite its status as one of India's largest lenders, it has frequently traded at a lower P/E multiple compared to some high-growth private banking rivals. The bank’s recent performance highlights a focus on asset quality, with gross non-performing assets (NPAs) falling to 1.23%. Credit costs are also on a downward trend, which traditionally helps improve return on equity. Investors often monitor Axis Bank’s ability to maintain its growth in advances—which grew 19% year-on-year—while keeping credit costs in check. The management's strategy of calibrated growth in a volatile macroeconomic environment remains the key indicator for long-term health.

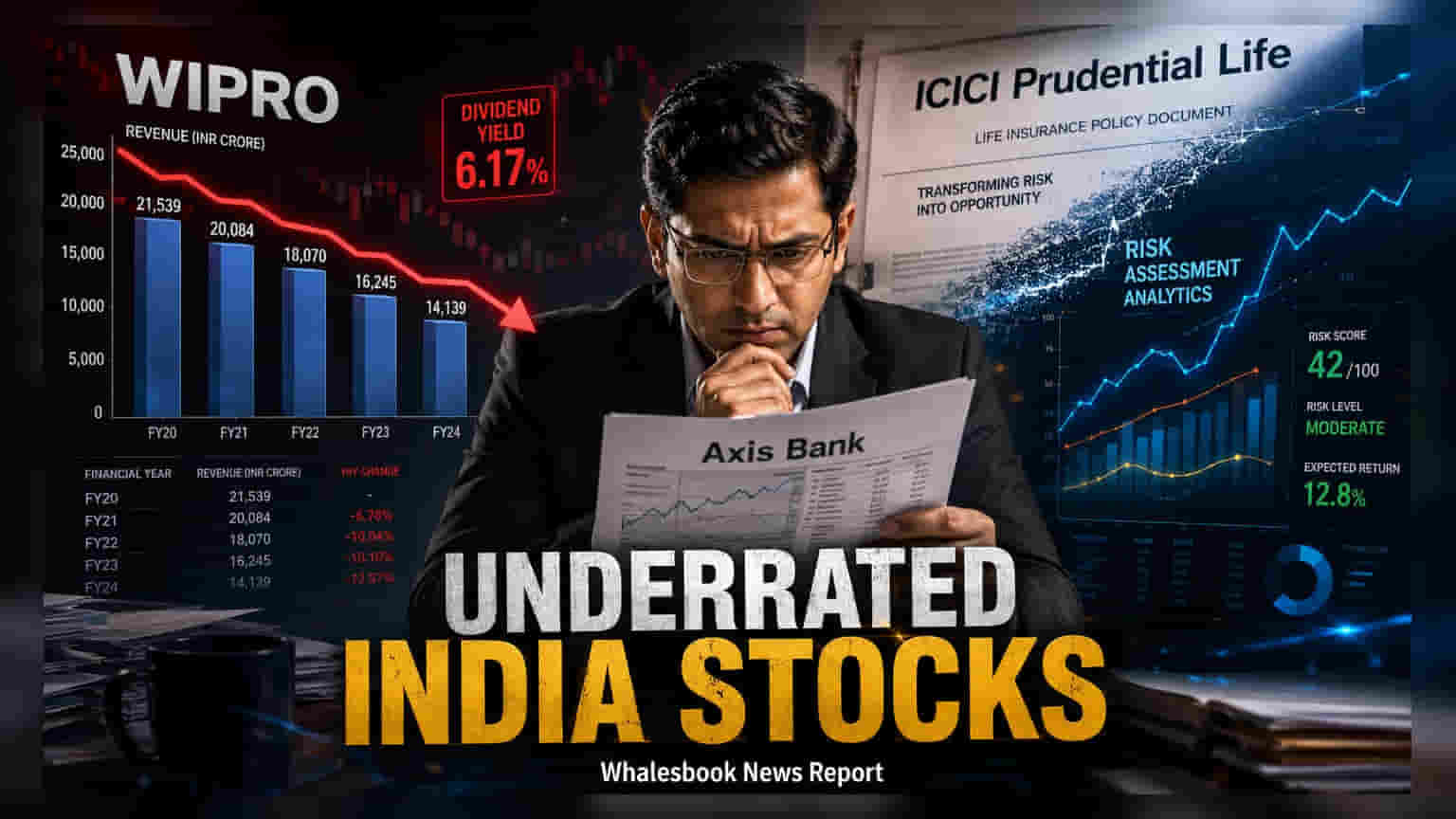

Wipro’s Strategic Pivot and Yield Appeal

Wipro trades at a valuation discount largely due to the market’s perception of its growth pace compared to larger IT peers like TCS or Infosys. The company is currently undergoing a significant transition, focusing heavily on AI-native business units to move toward a more software-focused services model. In the fourth quarter of FY26, it reported $2.65 billion in IT services revenue and $3.5 billion in new order bookings. For many investors, Wipro’s attraction currently lies in its cash return policy, evidenced by a dividend yield of 6.27%, which provides a steady income component that is often absent in faster-growing tech stocks. The next monitorable for the company is whether its AI investments can translate into margin expansion and higher growth rates to close the valuation gap with its sector peers.