Ace investor Dolly Khanna has reduced her stakes below 1% in GHCL, IFB Agro, and KCP Sugar. The exits follow concerns over declining sales, weak return ratios, and poor core operational profitability. These moves serve as a reminder for investors to look beyond stock price and focus on the quality of underlying business performance.

What Happened

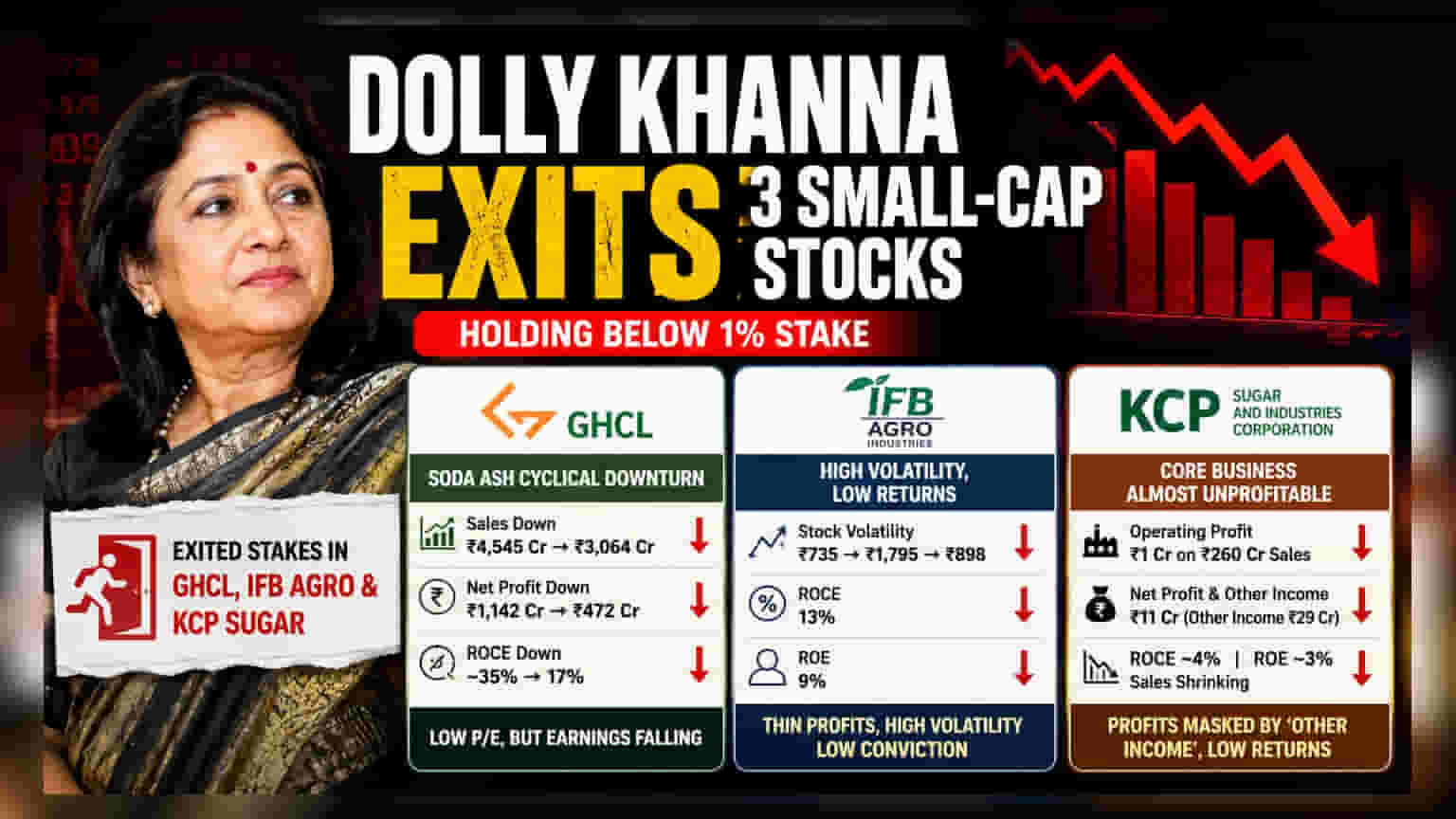

In recent shareholding disclosures, prominent investor Dolly Khanna has exited her positions in three small-cap companies: GHCL Ltd, IFB Agro Industries, and KCP Sugar and Industries Corporation. In all three cases, her holding has fallen below the 1% threshold, meaning she is no longer a significant shareholder required to disclose her stake publicly. While individual investment decisions are personal, the exits come after a period of weakening operational performance and financial results for these companies.

GHCL: The Challenge Of A Downward Cycle

GHCL, a key player in the soda ash industry, has faced a difficult period, with financial results showing a decline from the highs seen in fiscal year 2023. Annual sales have dropped for three years in a row, falling from Rs 4,545 crore to Rs 3,064 crore by fiscal year 2026. During this time, net profit has fallen by more than half, from Rs 1,142 crore to Rs 472 crore.

For investors, the key concern here is the return on capital employed (ROCE), which indicates how efficiently a company uses its money to generate profits. This figure has dipped from roughly 35% to 17%. While the stock may appear inexpensive with a low price-to-earnings (P/E) ratio, investors should be cautious, as falling earnings can sometimes make a stock look cheaper than it actually is.

IFB Agro: Volatility And Low Returns

IFB Agro Industries, which operates in the industrial alcohol and marine foods sectors, has seen a swift exit from the investor’s portfolio after only a short holding period. The company struggled with an operating loss in fiscal year 2024. Although it returned to profit in 2026, the return on capital employed and return on equity remain low at 13% and 9% respectively.

The stock has also experienced extreme price swings, moving from Rs 735 in June 2025 to a high of Rs 1,795 in January 2026, before falling to Rs 898. Such high volatility combined with a thin earnings base often makes it difficult for long-term investors to maintain conviction in the business.

KCP Sugar: Core Business Weakness

KCP Sugar and Industries Corporation presents a concerning picture regarding the quality of its profits. In fiscal year 2026, the company recorded sales of Rs 260 crore but managed an operating profit of only Rs 1 crore, meaning its core business generated almost no profit margin. A significant portion of its Rs 11 crore net profit came from 'other income' of Rs 29 crore, which masks the underlying struggles in its sugar, spirit, and ethanol operations.

Furthermore, the company has seen sales shrink over the past five years, with return ratios (ROCE and ROE) staying at minimal levels of about 4% and 3%. While the stock trades below its book value, this can be a warning sign of a business that is not generating enough value for shareholders.

What Investors Should Track Next

These exits highlight the importance of looking beyond headline numbers like low P/E ratios or low stock prices. When evaluating such companies, investors should track:

- Quality of Profit: Does the profit come from core business operations, or is it heavily dependent on 'other income' or one-time gains?

- Return on Capital: Is the company actually generating efficient returns on the money invested in the business?

- Sales Consistency: Is the company growing its top-line sales, or is it in a long-term decline?

- Operational Margins: Is the core business profitable enough to sustain itself without outside help?

Investors may use these signals to re-evaluate whether their holdings in similar small-cap stocks are backed by strong business fundamentals or if they are simply holding onto declining assets.