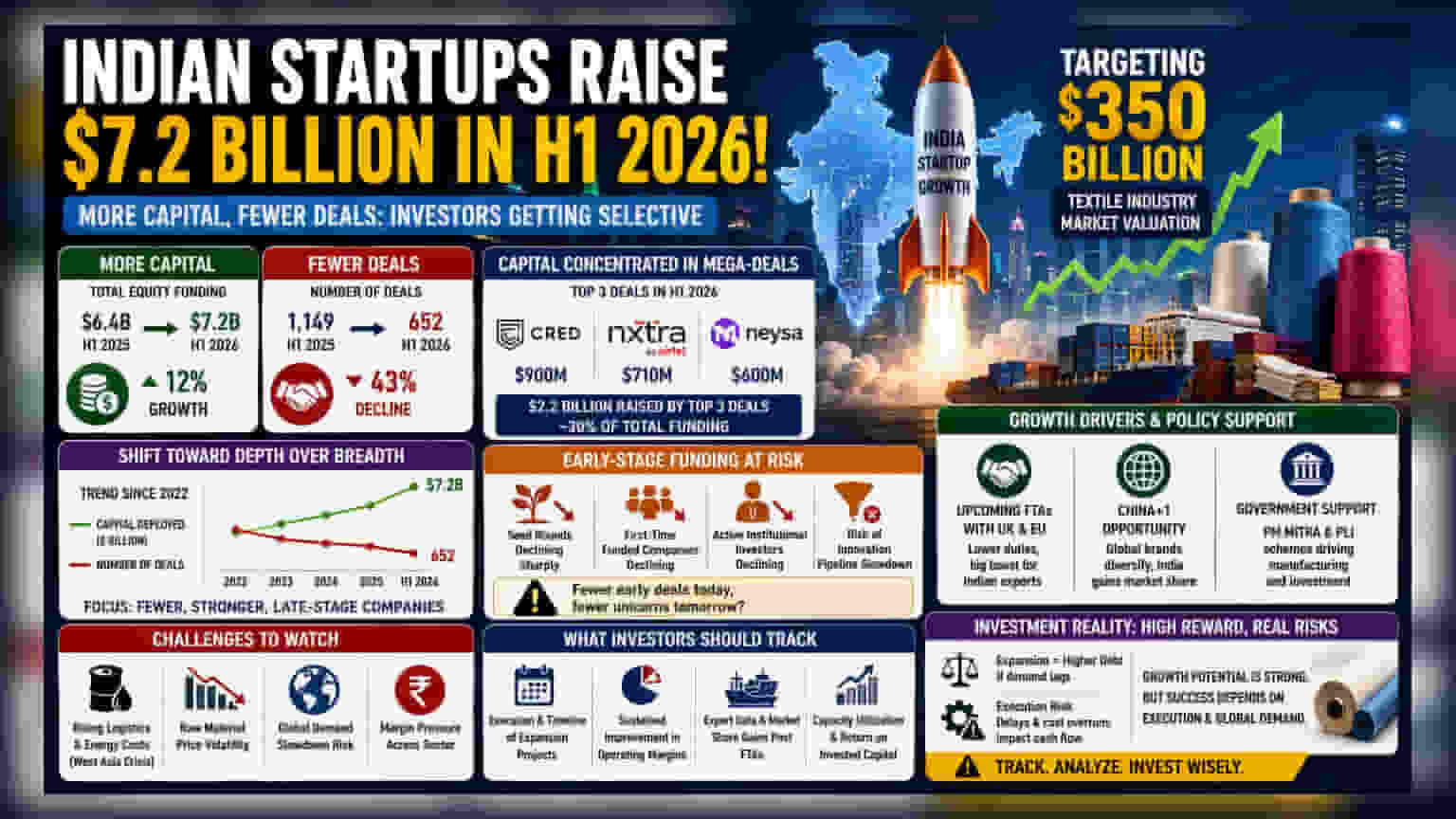

Indian startups raised $7.2 billion in the first half of 2026, a 12% increase from the previous year. While total capital grew, the number of funding rounds dropped by 43%, signaling a shift where investors are betting large sums on fewer, established companies. This trend highlights a tightening pipeline for early-stage firms.

What Happened

Indian startups secured $7.2 billion in equity funding during the first six months of 2026. This represents a 12% growth in total capital compared to the same period in 2025. Despite this increase in money flow, the number of deals fell sharply by 43%, dropping from 1,149 rounds to 652 rounds. This data, reported by market tracker Tracxn, highlights a market where investors are significantly more selective with their capital.

The Shift Toward 'Depth Over Breadth'

For several years, the Indian startup ecosystem operated on high volumes of deals. The current landscape shows a distinct move away from this. Instead of spreading smaller amounts of capital across a wide portfolio, institutional investors are focusing on fewer, more mature companies. This strategy aims to support proven business models that have demonstrated a clear path to profitability or market leadership. This trend has been visible since 2022, but the 2026 data shows the gap between the number of funded companies and the total capital deployed is widening.

Concentration of Capital in Mega-Deals

A significant portion of the total $7.2 billion raised is concentrated in just three massive transactions. CRED secured $900 million, Nxtra raised $710 million, and Neysa attracted $600 million. Together, these three deals account for $2.2 billion, or nearly 30% of all funding in H1 2026. This level of concentration suggests that capital is flowing heavily toward late-stage companies with established operations, data infrastructure, or high-value AI capabilities, rather than being distributed across the broader startup spectrum.

The Early-Stage Funding Risk

While late-stage funding is robust, the health of the early-stage pipeline is a concern. The number of seed rounds and first-time funded companies has declined sharply. Furthermore, the total count of active institutional investors has dropped, which may create a bottleneck for the next generation of startups. Without a steady influx of early-stage capital, the ecosystem faces a risk of a slowing innovation pipeline. While 13 technology IPOs were completed in H1 2026, suggesting strong exit opportunities for mature companies, the long-term impact of fewer early-stage investments could affect the total number of future IPO candidates.

What Investors Should Track Next

Investors should monitor whether the current focus on late-stage and AI-related companies continues or if it leads to a supply gap in new high-quality startups. The key monitorable will be the trend in early-stage deal volumes in the second half of the year. If seed funding continues to contract, it may indicate a long-term challenge in developing the next wave of unicorns. Additionally, market participants will watch whether the shorter time from first funding to IPO becomes a standard trend or remains limited to a select group of capital-intensive sectors like data centers and AI.