The Shifting Negotiation Landscape in India

India's venture capital scene, once known for rapid growth and founder-friendly terms, is undergoing a major shift. As the market matures, driven by global economic changes and a focus on profitability, investors hold more sway. This move away from "growth at all costs" toward disciplined profitability means deal terms increasingly favor investors, with liquidation preferences leading the way. The growing complexity of these clauses, influenced by global trends and geopolitical uncertainties, makes it tougher for founders to protect their equity. Market corrections and the difficulties many startups face have intensified this, pushing investors to seek better protection.

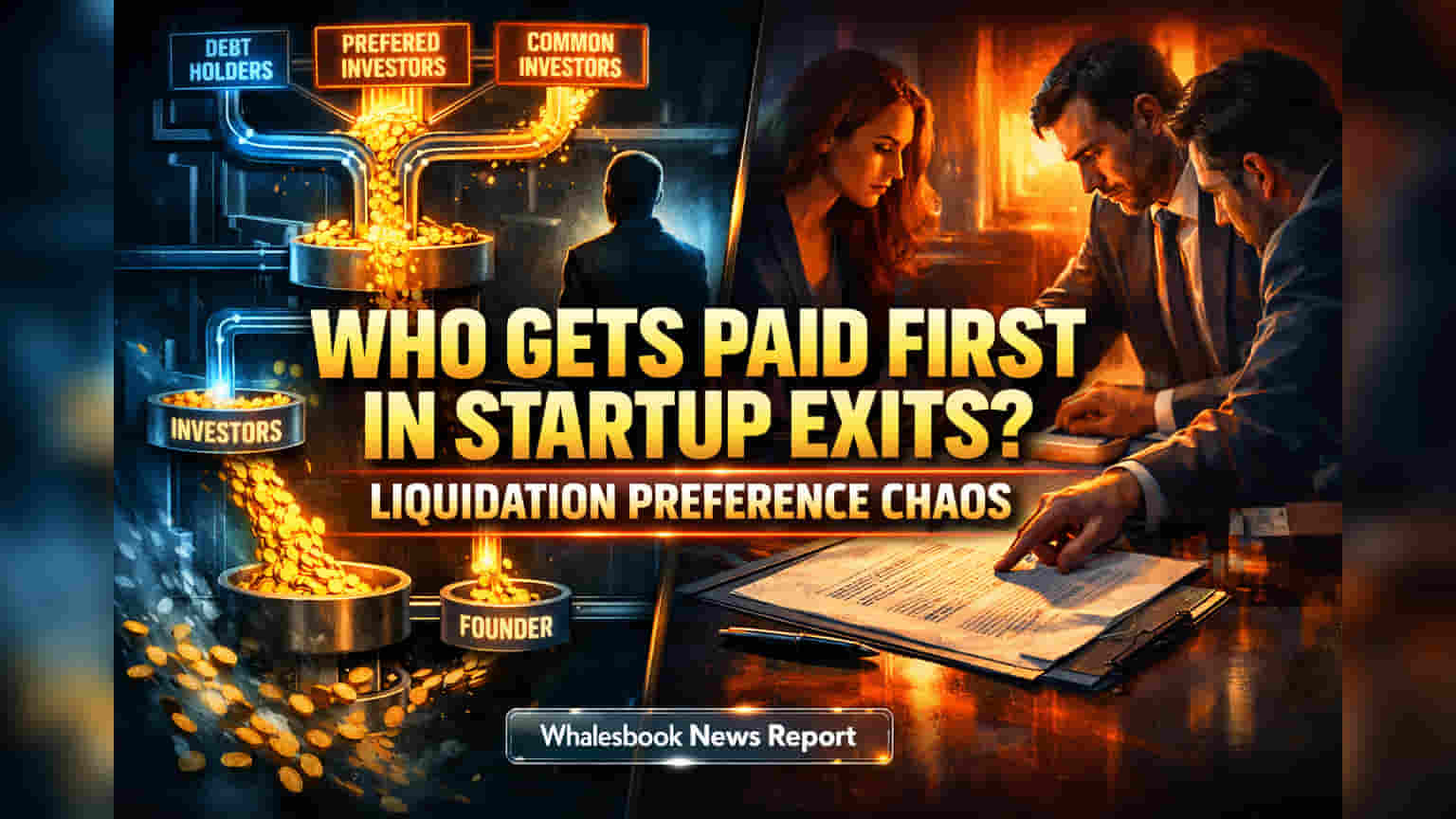

How Liquidation Preferences Can Erase Founder Value

The core issue for founders is how aggressive liquidation preferences can systematically reduce their final payout. Participating preferences, known as "double-dipping," let investors recover their initial investment and then take a share of the remaining profits. This dual recovery significantly cuts the capital available for common shareholders, which usually includes founders and employees. The rise of stacked or seniority-based preferences, where later investors get paid before earlier ones, further worsens founder dilution. With modest exits, high multiples (like 2x or 3x the investment) combined with stacked preferences can fully repay investors. This leaves founders and early employees with minimal or no return, even if the company exits at a valuation well above its total invested capital.

Global Trends and Indian Legal Nuances

Globally, liquidation preference negotiations show regional differences. The U.S. market often features more founder-friendly 1x non-participating terms, while parts of Asia tend to have stricter deal structures. In India, the mix of investor contract rights and legal statutes adds complexity. Laws like the Companies Act, 2013, and the Insolvency and Bankruptcy Code (IBC) offer a foundation, but applying them to complex liquidation preferences isn't always clear. The IBC's payment order could override contracts in formal insolvency, but enforcing contractual obligations against a company and its promoters is still debated legally. This uncertainty requires careful drafting and a clear grasp of potential enforcement issues.

The Extreme Risk: Preferences Wiping Out Founders

The biggest risk for founders is that aggressive liquidation preferences can completely eliminate their equity value at exit. "Double-dipping" from participating preferences diverts returns that would otherwise go to founders. When combined with stacked seniority, this can wipe out founders and even earlier investors, even in deals that look like exits. The definition of a "liquidation event" can be tricky, with broad terms potentially triggering preference payouts when a full exit wasn't intended. The harshest outcome occurs when aggressive liquidation preferences are combined with drag-along rights. These rights allow majority shareholders, often investors, to force all shareholders to sell. This can trap founders in transactions where preferences are paid, but founders receive nothing. Such terms can demoralize employees and hinder future fundraising, showing a potential failure to align incentives for long-term growth.

Protecting Your Stake: What Founders Can Do

In this changing market, founders need to be extremely careful when negotiating liquidation preferences. The typical founder-friendly term is a 1x non-participating liquidation preference, which gives investors downside protection while keeping significant upside for founders. Founders should strongly resist participating clauses or multiples higher than 1x unless the valuation and exit potential clearly support them. It is essential to hire experienced legal counsel specializing in venture capital deals to navigate the complex terms and potential traps. Founders must thoroughly model various exit scenarios and understand how different preference structures will affect their personal returns before signing any term sheet. The startup ecosystem's long-term health relies on finding a balance that protects investor capital without discouraging the entrepreneurs who drive innovation.