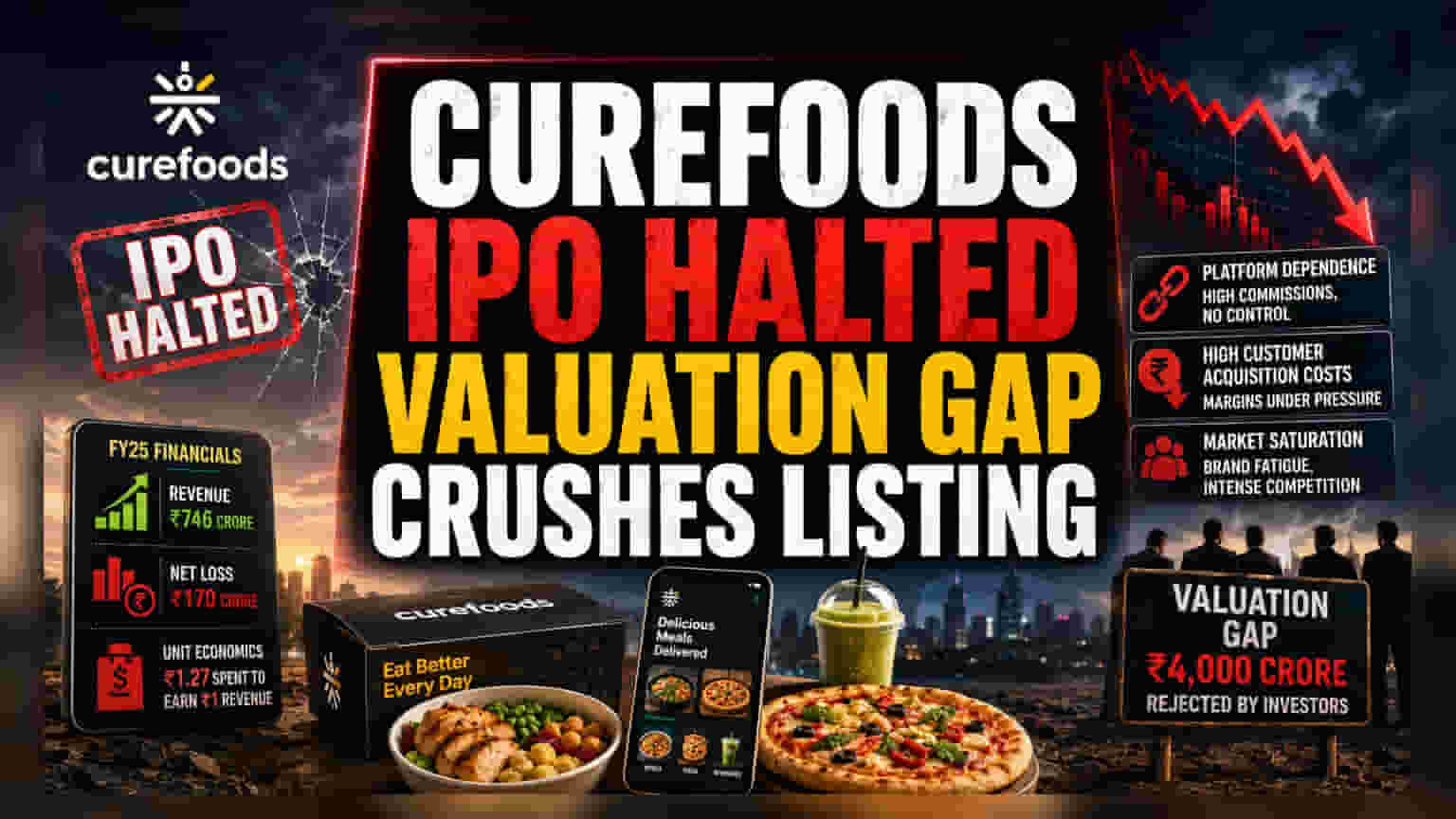

The Valuation Disconnect

Curefoods' decision to halt its public listing marks a sharp correction in investor sentiment toward the Indian food-tech sector. Despite securing regulatory approval in October 2025, the company failed to bridge the valuation gap during intensive roadshows. Institutional investors and mutual funds, increasingly wary of loss-making new-age entities, balked at the company’s requested Rs 4,000 crore valuation. This refusal forced a strategic retreat, as the company chose to prioritize long-term stability over a dilutive, underpriced public offering.

The Operational Reality

The firm’s financial profile underscores the difficulty of justifying high valuations in a challenging macroeconomic environment. While the company achieved operating revenue of approximately Rs 746 crore in FY25, it sustained a net loss of roughly Rs 170 crore. Critically, unit economics remain strained, with the business spending approximately Rs 1.27 to generate every rupee of operating revenue. These figures have left investors demanding clearer paths to sustainable profitability rather than mere topline expansion, contrasting with the more aggressive, growth-at-all-costs strategies seen in previous cycles.

Sector-Wide Contagion

Curefoods is not an outlier but rather the latest casualty of a cooling IPO market for Indian technology firms. Major industry peers, including Flipkart and PhonePe, have similarly deferred their listing plans, citing unpredictable market volatility and a crowded, cautious pipeline. Unlike the 2021-2022 period where optimism fueled premium pricing, the 2026 market climate is characterized by rigorous fundamental scrutiny. Investors are now heavily discounting cloud kitchen models that remain deeply dependent on third-party aggregators—a reliance that introduces structural vulnerability to fee increases and changing platform algorithms.

Structural Vulnerabilities

The Bear Case against the current cloud kitchen business model centers on two primary risks: platform dependence and high customer acquisition costs. Because many operators lack direct, owned-channel customer relationships, they remain vulnerable to the ranking and commission structures of dominant food delivery platforms. Furthermore, the saturation of the Indian food-tech market has led to 'brand fatigue' and intense competition, where profit margins are consistently compressed by the need to fund aggressive discounts to maintain order volumes. For Curefoods, while expansion into diverse categories—from health meals to pizza and beverages—has built scale, it has also increased operational complexity and capital intensity. The inability to secure a higher public valuation suggests that the market now views these brands more as high-burn assets than as defensive, profit-generating utilities.