The Shift in Market Mechanics

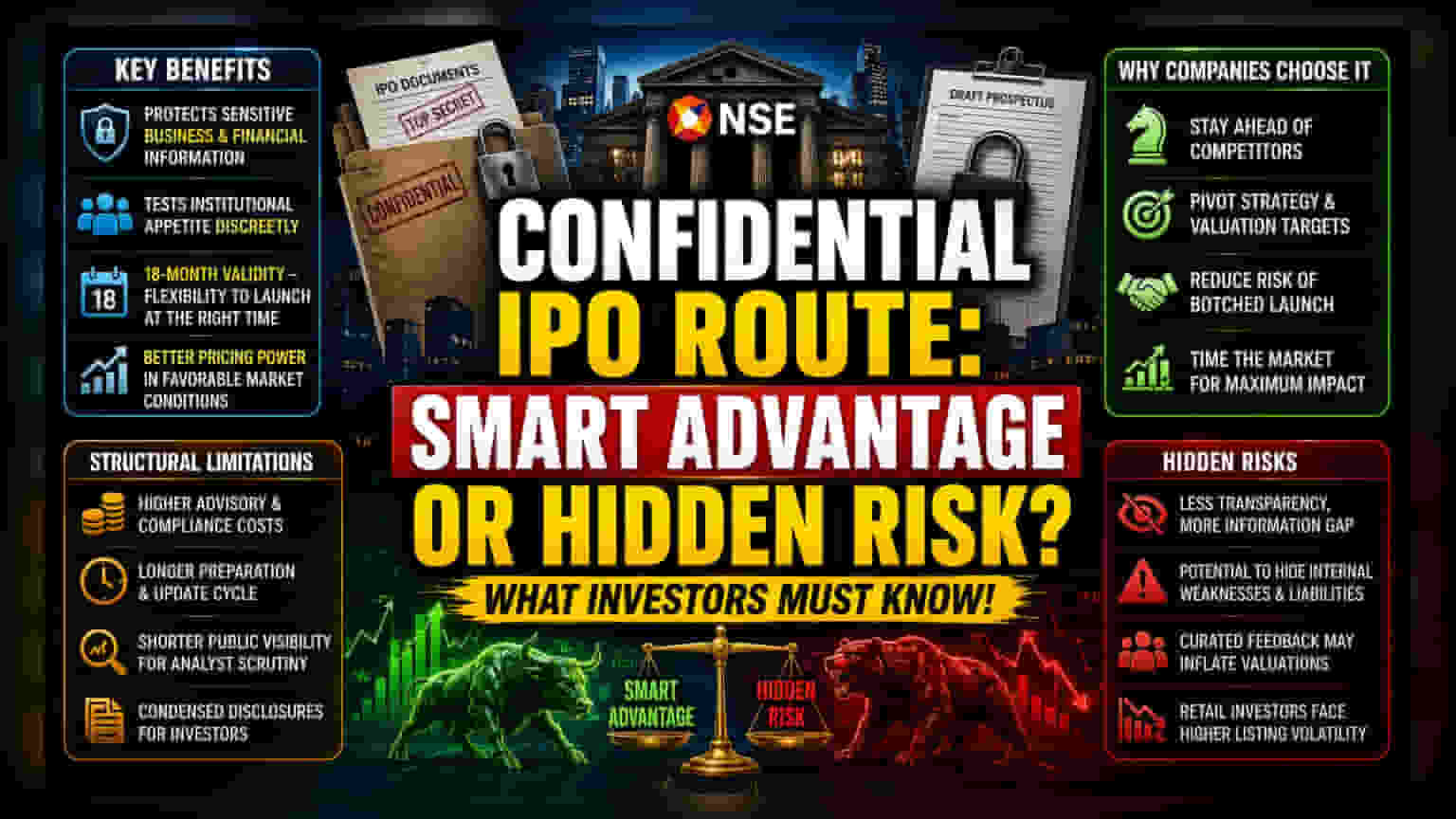

The reliance on the confidential filing route signals a departure from the traditional transparency-first model that previously defined Indian primary market entries. By opting for a phased disclosure approach, issuers are effectively insulating their growth narratives and proprietary financial metrics from competitors during the sensitive pre-IPO preparation phase. This defensive posture is increasingly common among firms wary of shifting macroeconomic signals, allowing leadership teams to pivot their valuation targets in real-time as market sentiment fluctuates.

Valuation Arbitrage and Regulatory Stance

Unlike the standard route, which triggers immediate public disclosures of competitive advantages and risk factors, the confidential process functions as a regulatory sandbox. Issuers gain the ability to test institutional appetite through discreet engagements with Qualified Institutional Buyers before committing to a public price band. This controlled environment minimizes the risk of a botched launch, which often stems from sudden shifts in liquidity or sector-specific headwinds. The extension of the approval validity window to 18 months provides a critical buffer, enabling companies to wait for favorable interest rate cycles or improved market liquidity that might otherwise undermine a traditional offering.

Structural Limitations and Investor Hurdles

While the confidential route is touted for its flexibility, it imposes significant operational burdens. The extended preparation period forces issuers to bear prolonged advisory and compliance costs, often necessitating multiple rounds of legal and accounting updates to keep filings current. From a market efficiency standpoint, the reduced duration of public visibility limits the timeframe for independent analysts to stress-test financial projections, potentially leading to more volatile price discovery upon listing. Investors must rely on condensed final prospectuses, which may omit the nuanced history of iterative regulatory feedback that often shapes a company’s risk profile.

The Forensic View: Hidden Risks

The move toward shadow filings raises questions regarding the democratization of information. Critics argue that the increased reliance on this mechanism may mask internal weaknesses or evolving legal liabilities that would normally be exposed earlier in the public record. Furthermore, companies with complex capital structures or history of regulatory friction are leveraging this opacity to control the narrative surrounding their debut. Without the early-stage scrutiny of the public eye, firms may attempt to inflate valuation expectations through curated institutional feedback, potentially creating a valuation gap that retail participants bear the cost of once the stock trades openly.