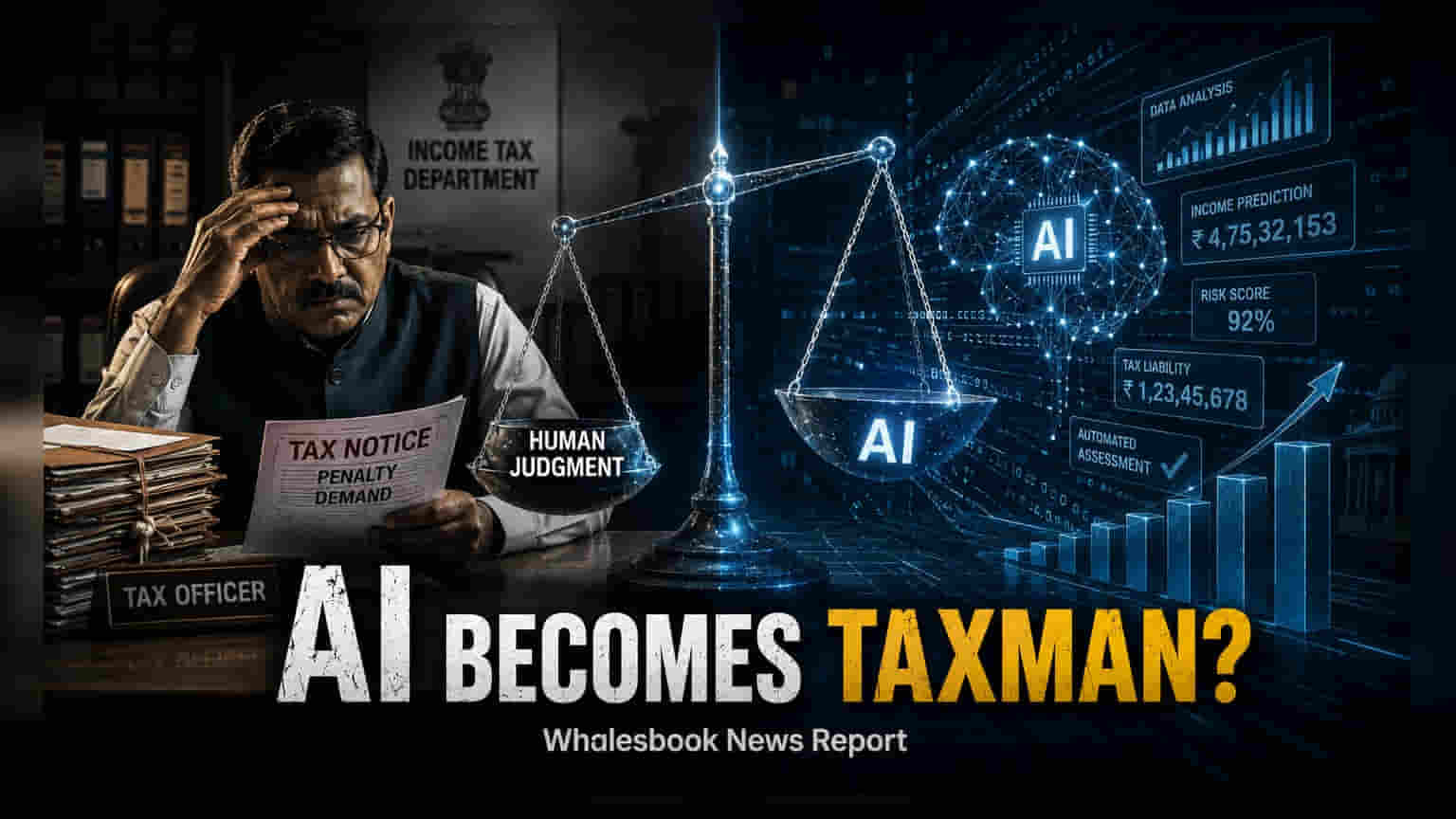

India’s GST system now uses AI to process over a billion monthly invoices, successfully identifying ₹25,000 crore in fraudulent claims. However, the automated approach to flagging tax risks and suspending registrations has raised concerns regarding transparency and natural justice. Businesses and legal experts are increasingly questioning whether algorithmic decisions provide enough clarity to taxpayers during scrutiny.

The integration of Artificial Intelligence and Machine Learning within India's Goods and Services Tax (GST) framework marks a major shift in how the government detects tax evasion. With the system now processing more than a billion invoices each month, authorities are leveraging these digital tools to identify complex patterns that manual audits might miss. The Business Intelligence and Fraud Analytics (BIFA) tool has become central to this strategy, integrating data from multiple financial sources to assign risk scores to businesses.

This technology-driven approach has produced tangible results in the fight against tax fraud. Recent enforcement drives have led to the detection of more than 29,000 fake GST registrations and recovered or blocked approximately ₹25,000 crore in fraudulent Input Tax Credit (ITC) claims. For high-risk entities flagged by the system, the government has introduced mandatory biometric and in-person verification at GST Suvidha Kendras to ensure legitimacy.

Challenges to Algorithmic Oversight

Despite these gains in administrative efficiency, the reliance on automated systems has sparked debate over the legal rights of taxpayers. A primary concern is the transparency of the decision-making process. When the system issues a show-cause notice based on a high-risk score without clearly explaining the parameters or logic behind that score, it complicates a taxpayer's ability to provide a meaningful defense. This lack of detail in communication is often cited as a hurdle to the principle of natural justice, which requires that individuals be informed of the case against them.

Legal experts are also questioning the balance between machine-led alerts and human oversight. Under existing tax laws, the decision to initiate proceedings requires a 'reason to believe' from a proper officer. There is growing concern that a mechanical reliance on machine-generated flags, without a clear, documented application of independent judgment by tax officials, could make enforcement actions vulnerable to legal challenges in court. Furthermore, the suspension of a GST registration—often a result of these algorithmic flags—can immediately paralyze a small business's operations, making the subsequent appeal process a significant financial burden for smaller players.

Future Governance and Taxpayer Protection

As India continues to refine its digital tax infrastructure, the conversation is shifting toward the need for a formal governance framework. Global benchmarks, such as the EU's AI Act, categorize the use of AI in tax administration as a high-risk area, necessitating strict transparency and human-in-the-loop oversight. Similar calls for 'algorithmic impact assessments' are being made domestically to disclose error rates and potential biases in the models used by the Central Board of Indirect Taxes and Customs (CBIC) and the GST Network (GSTN).

For investors and business owners, the next phase of this evolution will likely involve potential legislative or procedural changes. Taxpayers should track whether the government moves to amend the Central Goods and Services Tax (CGST) Act to define the legal scope of AI-based decisions. Increased disclosure requirements regarding how risk scores are calculated, along with mandatory human verification steps, remain the most important monitorables for ensuring that technological efficiency does not come at the cost of legal clarity.