The Shift Toward Targeted Enforcement

The latest directives from the Central Board of Direct Taxes mark a transition from blanket, system-generated audits to a more surgical methodology for the 2026-27 cycle. While the Computer Assisted Scrutiny Selection mechanism remains active for general discrepancies, the new guidelines prioritize entities already flagged by field intelligence or historical non-compliance. This recalibration is designed to extract higher revenue yields by focusing resources on taxpayers with a demonstrable history of investigative interest.

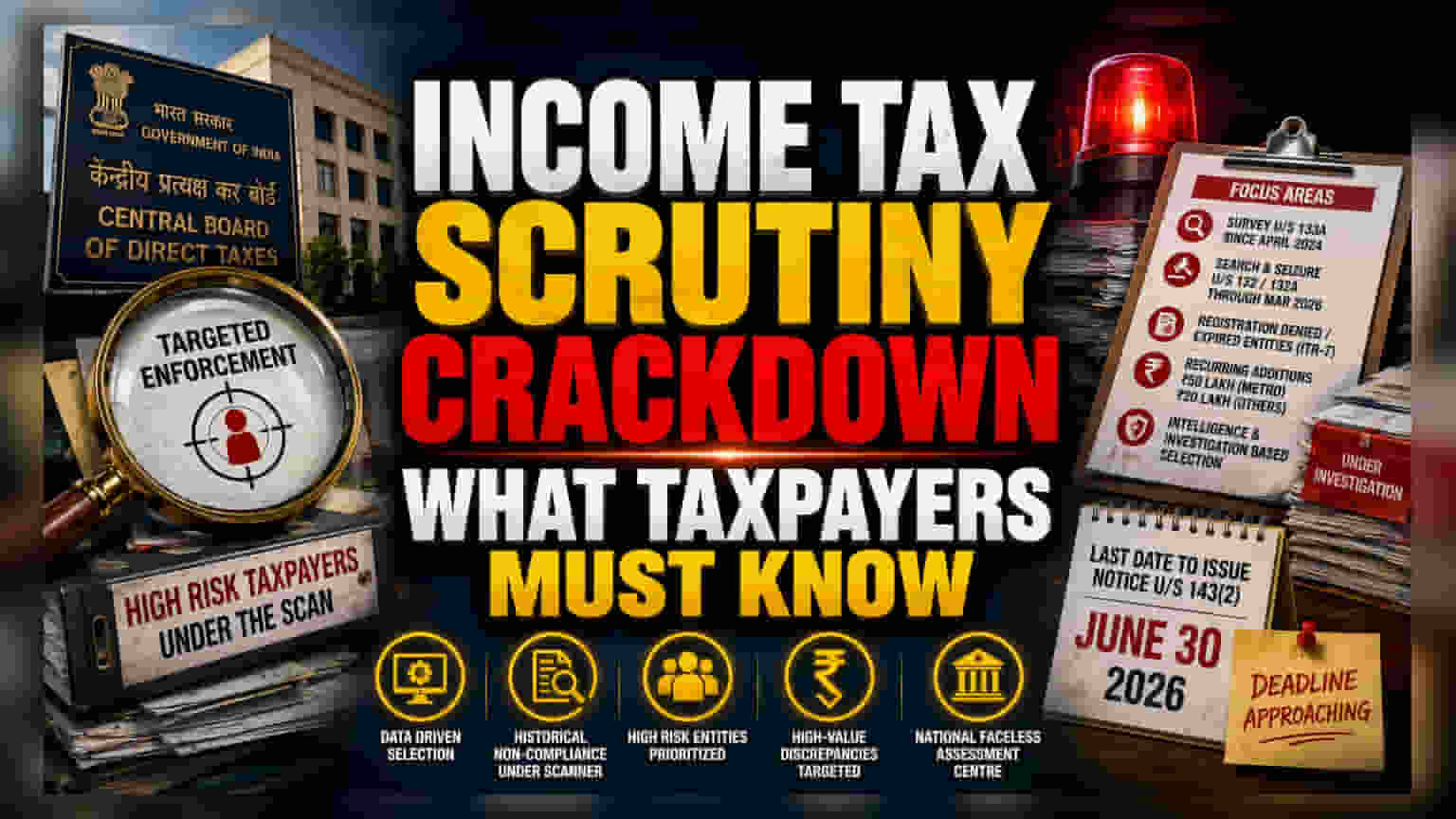

The Anatomy of the Scrutiny Net

Administrative pressure is mounting on six specific taxpayer cohorts. Foremost among these are entities subjected to survey operations under Section 133A since April 2024. By extending the scrutiny net to include search and seizure cases processed under Section 132 or 132A through March 2026, the department is ensuring that any subsequent income tax returns are scrutinized for consistency with evidence unearthed during those earlier enforcement actions. The inclusion of trusts and academic institutions that persisted in claiming tax benefits despite the formal expiration or denial of their registration status represents a distinct hardening of the regulatory stance on non-profit compliance.

The Valuation and Information Threshold

The reliance on recurring income additions serves as a key indicator of systemic tax avoidance. By maintaining a threshold of ₹50 lakh for metropolitan hubs and ₹20 lakh for secondary jurisdictions, the department is signaling that it will pursue serial offenders whose past assessments reveal persistent, high-value discrepancies. Unlike data-matching exercises that rely on passive AIS or SFT records, this approach utilizes active intelligence sharing from external law enforcement and the department’s own investigation wings. This indicates a move toward inter-agency integration where criminal or regulatory inquiries in one sphere automatically trigger tax-compliance reviews.

Operational Risks and Compliance Deadlines

For corporate tax departments and high-net-worth individuals, the June 30, 2026 deadline for issuing notices under Section 143(2) creates an immediate window of peak volatility. The strict focus on ITR-7 filers—specifically those with unresolved registration issues—highlights a specific weakness in the governance of charitable entities. Entities that failed to secure appellate reinstatement of their registration prior to the March 2025 cutoff face a high probability of assessment. The administrative burden is shifted heavily onto the taxpayer, requiring rigorous documentation to justify deductions that were historically treated with more leniency. Any entity failing to reconcile these specific historical flags with current filings risks prolonged engagement with the National Faceless Assessment Centre, where the burden of proof remains firmly on the claimant.