In May 2026, leading mutual funds including Quant ELSS and Motilal Oswal Midcap raised their holdings in Premier Energies, even as promoters sold shares. This institutional buying highlights confidence in the company’s strong order book and renewable energy expansion, though investors should track the execution of future projects.

What Happened

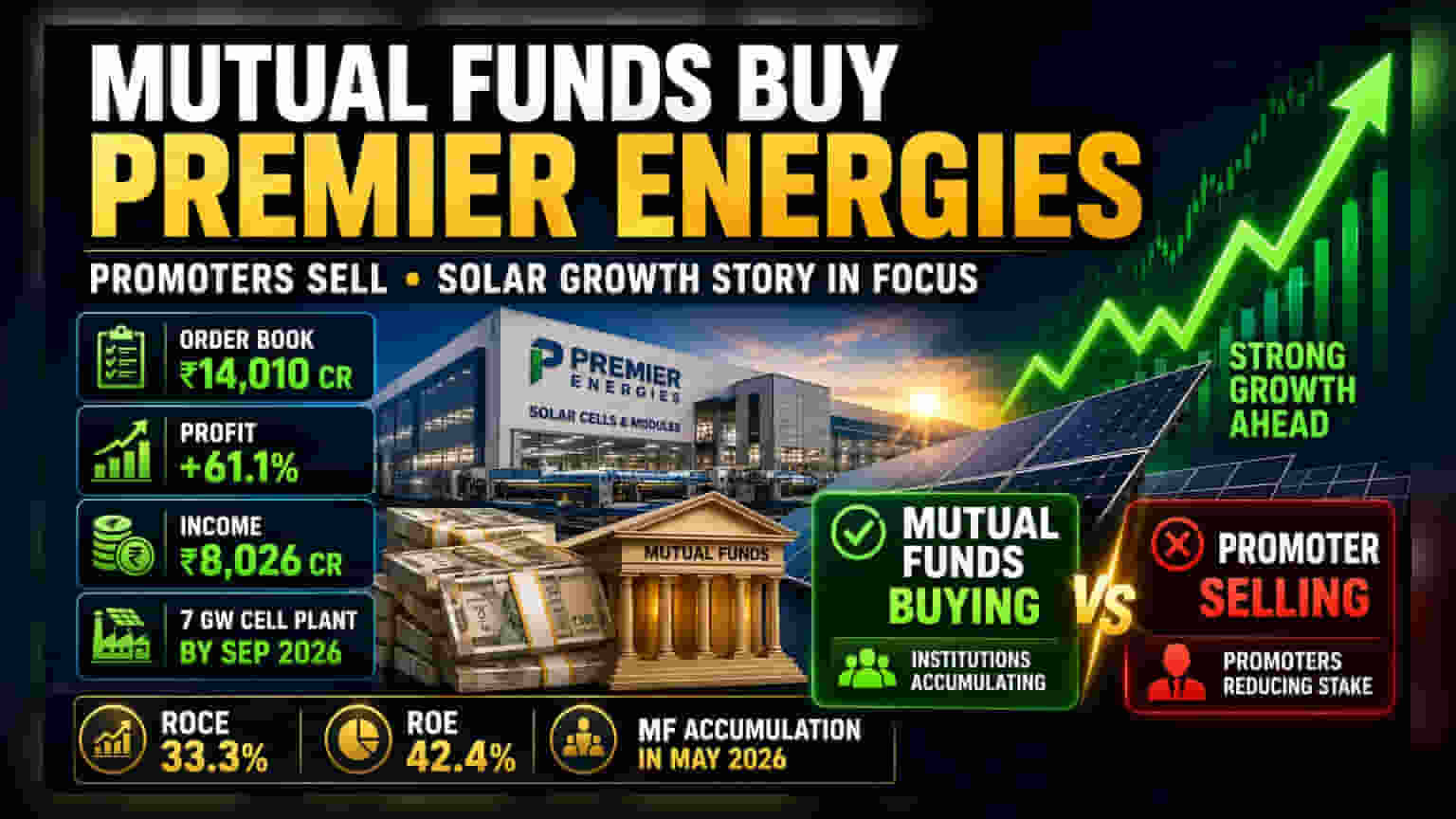

During May 2026, major mutual fund houses aggressively accumulated shares of Premier Energies Limited. Notable investors such as Quant ELSS Tax Saver and Motilal Oswal Midcap Fund were among the top buyers, with some funds allocating more than 1% of their total assets to the stock. This surge in buying is significant because it occurred simultaneously with share sales by the company's promoters. While promoter selling can sometimes signal a lack of confidence, the counter-action by large institutional investors suggests a belief in the company’s underlying growth story.

The Disconnect Between Promoter and Institutional Action

When promoters sell shares, it often raises questions among retail investors. However, institutional buying by large mutual funds typically indicates that professional analysts have reviewed the company’s fundamentals and see value beyond the short-term supply of shares. Mutual funds often focus on the long-term potential of the company’s order book and its strategic role in India’s renewable energy sector. Investors should view this as a divergence in outlook between insiders and external institutional managers, which is not uncommon in growing mid-sized companies.

Strong Financials and Growth Pipeline

Premier Energies reported solid growth for the financial year ending March 2026. The company’s total income rose by 20.7% to ₹8,026 crore compared to the previous year, while profits grew significantly by 61.1% to ₹1,509.7 crore. A key driver of this performance is a strong order book of ₹14,010 crore, which increased by 66% year-on-year. The company has also maintained high return ratios, with a Return on Capital Employed (ROCE) of 33.3% and a Return on Equity (ROE) of 42.4%, indicating efficient use of capital to generate profit.

Understanding the Risks and Expansion

The company is in the middle of a massive manufacturing expansion. It has already commissioned a 5.6 GW module facility and is currently building a 7 GW cell plant, which is expected to start operations in September 2026. Other projects include a 10 GW ingot-wafer plant, a 6 GWh Battery Energy Storage Systems (BESS) facility, and a 3 GW inverter plant. Furthermore, the company acquired a 51% stake in Transcon Ind Limited in April 2026 to boost its transformer business.

While these expansions show growth intent, they also carry risks. The primary challenge is execution—any delay in setting up these new plants could impact revenue targets. Additionally, managing such a large project pipeline requires consistent capital availability and smooth operational management. Investors should watch how quickly these facilities start contributing to revenue.

What Investors Should Monitor

Moving forward, the key things for investors to track include the successful commissioning of the 7 GW cell plant by September 2026 and the progress of the newly acquired Transcon Ind business. Additionally, monitoring future shareholding pattern filings will be important to see if mutual funds continue to add to their positions or if promoter selling trends change. Finally, maintaining a watch on whether the company can sustain its current profit margins amidst large-scale manufacturing expansion will be crucial.