Housing Sales in Tier 2 Cities Show Mixed Trends

A recent report by PropEquity, a real estate data analytics firm, reveals a nuanced picture of the housing market in India's top 15 tier 2 cities for the third quarter ending September 2025 (Q3 2025). While the volume of housing sales experienced a slight decline, the overall value of these sales saw an increase, signaling a growing preference for premium properties.

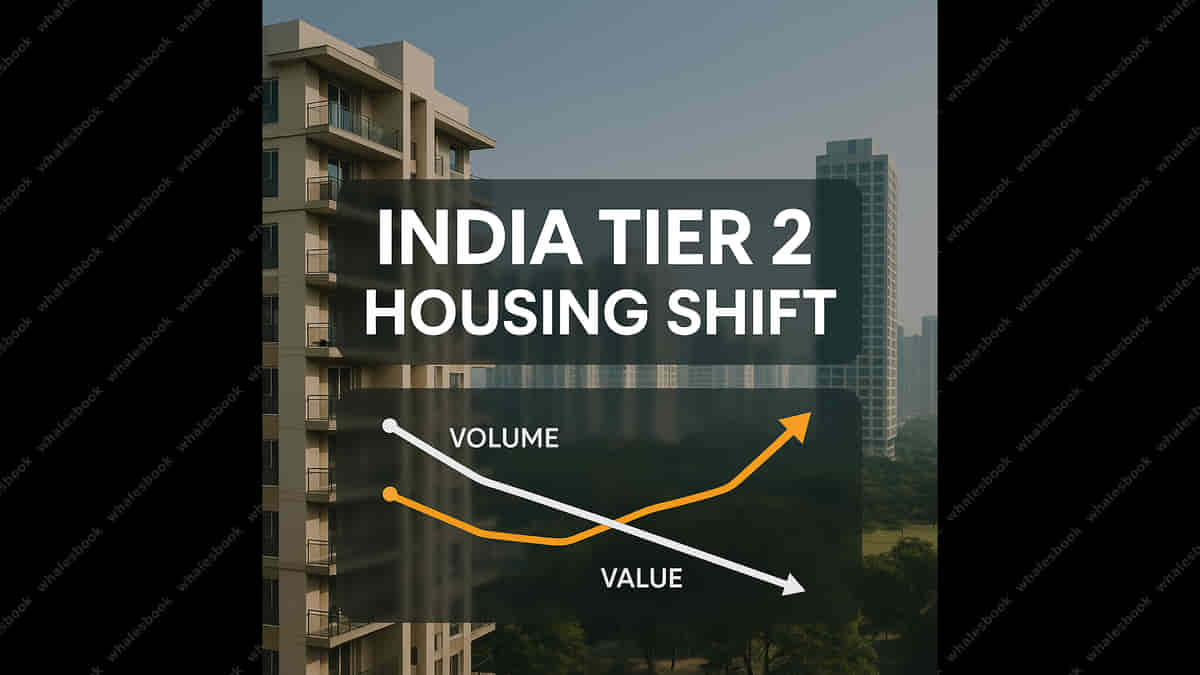

Key Numbers and Market Performance

- Sales Volume Decline: Housing sales across these 15 cities dropped by 4% year-on-year (YoY) to 39,201 units in Q3 2025.

- Sales Value Growth: Despite the volume decrease, the total sales value climbed by 4% YoY, reaching Rs 37,409 crore.

- New Supply Drop: New housing supply saw a significant reduction, declining 10% YoY to 28,721 units.

- Quarter-on-Quarter (QoQ) Trends: On a quarter-on-quarter basis, housing sales fell by 3%, sales value by 1%, and new launches by 26% in Q3 2025.

Regional Variations

Eight out of the fifteen cities surveyed recorded a year-on-year decline in housing sales. Bhubaneshwar experienced the most substantial drop, with sales falling by 26%. Conversely, Trivandrum saw the highest increase in sales at 19%. Bhubaneshwar also faced the steepest decline in new property launches, down by 88% YoY. Ahmedabad maintained its position as the leading market in terms of both sales volume and new launches.

Driving Factors for the Market Shift

Samir Jasuja, Founder and CEO of PropEquity, attributed the moderation in sales momentum, particularly in the affordable and mid-income segments, to rising input costs and evolving consumer aspirations. He noted that increasing home prices and larger home sizes are gradually influencing buyer choices.

- Jasuja also highlighted the sustained importance of tier 2 cities as growth engines for India, driven by expanding employment opportunities, infrastructure development, and improved connectivity.

Gujarat's Dominance in Real Estate

The four cities in Gujarat—Ahmedabad, Surat, Gandhi Nagar, and Vadodara—continue to be dominant forces in tier 2 real estate, collectively accounting for over 60% of both launches and sales. Lalit Parihar of Aaiji Group emphasized that robust economic growth, manufacturing strength, a rise in white-collar employment, and rapid infrastructure upgrades are fueling strong housing demand in these regions. He pointed to their balanced offering of affordability, quality of life, and long-term investment potential.

Impact

This trend suggests a potential shift in developer focus towards higher-margin premium housing, which could impact inventory levels and pricing strategies. It may also benefit companies supplying premium construction materials or those catering to a more affluent buyer segment. Investors in real estate could see varying performance among developers based on their product mix and geographic focus. Overall market sentiment might be influenced by the affordability challenges arising from rising home prices.

Impact Rating: 7/10

Difficult Terms Explained

- YoY (Year-on-Year): A comparison of data from a specific period to the same period in the previous year.

- Tier 2 Cities: Cities that are considered major economic and population centers but are not the largest metropolitan areas (like Tier 1 cities).

- Sales Value: The total monetary amount generated from selling properties.

- New Supply: Refers to the number of new housing units that are launched or made available in the market.

- Affordable and Mid-Income Segments: Housing categories priced within the reach of low to middle-income groups, typically based on local economic conditions and income levels.

- QoQ (Quarter-on-Quarter): A comparison of data from a specific quarter to the immediately preceding quarter.